"We always overestimate the change that will occur in the next two years and underestimate the change that will occur in the next ten."

– Bill Gates

St. Patrick’s Day is big in our house. When my kids were younger, they would ask whether I had ever seen an actual Leprechaun. When I told them yes, they asked how/when/what were the circumstances. I took a deep breath for dramatic effect and, in my most matter-of-fact voice, explained that the truth was that the only way you could see a leprechaun was to summon one. And the only way to summon one was to fold a single piece of notebook paper in half eight times. (Earlier that week, I had read about how this was impossible. I then tested and confirmed said impossibility.) On the eighth fold, I told them, the Leprechaun appears.

Unsurprisingly, my kids immediately began folding paper and quickly found out that they couldn’t fold it seven times, let alone eight. If you’re curious, give it a try and you’ll see what happens. While they didn’t realize or appreciate it at the time – and probably still don’t – this was their first lesson in exponents.

Humans – young and old – are generally terrible at comprehending the implications of exponential growth. The human brain tends to think about things in linear terms. This is a product of our evolution and everyday experience. In the above example, we intuitively know that folding a piece of notebook paper in half is easy. We also know that doing that a second time is still easy, and so we assume that easiness perpetuates into the future without realizing what is happening at the exponential level.

In Jeff Booth’s book, The Price of Tomorrow, he takes my Leprechaun example to a much-further extreme and asks how thick a piece of paper would be if you folded it in half 50 times. The answer is amazing. While a standard piece of notebook paper is just 0.05 millimeters thick, if you folded it in half 50 times the thickness would become “tall” enough to reach from the Earth to the Sun. While that first ten folds only increase the thickness from 0.05 millimeters to 51 millimeters, the 20th fold by itself increases the thickness by 26,214 millimeters and the 50th fold increases it by around 35 million miles.

Perhaps the most famous example of exponents confounding people surrounds the purported origin story of chess. There are several versions of this story, but the general idea is that chess was invented at some point in the mid-13th century, likely in India. The King of India, the story goes, was so pleased with the game that he offered its inventor any reward he wished.

The inventor asked the King to put one grain of rice on the first square of the chess board and then double it on each subsequent square until all 64 squares were doubled. The King considered the request foolish because it would produce such a small reward for the inventor of such a wonderful game, but he ordered it be done.

Very quickly it became apparent that the request would be impossible to accommodate as it would require more rice than was in all of India. Different versions of the story have the inventor then being executed for making the King look foolish or being promoted to a high-ranking advisor for his cleverness.

Either way, let’s consider the request for a moment. There are 64 squares on a chessboard. To double the number of grains of rice on each square would require ~18.5 quintillion grains of rice (18.5 thousand, thousand, thousand, billion grains of rice). Global rice production averages 761 million metric tonnes per year. At 2,200 pounds per metric tonne and 25,000 grains of rice per pound, this works out to annual global rice production of ~41.8 quadrillion grains. It would take approximately 441 years’ worth of global rice production to fulfill the chessboard request.

That’s what is remarkable about exponential growth. Most people think about the first grain on the first square, followed by the two grains on the second square and then, maybe, the four grains on the third square, but likely don’t go much, if any, beyond that in their immediate thinking. As such, it’s almost unimaginable how huge the numbers become, like the ~9.2 quintillion grains of rice on the 64th square.

Now that we, hopefully, have a better appreciation for exponential growth, let’s consider which sector benefits the most.

Years ago, my colleague, Tom Tobin, recommended the book The Singularity by Ray Kurzweil and it changed my whole framework for thinking about time and progress in RoC (rate of change) terms. The book is about technology and technological progress and what happens when we reach the AI singularity somewhere around 2035-2040 (hint, bad things), but what it really is about is exponential growth.

Moore’s Law is the backbone of the argument, with Gordon Moore, the co-founder of Fairchild Semi and former CEO of Intel, postulating in 1965 that the number of transistors in an integrated circuit would double roughly every year for the next decade, and then double roughly every two years after that. What is remarkable is that that exponential trend has largely continued apace for the last fifty years.

