Position: Long Germany (EWG); Short Italy (EWI), Euro (FXE)

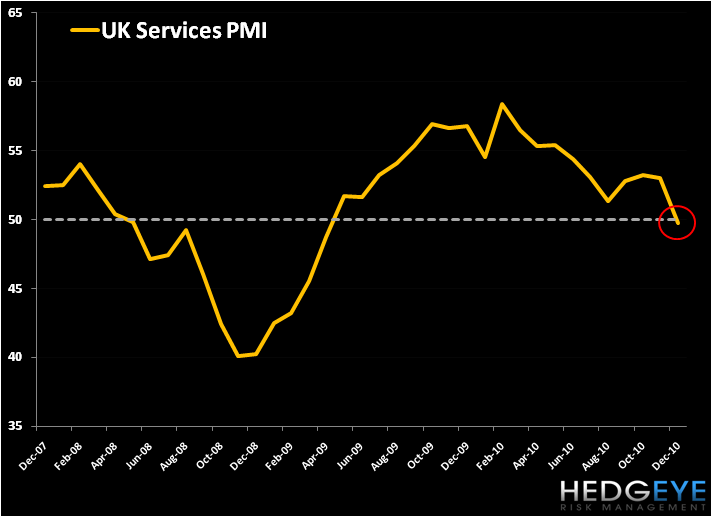

UK Services PMI for December declined to 49.7 versus 53.0 in November, and importantly fell below the 50 level that divides expansion (above 50) and contraction (below 50).

As we’ve noted in previous work, including yesterday’s piece titled “Europe’s New Year’s Update”, we believe inflation in the UK will continue to be a negative headwind in 2011. In the most recent Bank of England Minutes the committee concluded that over the intermediate term CPI could reach as high as 4.0%. Even at its current level of 3.3% Y/Y we’re cautioning that consumption can be chocked off.

While UK Manufacturing PMI showed a gain to 58.3 in December (the highest in 16 years) versus 57.5 in November, given the prospects for slower growth this year, including the economies of its main trading partners in Europe, there’s reason for caution. The UK’s austerity program over the next 4 years is a tax on the consumer and should weigh on confidence to the downside. With Services a stronger driver of overall growth than manufacturing in the UK, we believe this inflection in the Services PMI is meaningful and stagflation may not be far afield.

Currently we’re playing Europe’s Sovereign Debt Dichotomy with a short position in Italy (we re-shorted the etf EWI on 1/4), and are short the Euro (FXE) with a TRADE range of $1.30-$1.32 versus the USD. We remain long Germany (EWG) in our Virtual Portfolio.

The BoE meets next on January 13th to announce its interest rate policy, with consensus expectations of no change to the current main rate of 0.50%.

Matthew Hedrick

Analyst