This guest commentary was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst. This piece does not necessarily reflect the opinion of Hedgeye.

|

“In an August 2005 interview, Robert Shiller predicted U.S. house prices could fall by 40 percent (Leonhardt, 2005). The S&P/CaseShiller U.S. National Home Price Index began to fall in the third quarter of 2006. The house price index for purchase transactions produced by the Office of Federal Housing Enterprise Oversight (OFHEO) declined for the first time (since 1993) in the third quarter of 2007.” David C. Wheelock |

Over the holiday break, we focused on a couple of writing projects in between watching football and holiday reunions. In particularly, we wrote a new column for National Mortgage News on the return of the Zombie loan.

We also put some finishing touches on a new paper on enhancing the liquidity of Ginnie Mae mortgage servicing assets that we'll be posting on SSRN. And we had a great conversation with Wilfred Frost of CNBC on the outlook for banks in the US in 2022.

The good news of sorts is that the outlook for residentially house assets generally remains quite positive, with the exception of the prospective re-default of tens of thousands of loans that were modified at the behest of progressives in Congress as a result of COVID.

As these zombie COVID loans default, again, servicers will simply modify the loans and sell the loans into a new pool – and pocket a new gain on sale. Perfect. Indeed, until such time as voters show the progressives the door, these re-defaulted or "zombie" loans will simply be rolled, again and again. And the taxpayer, through the GSEs and the FHA, will foot the bill.

The bad news, however, is that the urban subset of commercial loans, including mortgages on multifamily real estate, are in for a tough year.

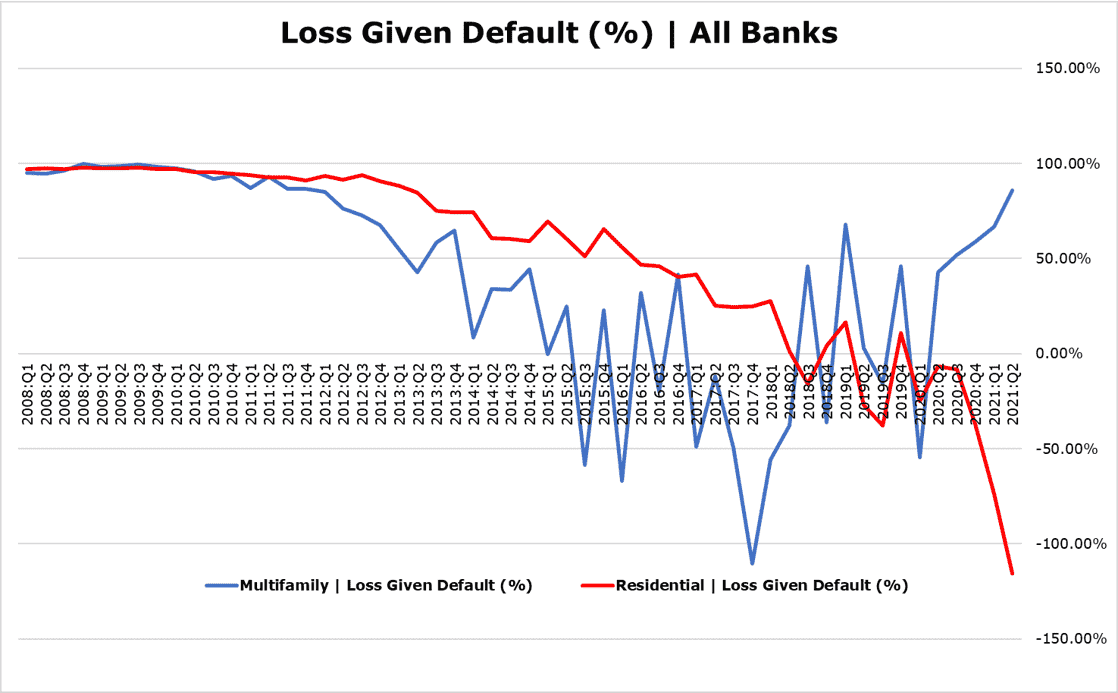

National statistics for commercial real estate are improving, yet for some reason the indicator of loss given default or LGD for the $500 billion in bank-owned multifamily loans was 75% of the loan balance in Q3 2021. This is above the ten year average LGD for multifamily loans.

Source: FDIC/WGA LLC

Loss rates for multifamily loans owned by banks have been elevated for two years, even before COVID.

While the absolute number of defaults is low, it is far higher than the other series for residential housing, all of which show net-charge off rates at or below zero. Notice that LGD on multifamily loans and 1-4s basically tracked up through 2017, then diverged.

Meanwhile, the LGD for 1-4s was negative 130% in Q3 2021, meaning that banks are generating more than twice the loan proceeds in those rare instances when they sell a home in foreclosure. This metric, which is based upon the Basel I methodology, suggests that home prices are very inflated. Send those cards and letters to Chairman Jerome Powell c/o The Federal Reserve Board in Washington.

