As one of the few unregulated areas of health care, the pharmaceutical industry has been fertile ground for rent seekers to grow and prosper. It has to be the only industry in the U.S. with at least five different types of entities - all with their hand out - standing between the manufacturer of the product and the end user. Almost all are paid on a spread basis. Wholesalers might get 5-6% of the drug price, Pharmacy Benefit Managers might get 2% and so on.

It is an arrangement that works ok as prices decline and middlemen wedge themselves into a fattening delta between what the customer (or their insurer) pays and what it cost to produce the drug. I say it is only "ok" because distortions emerge - like cash-pay coupons offered by GDRX - as a necessary response to the widening spread between the list price and what the manufacturer is eventually paid.

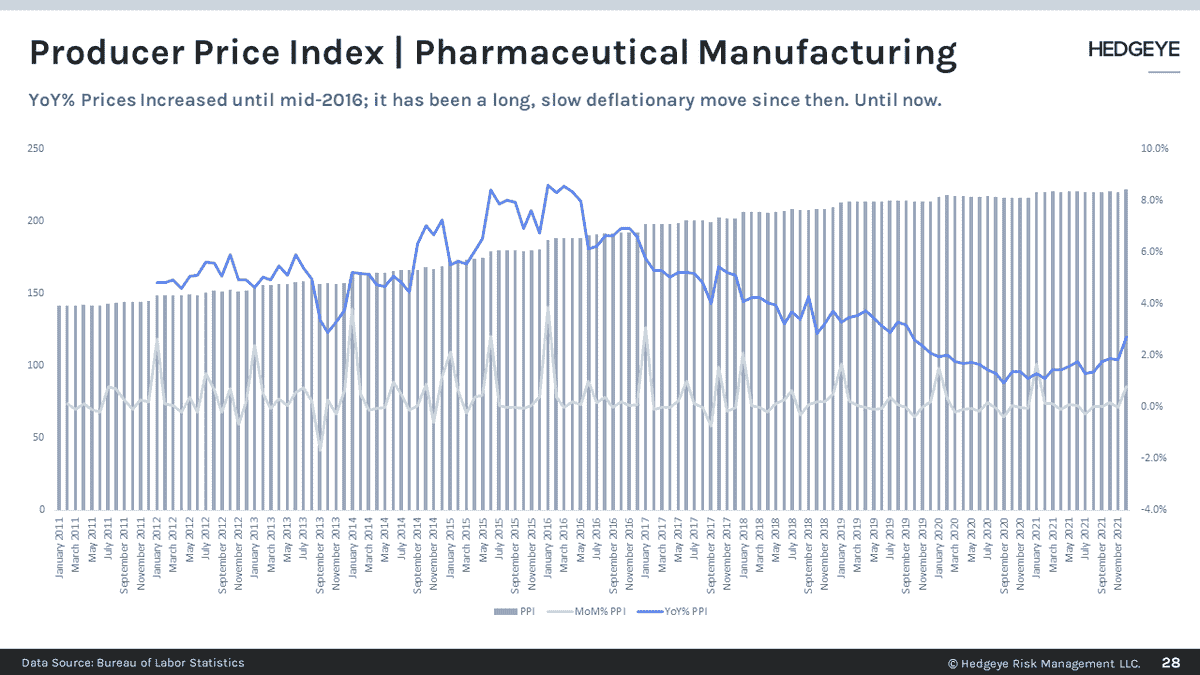

What happens then the trend reverses itself?

Since 4Q 2020, the PPI for drug prices has been bumping along at the bottom of a five year trend. In late 2021 it started to move north. Will it endure? CAH reported at JPM22 that inflationary impacts are hard to predict. MCK appears to be pivoting away from simply wholesaling to offering drug supply chain "solutions." External trends also seem to suggest the answer is yes.

Part of the deflation of producer drug prices can be attributable to cheap imports. It is a problem that was noted first by the Defense Department in late 2018. As the U.S. moves to limit the political risk to the drug supply chain, it will become more dependent on manufacturing capacity with higher wage levels. Another factor will no doubt continue to be transportation costs.

As prices for production and distribution, rise wholesalers, PBMs, GPOs and Pharmacies are going to have to justify their cut of the spread between what it costs to make a drug and what the customer or insurer pays for it. Given all the heat that Pharma has taken, an inflationary trend seems like a golden opportunity to reconsider the role of everyone who has their hand in the drug supply chain cookie jar.

Emily Evans

Managing Director – Health Policy

Twitter

LinkedIn