Consider that in 1970 the Intel 4004 IC had approximately 2,000 transistors. More recently, the AMD Epyc Rome has close to 50 billion transistors on its IC. That works out to compound growth of around 41% per year for 50 years. In any given year or two, it’s not that remarkable or discernible, but over ten years – let alone fifty – the progress is extraordinary.

Back to the Global Macro Grind…

Pop Quiz. If I asked you what the performance of the 11 GICS Level One sectors has been since 12/31/18, could you answer correctly? Could you rank them? That time frame is interesting because it incorporates both pre and post-pandemic periods. For reference, in order, here are the sectors ranked from first to worst.

(12/31/18 – 12/23/21)

- Tech (XLK) +179%

- Cons Discretionary (XLY) +105%

- Communications (XLC) +89%

- Basic Materials (XLB) +75%

- Financials (XLF) +63%

- Industrials (XLI) +62%

- Real Estate (XLRE) +61%

- Health Care (XLV) +60%

- Cons Staples (XLP) +48%

- Utilities (XLU) +32%

- Energy (XLE) -4%

I raise the question because it highlights exponential growth and how dominant Tech is as a result. Not only did Tech outperform all other sectors on a cumulative basis since 2018, but it did so fairly consistently on a full-year basis. It was the top performing sector in 2019 (+48%), the top performing sector in 2020 (+42%) and is currently the third best performing sector YTD in 2021 (+33%), trailing only Energy (+45%) and Real Estate (+36%).

There is a structural tailwind embedded in tech in the form of exponential growth that confounds even sophisticated investors for the same reason most people would fail to correctly answer the question, would you rather have $1 million dollars today or a penny that doubled every day for a month.

Interestingly, and the second intended takeaway from today’s Early Look, there is another sector that has performed nearly as well as Tech since 2018. Any guess as to which one?

The answer is Housing. Since 2018, Housing (ITB) has returned 167% to Tech’s 179%. In 2019 Housing returned +48% to Tech’s +48% return. In 2020 Housing returned +26% to Tech’s +42% and in 2021 YTD, Housing has returned +44% to Tech’s +33%.

Why is this the case?

There are really two reasons. The first is monetary. From a strictly monetarist standpoint, Housing is a tremendous inflation hedge. In the simplest construct, if we take the US M2 of $14.547 Trillion at 12/31/18 and we compare it to the most recent reading of $21.269 Trillion on 11/1/21, we find that the money supply has grown +46.2% over that time period.

Now, let us consider home price growth in nominal terms. In December 2018 the S&P/Case-Shiller US National Home Price Index stood at 204.75. As of the most recent reading, September 2021, it stands at 271.18. That works out to an increase of +32.4%. Meanwhile, the housing stock has grown just +2.4% from 138.8M units at YE 2018 to 142.1M units at 9/30/21, so supply growth is only a small countervailing force.

So, on an annualized basis, you have the money supply growing at +14.5% per year since 2018 and home prices growing at 11.0% per year. We believe that we’ve already seen the point of peak Hawkishness from the Fed with expectations for rapid tapering and three rate hikes next year, and we see a sizeable Quad 4 event on the horizon in Q2 of 2022. As such, we expect that the pace of expansion of the money supply will remain elevated relative to both historic trends and expectations in the foreseeable future.

Monetary dynamics are the first backstop for the Housing market.

The second reason has to do with the Pandemic. Work-from-home increasingly appears here to stay. We now host quarterly calls with Ed Pinto, the Senior Fellow and Director of the AEI Housing Center and former head of Credit at Fannie Mae. This past quarter he presented some fascinating information on the WFH trends. He cited survey data suggesting 20-25% of the US workforce will continue to work from home post-pandemic. This works out to around an incremental 25 million US workers vs pre-pandemic levels.

He goes on to consider the cost-of-living – namely in housing – arbitrage opportunities associated with that secular trend. Consider the example of tech workers in San Jose, where the median home price is $1.35 Million, moving to the Phoenix area where the median home price is just $390k. Not only would they be saving a fortune on housing costs, but the median square footage of a home in Phoenix is 30% larger than that of San Jose, meaning that they would get 30% more house for less than one-third of the cost. Think about a) the discretionary spend potential that will free up, and b) the long-term structural demand impulse for rural/suburban housing in lower-cost areas.

