TODAY’S S&P 500 SET-UP - December 10, 2010

As we look at today’s set up for the S&P 500, the range is 35 points or -1.54% downside to 1214 and 1.30% upside to 1249. Equity futures are trading above fair value in the wake of yesterday's financial-led gains. Trading in Asia and Europe has proved mixed. To coincide with the start of China's Central Economic Work Conference, authorities have raised their bank reserve requirement. Today's data highlights include Dec preliminary U of M Consumer Confidence and Oct Trade Balance.

- Aastrom Biosciences (ASTM) to offer undisclosed amount of shares

- Borders Group (BGP): 16 stores to be closed in 4Q, in talks to refinance

- Capstead Mortgage (CMO) declares 4Q div 39c-shr

- Cypress Sharpridge Investments (CYS) to offer 10m shrs

- Esterline Technologies (ESL) sees FY11 EPS above est.

- Green Mountain Coffee Roasters (GMCR) sees 1Q EPS below est.

- National Semiconductor (NSM) sees 3Q rev. below est.

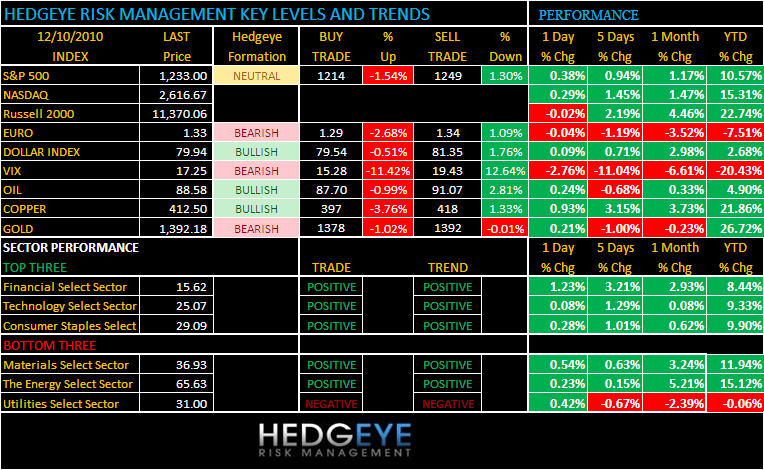

PERFORMANCE

- One day: Dow (0.02%), S&P +0.38%, Nasdaq +0.29%, Russell 2000 +0.47%

- Month-to-date: Dow +3.31%, S&P +4.44%, Nasdaq +4.47%, Russell +5.59%

- Quarter-to-date: Dow +5.39%, S&P +8.04%, Nasdaq +10.47%, Russell +13.53%

- Year-to-date: Dow +9.03%, S&P +10.57%, Nasdaq +15.31%, Russell +22.74%

- Sector Performance: Financials +1.3%, Telecom +1.1%, Materials +0.4%, Consumer Spls +0.4%, Utilities +0.3%, Energy +0.3%, Industrials +0.2%, Healthcare +0.2%, Tech 0.00%, Consumer Disc (0.02%)

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 354 (+1039)

- VOLUME: NYSE 1004.27 (-8.10%)

- VIX: 17.25 -2.76% YTD PERFORMANCE: -20.43%

- SPX PUT/CALL RATIO: 1.33 from 2.05 -35.21%

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 16.83 0.102 (0.607%)

- 3-MONTH T-BILL YIELD: 0.14% -0.01%

- YIELD CURVE: 2.59 from 2.63

COMMODITY/GROWTH EXPECTATION:

- CRB: 316.09 -0.25%

- Oil: 88.65 +0.10%

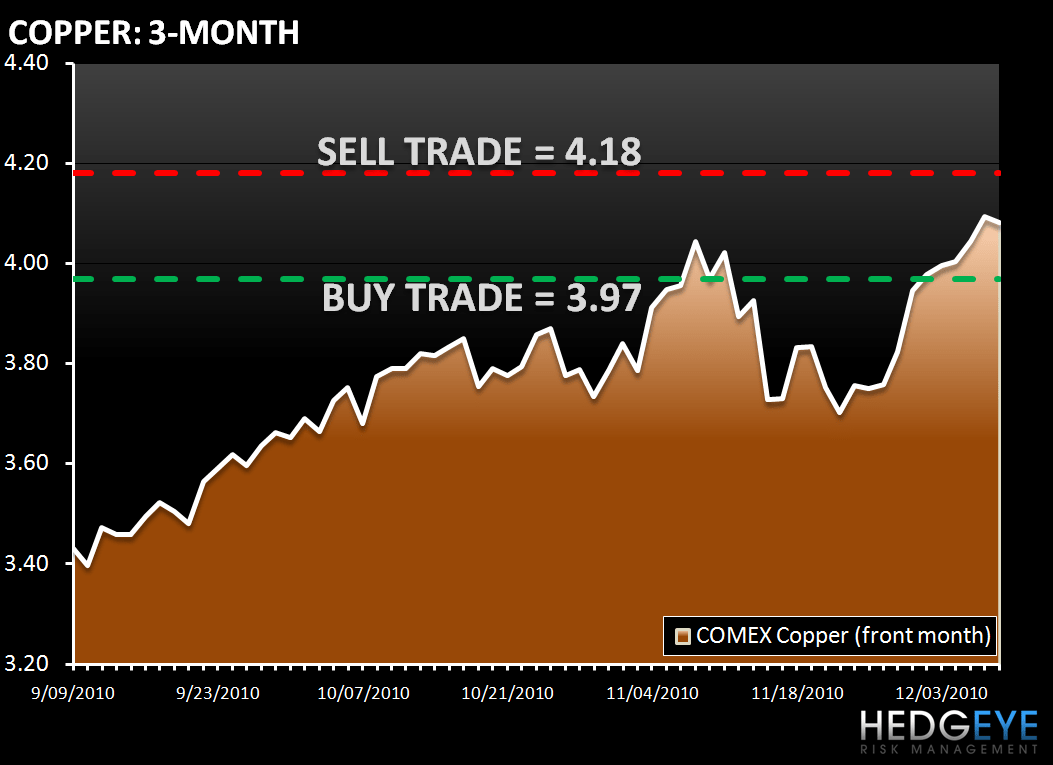

- COPPER: 408.70 -0.33%

- GOLD: 1,389.30 +0.53%

CURRENCIES:

- EURO: 1.3222 -0.04%

- DOLLAR: 80.069 +0.09%

OVERSEAS MARKETS:

EUROPEAN MARKETS:

- European markets trade mixed to higher with peripheral markets lagging.

- The FTSE100 mainly fluctuated in a narrow range either side of unchanged, while the DAX and CAC have extended early gains to trade near session highs.

- Chinese trade data underlined the strength in its economy.

- President Sarkozy and Chancellor Merkel are meeting to discuss the EuroZone crisis ahead of next week's EU Summit.

- Germany Nov Wholesale Price Index +7.8% y/y vs prior +7.7%

- France Oct Industrial Production (0.8%) m/m vs con +0.3%

- UK Nov Core PPI +3.3% y/y vs con +3.5% and prior revised +3.2%

ASIAN MARKTES:

- Most Asian markets went down today as strong trade figures from China exacerbated fears that the country will raise interest rates.

- China rose on its trade figure, though volume remained tepid

- China increased bank reserve ratios

- Australia finished flat as gains in banks balanced out declines by miners.

- Hong Kong finished flat, but Chinese property stocks fell on worries about interest rates.

- Taiwan fell 0.40%

- Japan rose 1% early, but quickly reversed course on profit-taking, having reached a seven-month high.

- McDonald’s Holdings (Japan) fell 2% on lower November comps

- Japan November corporate goods price index +0.9% y/y. Q4 large-company sentiment (5.0) vs 7.1 seq. November consumer confidence 40.4, +0.9 pts y/y, (0.5 pts) seq.

- China November trade surplus $22.90B vs $22.3B survey.

Howard Penney

Managing Director