“He who will not economize will have to agonize.”

-Confucius

Sitting at my desk in New Haven this morning, what I do know is my own pain. What I don’t know, is what someone else’s feels like. We’ll see how the levered-long US stock market bulls feel on the first tweak today. This isn’t a snap, yet – this is a tweak.

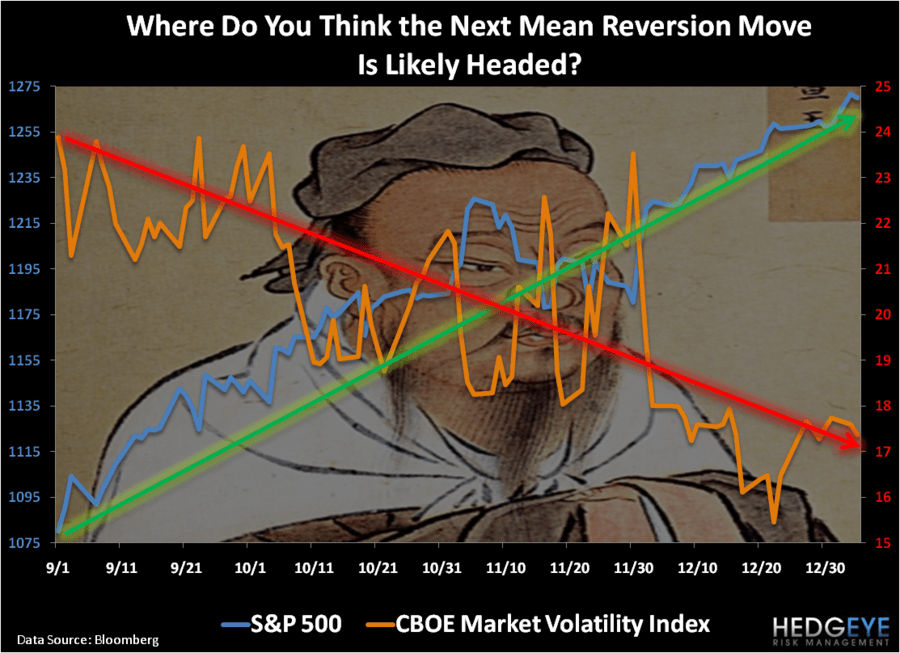

The agony of defeat isn’t new to global macro markets as of this morning. It’s been new to US Treasury and Emerging Debt Markets since November. It was new to the Gold market yesterday during a $40/oz swoon (we’re short GLD). What goes around in terms of mean reversion risk, eventually comes around. You can learn this lesson in a variety of ways in life. In markets, the best way to learn this lesson is the hard way.

If you didn’t raise your Cash position in the last week, it wasn’t because we didn’t tell you to. We started the year with a 61% US Cash position in the Hedgeye Asset Allocation Model and the US Dollar Index has been up every day for the year-to-date (including this morning).

Yesterday, on commodity market weakness we invested 6% of our cold hard cash into oil and corn. Now we have 55% of our hard earned capital in cash. Being in Cash means you can invest it lower.

To be sure, there is absolutely no doubt that you can ride Hi-ho, Silver and call yourself Captain Cowboy on the ride to everything making higher-highs, until they don’t. So you better have a risk management plan when the music stops.

In addition to Gold selling off hard yesterday, US small cap and housing stocks got creamed, trading down -1.8% and -1.5% respectively (XBH and IWM). This morning, European stock markets and US Futures are getting hit hard after Portugal raised 6-month paper at a yield of 3.68% (vs 2.04% last!) and Asia closed down across the board.

This interconnected game of risk has always been “on” – it’s just when everyone stops paying attention to the moving parts that it starts to be a lot more fun. On balance, our intermediate-term TREND view on the global economy remains intact:

1. Global Growth Slowing

2. Global Inflation Accelerating

3. Globally Interconnected Risk Compounding

Now, before a US centric stock market bull gets his/her shirt in a knot about this, allow me to kick off this morning’s Global Macro Grind with a remedial reminder that all of the aforementioned points start with the word Global. That’s right, say it just like Paul Newman had the owner of the Charlestown Chiefs say “H-owned”… G-lo-bal… G-lo-bal…

In terms of the global macro data points that are in my notebook for 2011 to-date, here’s the grind:

- South Korean inflation (CPI) jumps to +3.5% in DEC vs +3.3% in NOV and the Korean government declared “war on inflation”

- South Korean exports slow, sequentially, from their NOV highs of +25% to +23.1% in DEC

- Polish Inflation (CPI) jumps to +3.1% in DEC vs +2.7% in NOV and 2-year bond yields in Poland are pushing to +4.9% this morning (highest in a year)

- Chinese manufacturing (PMI) drops for the 1st time in 5 months (53.9 DEC vs 55.2 NOV) as growth continues to slow

- German manufacturing (PMI) accelerates again sequentially to a new high of 60.7 DEC vs 58.1 NOV

- German unemployment stays unchanged m/m at 7.5% for DEC vs NOV

- Brazil’s newly elected President, Dilma Rousseff, kicks off the New Year calling inflation trends pushing to +6% y/y “the plague”

- Pakistan’s PM loses his majority and a key Governor is murdered overnight as Pakistan now has to face the Taliban and +15.48% inflation

- UK manufacturing (PMI) remained flat, sequentially, in DEC vs NOV at 58.3

- Indonesia’s inflation (CPI) accelerates, sequentially, to +6.96% DEC vs +6.33% NOV

- European Union inflation (CPI) accelerates to a 2-yr high of +2.2% in DEC vs +1.9% in NOV

- Australian manufacturing index slows for the 4th consecutive month (pre JAN floods) at 46.3 DEC vs 47.6 NOV

- Thailand inflation (CPI) ramps, sequentially, to +3.0% DEC vs +2.8% NOV

I’ll go Lone Ranger (sans le hi-ho, Gold) and stop at point #13 just to push my own book and summarize that if Captain American Stock Picker (he’s back!) wants to tell me that “growth is back!”… and that the rest of the world’s growth and inflation risks cease to exist… that he/she may want to, at a bare minimum, economize that bullishness and wait for lower prices.

Back to the USA, where consensus is running rampant that the US consumer is Just Lovin’ It (except the collapse of MCD’s stock), this morning’s ABC Consumer Confidence reading (it’s weekly) dropped for the 2nd consecutive week (i.e. dropping both weeks post Christmas shopping) back down to minus -45. That’s only a few points away from its all-time low and even a Thunder Bay Bear on some things US Equities would call that agonizingly cold!

My immediate term support and resistance lines for the SP500 are now 1261 and 1270, respectively. A close below 1261 puts 1237 in play.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer