TODAY’S S&P 500 SET-UP - December 28, 2010

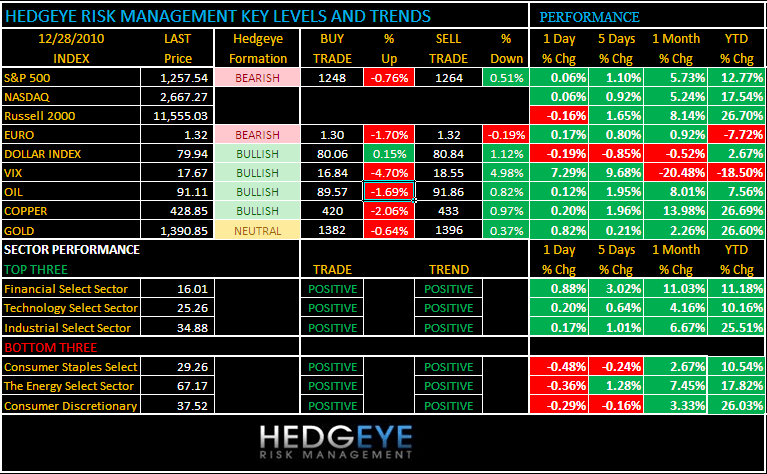

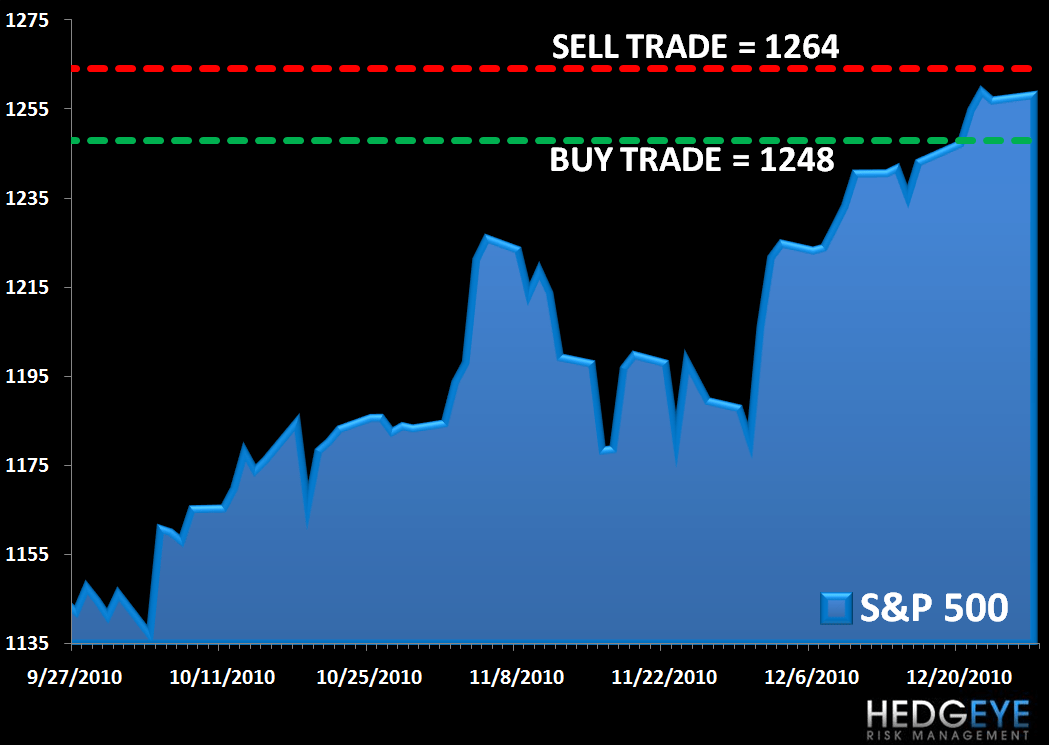

As we look at today’s set up for the S&P 500, the range is 16 points or -0.76% downside to 1248 and 0.51% upside to 1264. Equity futures are trading above fair value after Asia finished mixed and Europe trades flat. Volume low in volume internationally.

Today all eyes are on the Case-Shiller Home Price Index and December consumer confidence numbers. Home prices are estimated to drop in 0.2% Y/y in October - the housing data will remain a weak.

Other data and events today:

- Consumer confidence - December estimate is 56.4, prior 54.1

- Richmond Fed Manufacturing - December estimate is 11 prior 9

- U.S. to sell $25b 4-wk bills, $35b 5-yr notes

- ABC consumer confidence, prior -41

WHAT TO WATCH:

- ICSC releases weekly sales information; may revise December sales forecast following weekend results curtailed by snow.