Two obvious questions should occur to investment and risk managers: First, how big will the losses be to lenders as a result of the credit problems facing urban commercial and multifamily properties? Second, how much longer will the positive, really surreal credit conditions persist in 1-4 family assets? As we’ve already noted, there are signs of lender fatigue and credit stress in some of the more aggressive fringe products in the housing complex.

Our best guess on commercial credit exposures is that banks and bond holders could face tens of billions in losses over the next several years.

The change in asset utilization for many urban properties in New York City is profound. New York City and its environs face a difficult period of right-sizing government to fit a metropolis with an expanding sense of entitlement and a shrinking commercial base.

The commercial real estate community and the lender banks are putting brave face on a daunting situation. A group of nine banks provided the $3 billion to SL Green, the National Pension Service of Korea and Hines’ One Vanderbilt in June 2021, The Real Deal reports.

Wells Fargo reportedly originated half of the total debt, or $1.5 billion, while Goldman Sachs contributed $600 million. Bank of America, Bank of China, Bank of Montreal, Deutsche Bank and JPMorgan Chase each provided $150 million.

One Vanderbilt is one of the newest and most attractive properties in Manhattan, located next door to Grand Central Station. But on the other side of GCT, 245 Park Avenue just slipped into special servicing before the New Year. Go further East to Lexington Avenue and then Third Avenue, and what you see is one mostly empty commercial building after another, from 42nd Street all the way into the 60s on Manhattan's East Side.

Go west across the island of Manhattan to Hudson Yards on 10th Avenue in the 30s. Work on Phase 1 continues toward completion, again due to the forbearance of the bank lenders. When will Phase 2 begin, to monetize the remaining air rights over the westbound train tracks below? Nobody knows, but the payments for those air rights were financed with debt, of note.

Keep in mind that, where possible, banks will roll commercial loans to avoid a more general markdown of impaired collateral in the portfolio, but there is only so long forbearance can go on until the rules break. Bank investors should watch Q4 2021 disclosure carefully for signs of regulatory forbearance for commercial and particularly multifamily residential assets in 2022. After all, it’s an election year. That is, don't just read the press release.

Meanwhile, the Wall Street Journal reports that the US mortgage industry wrote $1.6 trillion in purchase mortgages in 2021, a record that was broken in large part due to the Fed-induced housing price inflation.

When the MBA stats for the full year are released, we suspect that the industry wrote fewer, bigger mortgages to achieve this feat. The conforming loan limit was $417,000 in 2008, but today is just shy of $1 million thanks to the FOMC. That's a more than 100% increase in 12 years of rising inflation and debt.

As with the zombie COVID mortgages and underwater multifamily properties, there is likely to be a larger, more general delinquency problem with residential mortgages down the road, probably in time for the next Presidential election in 2024 or shortly thereafter.

During this period, keep in mind, the FOMC intends to reinvest the proceeds of redemptions of both Treasury debt and mortgage-backed securities in the system open market account (SOMA), the engine of US inflation. That is, the FOMC will continue to stoke the fires of inflation by purchasing government debt and mortgage bonds rather than allow the SOMA to shrink.

Quite to the contrary to the ignorant narrative about tapering quantitative easing or “QE,” the Fed will continue to suppress home mortgage interest rates and there will push further home price inflation, hurting affordability. We will simply run out of buyers, with or without an increase in housing supply, as has historically occurred.

When pondering the outlook for US housing over the next five years, we think it is prudent to consult the historians. David C. Wheelock, a much revered economist with the St. Louis Fed, wrote the analysis for the May/June 2008 issue of Review (“The Federal Response to Home Mortgage Distress: Lessons from the Great Depression”).

In discussing the Great Depression and the 2008 financial crisis, Wheelock notes that home prices actually peaked in the mid-1920s and, more recently, in 2005, but it took several more years before the proverbial wheels came off the skateboard. It is 2005 all over again kiddies.

Wheelock writes:

“Although the nominal value of mortgage debt peaked in 1930 and then declined, deflation caused the real value of outstanding mortgage debt to continue to rise until 1932. Thus, consistent with [Irving] Fisher’s (1933) classic “debt-deflation” theory, the burden of outstanding mortgage debt increased sharply during the contraction phase of the Great Depression and economic recovery did not begin until the real value of outstanding debt had begun to decline.”

In modern day terms, the fact of a federal guarantee on principal and interest for agency and government insured MBS suggests that this time it will be different from 2008, when more than half the mortgage market was private label.

Yet the differences between the market of 1925, 2005 and 2025 include both positive and negative factors. Yes there is a credit guarantee on the MBS, but the 1) liquidity risk and 2) cost of servicing due to Dodd Frank and general progressive craziness means that a big residential home price correction could become an existential event for many lenders.

SO as we move into Q4 2021 earnings for financials in the next two weeks, keep your eyes peeled for news of restructuring of bank loans on urban commercial and multifamily properties.

Defaults on commercial loans can be delayed for months, and have been since 2020. In 2022, though, with state and federal foreclosure moratoria ending, the economic cost of COVID will emerge as a factor for many lenders. But the day of reckoning in residential housing is still several years away.

ABOUT CHRISTOPHER WHALEN

Christopher Whalen is the author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington. Currently, he serves as the editor of The Institutional Risk Analyst.