These trends are now visible in inventory. While national housing inventory is down 55% across the board vs 2019 levels, the greatest shortages are in less dense areas. In fact, binning the housing stock into density quintiles shows that inventory in the densest quintile is down 26% vs 2019 while inventory in the least dense and second least dense quintiles is down 63% and 59% respectively versus 2019. That relationship exists across all quintiles in a monotonic function. In other words, we’re seeing this WFH arbitrage opportunity play out in real time, but the takeaway is that this will be a secular trend, not unlike the migration from physical to online shopping over the last 20 years.

Pre-pandemic, an area’s walkability was arguably the key factor. Not so much anymore. In the post-pandemic world, what matters is a larger living area, home office space, room for children, a larger yard, proximity to family, and access to open spaces.

This reshaping of the workplace will drive rural/exurban/suburban real estate demand for decades until the arbitrage spread narrows considerably. With national inventory at 40-year record lows currently, the only solution is to increase production – a process which has been structurally stymied by regulations. While NIMBY (Not In My Back Yard) used to be the mantra, today it’s BANANA (Build Absolutely Nothing Anywhere Near Anything). This regulation-induced supply constraint, aka artificial scarcity, puts the homebuilding industry in the driver’s seat and goes a long way towards explaining why, as a sector, housing has rivaled Tech over the last three years.

Nothing about that equation is poised to change in 2022 or 2023. In fact, the setup arguably becomes more favorable with massive GSE conforming loan limit bumps for 2022, underwriting standards set to ease meaningfully, looming student loan forgiveness, probable low-income buyer assistance programs, increasing institutionalization of single-family as a rental asset class, and demographic tailwinds through 2025 of would-be first time homebuyers set to gobble up everything in sight.

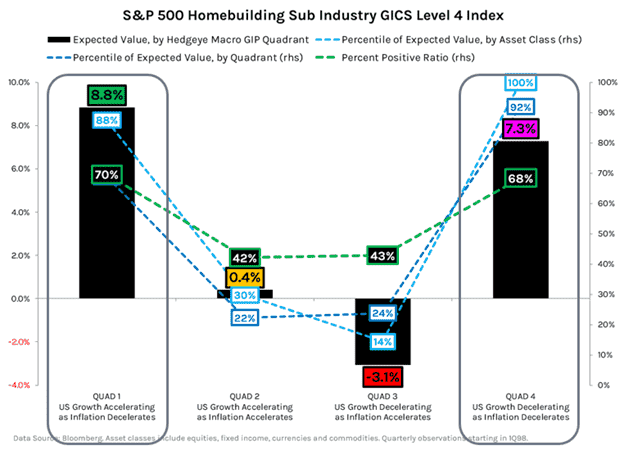

For this reason, we expect to see Housing remain near the top of the leaderboard, likely alongside Tech (though not in Quad 4 for Tech), for the foreseeable future. It’s also worth noting that Housing has historically performed best in Quad 1 and Quad 4 regimes. Our outlook for Q1 is Quad 1/Shallow Quad 4 and our outlook for Q2 is Quad 4.

Immediate-term Risk Range™ Signal with @Hedgeye TREND signal in brackets:

UST 10yr Yield 1.39-1.52% (neutral)

UST 2yr Yield 0.60-0.76% (bullish)

SPX 4 (bullish)

NASDAQ 14,960-16,001 (bullish)

RUT 2141-2278 (bullish)

Tech (XLK) 165.20-177.32 (bullish)

Consumer Discretionary (XLY) 191-208 (bullish)

Housing (ITB) 76.40-83.09 (bullish)

REITS (XLRE) 48.66-51.62 (bullish)

VIX 15.58-23.01 (bearish)

USD 95.80-96.82 (bullish)

Oil (WTI) 67.70-76.94 (bearish)

Nat Gas 3.52-4.18 (bearish)

Gold 1 (bullish)

Copper 4.18-4.49 (neutral)

To your continued Success,

Josh Steiner

Managing Director