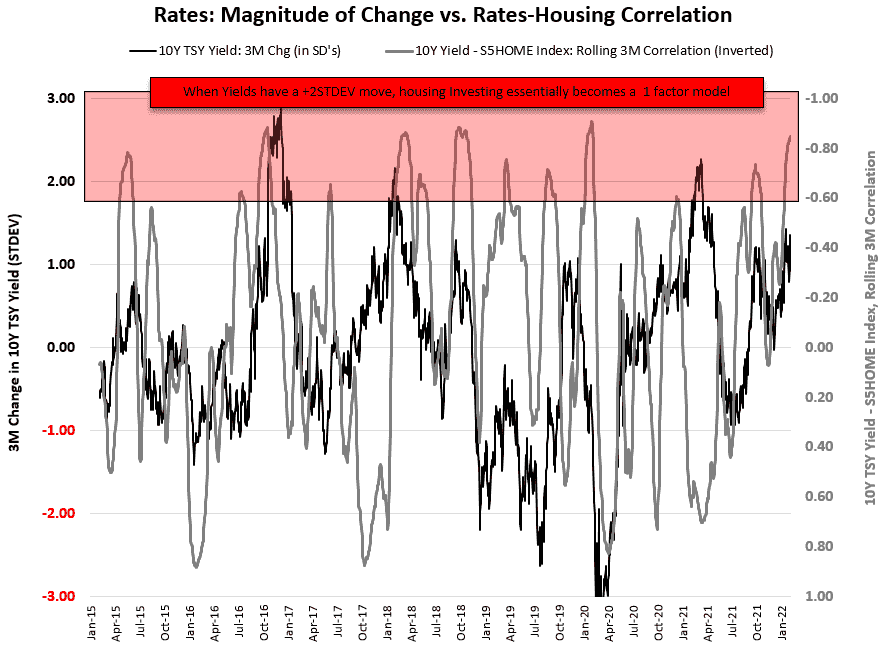

Below is a chart and brief excerpt from today's Early Look written by Macro analyst Christian Drake.

Housing = 1-factor model:

|

Below is a chart and brief excerpt from today's Early Look written by Macro analyst Christian Drake.

Housing = 1-factor model:

|

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.