- MasterCard Advisors’ SpendingPulse says total holiday season retail sales (including internet sales) from Nov. 5 through Dec. 24 rose 5.5%, best performance in five years.

- Travelers and New York commuters face further disruptions as winds hinder efforts to clear roads, runways. Passengers stranded after airlines canceled 6,000 flights face lengthy waits to rebook their trips

- AstraZeneca stops studies of experimental painkillers on concern they raise risk of joint damage; follows JNJ putting development program for fulranumab on hold last week.

PERFORMANCE

- One day: Dow (0.16%), S&P +0.06%, Nasdaq +0.06%, Russell +0.43%

- Last Week: Dow +0.72%, S&P +0.28%, Nasdaq +0.21%, Russell +0.34%

- Month-to-date: Dow +4.99%, S&P +6.52%, Nasdaq +6.77%, Russell +8.99%

- Quarter-to-date: Dow +7.11%, S&P +10.19%, Nasdaq +12.61%, Russell +17.19%

- Year-to-date: Dow +10.81%, S&P +12.77%, Nasdaq +17.54%, Russell +26.7%

- Sector Performance mixed (5 sectors up, 4 down) - Financials +0.88%, Tech +0.20%, Industrials +0.17%, Materials +0.16%, Utilities +0.06%, Healthcare (0.19%), Consumer Discretionary (0.29%), Energy (0.36%), and Consumer Staples (0.48%)

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: +320 (+439)

- VOLUME: NYSE 467.57 (-24.03%) - worst snow storm in six decades

- VIX: 17.67 +7.29% YTD PERFORMANCE: -18.50% (up 13.89% last two days)

- SPX PUT/CALL RATIO: 2.06 from 1.96 (+5.25%)

CREDIT/ECONOMIC MARKET LOOK:

Treasuries were mixed, nearly unchanged at the short-end, with 7bps narrowing of the 2/30 spread; 10-yr yield fell 6bps to 3.33%.

The Treasury auctioned $29B in 3-mo bills at 0.18%, up from the prior week, as well as $35B in 2-yr notes at 0.74%.

- TED SPREAD: 14.76 -2.943 (-16.621%)

- 3-MONTH T-BILL YIELD: 0.17% +0.02%

- YIELD CURVE: 2.65 from 2.74

COMMODITY/GROWTH EXPECTATION:

- CRB: 329.11 -0.08% (up 1.81% last week)

- Oil: 91.00 -0.56% Trading flat in the am - near a two year high

- COPPER: 428.00 +0.50% Trading up slightly in the AM

- GOLD: 1,379.60 -0.30% Trading up 1% in the AM

CURRENCIES:

- EURO: 1.3131 +0.07% - Trading up 0.75% in the AM

- DOLLAR: 80.366 -0.13% Trading down 0.57% in the AM - a two week low vs the EURO

EUROPEAN MARKETS:

- European Markets: FTSE 100: closed; DAX: +0.1%; CAC 40: +0.3%

- In thin trade again, Europe is trading slightly higher today, with auto stocks dragging on markets as they did yesterday on continued worries about the effects of China's rate hike and Beijing's new limits on cars.

- The UK remains closed until tomorrow.

- Basel Committee on Banking Supervision tells banks to be more transparent about pay, bonuses

- France Q3 GDP revised to +0.3% q/q vs preliminary +0.4%

ASIAN MARKTES:

- Asian markets were mixed this morning.

- South Korea went up 0.55% on construction and tech stocks. Hyundai Elevator soared by its 15% daily limit for a second straight day in response to Schindler Deutschland’s raising its stake in the company.

- Japan fell 0.61% on a stronger yen and weakness in China, though it was supported by strong industrial output data.

- Securities firms led China down 1.74% on fears that tightening measures are not over.

- Property stocks and banks fell in Hong Kong, which was closed yesterday, in reaction to the 25-Dec interest-rate rise in China. Carmakers extended their December 24th decline due to Beijing’s announcement that it would limit new-car registrations in the city.

- Australia and New Zealand were closed for Christmas.

- Japan November core CPI (0.5%) y/y vs cons (0.6%) - Jobless rate 5.1%, matching consensus and prior - Industrial output +1.0% m/m, matching expectations - Retail sales +1.3% y/y - Household spending (0.4%) y/y - Household incomes +0.5% y/y - Tokyo December core CPI (0.4%), matching expectations.

- Beijing raises minimum wage rate by 21%