“One can find so many pains when the rain is falling.”

-John Steinbeck

Timing is everything in life. As it relates to my current trip to Southern California, my timing couldn’t have been worse. I took a few hours away from the screens yesterday to finish up my Christmas shopping and a number of local business people informed me that this was one of the rainiest weeks Los Angeles had seen in, well, a really long time.

Today Keith is off to his hometown of Thunder Bay, Ontario with his wife and little ones, Jack (already a heck of an ice skater at only three years old) and Callie. Tomorrow I’ll head to my hometown, the small Alberta prairie outpost of Bassano, Alberta (total population of 1,200 and 75 some dogs). I think both of us, like many of you I’m sure, will take the next week to relax and begin planning for 2011. Much to the Steinbeck quote above, as I contemplate the future on this dark wet California morning, I do see a few pains.

While Steinbeck is most known for his literary career which culminated in the Nobel Prize for literature in 1962, he also knew a thing or two about state and local finances in California. In fact, his father was the long serving Treasurer of Monterey County.

California has become the poster child for one of the key potential pain points heading into 2011, that of municipal debt and deficits. We recently shorted municipal bonds in our Virtual Portfolio via the etf, MUB. While clearly not all municipal bonds are created equally, the general short case for the municipal bond market is as follows:

1. Rates are going higher – We’ve obviously already seen this over the last 30-days, but as the Fed is unable to keep the long end of the curve down, bonds will continue to suffer, especially as inflation expectations accelerate. Rates, obviously, have much more room to the upside from these historically low levels.

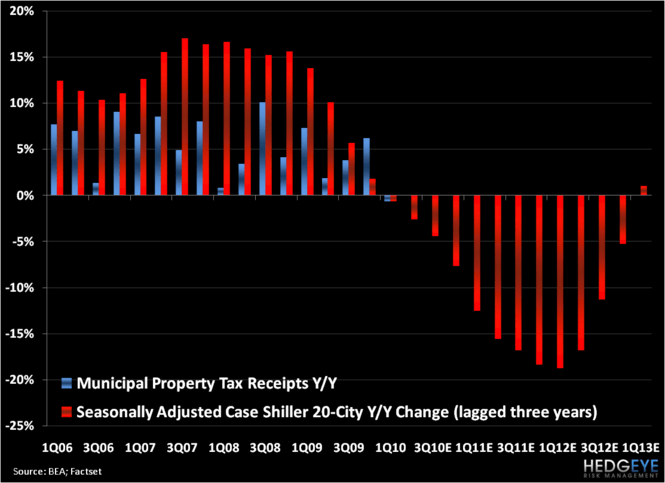

2. Housing prices have more downside – We are bearish on housing prices to the tune that we think home prices have 15 – 30% more downside nationally. Since appraisals for tax purposes operate on a 2 – 3 year lag to market prices, municipalities will begin collecting taxes based on dramatically declining home prices, which should hurt their tax receipts. Real estate taxes are the single largest revenue source for local governments. In the Chart of the Day, we show the Case-Shiller index versus property tax receipts.

3. State deficits set to expand – Currently, state level revenue is 12% below pre-recession levels, which is substantially worse than the revenue recovery in the past three recessions going back to the 1980 – 81 recession. This pain is likely to intensify, with States facing a $140 billion budget gap in fiscal 2011, according to the Center of Budget and Policy Priorities.

This is obviously the cliff notes version of our body of work on the municipal market, so if are a subscriber or prospective subscriber and would like more information, or to set up a call to discuss this topic with us, please email our Head of Sales Jen Ken at .

While Steinbeck has become one of America’s most lauded authors, he was also, while alive, one of its most controversial. He had left leaning politics and was long suspected to have ties to the Communist Party. In fact, perhaps his greatest work, The Grapes of Wrath, which is considered by almost all as one of the top ten English language novels of the last century, was originally harshly critiqued because it was deemed to be too pro-worker and overly critical of capitalism.

In addition to his full-time career of writing, Steinbeck was also a very active traveler. In 1947, he travelled to the Soviet Union with noted photographer Robert Capa. They were two of the first Westerners to visit the Soviet Union after the Communist Revolution. The output of this trip was A Russian Journal, which describe the harsh living conditions in the Soviet Union.

Since Steinbeck’s visit almost 60-years ago, much has changed in the former Soviet Union. While the transition to a fully functioning democracy in the vein of the West is still a work in progress, the introduction of capitalistic ways has certainly benefitted Russia, particularly as it relates to its vast natural resources. Due to modern reinvestment and the opening of her oil fields, since 1999 Russian oil production has increased 62%, or 3.5MM barrels per day, while total global oil production has only increased 10.5%, or 7.6MM barrels per day. The Russians are taking market share.

Despite the pain we see in municipal debt markets headed into 2011, we do have some great long ideas. As it relates to the Russian oil theme above, one of our favorite long ideas is Lukoil (LUKOY). According to our Energy Sector Head Lou Gagliardi:

“Although labeled a National Oil Company (NOC), Lukoil is 100% publicly owned. But, geopolitical risk, the Russian economy, a weak global economy and energy demand, and an onerous export tax duty have all weighted heavily on Lukoil’s share price in 2010 widening its market price discount to its discounted cash flow valuation further to 50%.

Historically NOCs trade at a discount to cash flow valuations and Lukoil’s historical discount has been in the 30% range. We believe its market discount will narrow reverting to the mean in 2011 driven by several catalysts. Lukoil’s high oil production weighting of 87% levers its share price to higher crude prices; its long-lived reserves, its expanding production profile internationally, and its growing crude oil production profile of ~2% per annum will contribute to significant earnings growth in 2011.

Lukoil’s balance sheet is strong with a debt to capital ratio of ~16% and a net of cash ratio at ~12%, as the Company is living within its capital spending. At $85.00 crude oil in 2011, we expect Lukoil to easily beat consensus with a ~25% E.P.S increase from 2010 to $14.75/ADR. For 2011, NCF at $85/bbl is targeted at $8.4 billion, or $10.12/ADR. At $89.00/bbl, earnings would jump 35% from prior year to nearly $16.00/ADR, adding roughly another $1 B in NCF.”

To put it simply: Lukoil is cheap, growing, has deep reserves, and a pristine balance sheet.

While the outlook does seem a little cloudy and rainy, there are plenty of Lukoil type opportunities out on the horizon. Moreover, as another well know American literary figure Dolly Parton once sang:

“The way I see it, if you want the rainbow, you gotta put up with the rain.”

Enjoy the holidays with your families and stay out of the rain,

Daryl G. Jones

Managing Director