Position: We sold out of our LONG corn position (the ETF CORN) in the Hedgeye Virtual Portfolio after this morning’s USDA crop report for an immediate term TRADE gain.

Supply

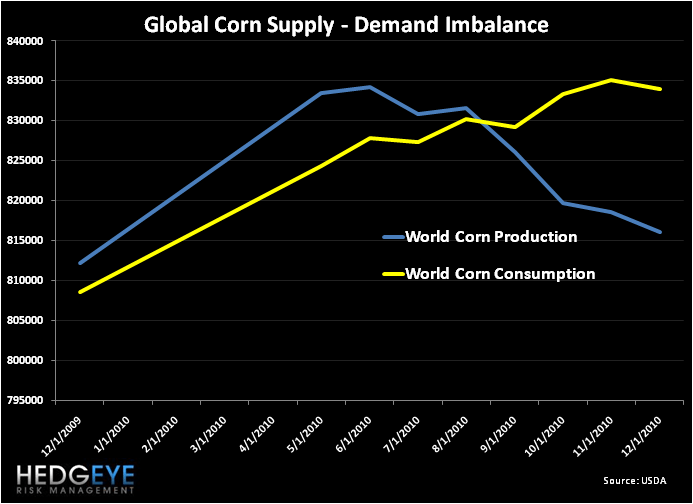

The USDA reported today that inventories of corn in the US as of December 1st were 10.04B bushels, an 8% decrease from last year’s level of 10.90B bushels. The agency also revised down its estimate for the 2010 total corn crop to 12.45B bushels from 12.54B bushels, taking the 2010 crop yield 5% below last year’s.

Looking ahead, the USDA expects that corn stocks will fall to 745MM bushels before the 2011 harvest begins, revised down from a projection of 832MM bushels made last month and below the consensus estimate of 779 MM bushels. The downward revision is due to US corn production seen to come in 93MM bushels lower than previously expected in 2010-11, as a 1.5 bushel/acre reduction in the national average yield outweighs an 183,000 acre increase in harvested land. On trade, the USDA is projecting a 5MM bushel increase in corn imports – only a minor dent in the domestic production decline.

Demand

Demand for the grain appears to be holding strong – corn consumption in the US for the three months ending in November was 6.5% greater year-over-year. Globally, the USDA tempered its worldwide consumption estimate by 0.2% to 836.1B bushels, still a 2.9% increase year-over-year.

Price

The report sparked corn prices – corn futures for March delivery jumped 22 cents this morning to $6.29/bushel – the highest level since July 2008.

Going Forward

We expect corn prices to trend higher this winter. While current prices are at a two-year high, domestic stockpiles are at a four-year low – thus, the supply fundamentals are bullish for price. Demand for the grain, which is more inelastic than supply, is sticky in the US and the rest of the world, evidenced by the USDA’s report today. These factors, coupled with exogenous events like the extreme flooding in Australia and dry weather in Brazil and Argentina, lend to a tight floor of support for corn prices in the intermediate term.

Kevin Kaiser

Analyst