Position: Long Germany (EWG); Short Euro (FXE), Short Italy (EWI), Short Spain (EWP)

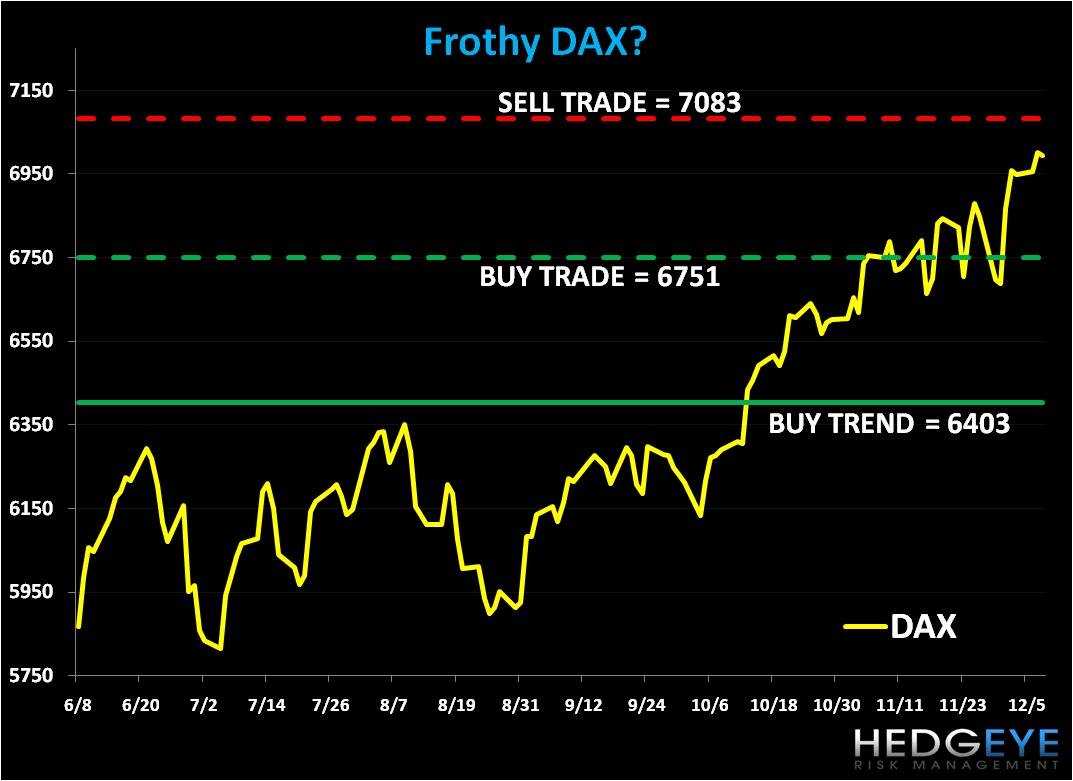

Germany’s fundamentals and capital markets continue to signal a positive divergence versus most of its European peers, however we caution that the DAX is approaching an immediate term TRADE overbought level (see chart below).

From a fundamental standpoint we continue to emphasize just how important Germany’s fiscal conservatism is as a differentiating factor versus its debt and deficit laden peers, the PIIGS in particular, which we believe has contributed to its equity outperformance (chart below).

Germany’s deficit is projected at 3.7% of GDP this year, according to the German Finance Ministry, with public debt at 75.5%. In comparison, most PIIGS are pushing deficit-to-GDP levels near low double digit figures with debt-to-GDP near or above 100%. As Reinhart and Rogoff examine in their work “This Time Is Different”, which examines sovereign default over the last 800 years, there are two important metrics used to indicate when a government is reaching the crisis zone of fiscal imbalance: debt-to-GDP north of 90% and deficit-to-GDP north of 10%.

It therefore comes with no great surprise that based on YTD equity performance alone, the market is rewarding those countries that have not violated these critical fiscal levels. Germany is certainly one standout. On the credit side, we continue to see elevated yields (though off their highs) for the PIIGS. As we noted in previous works, despite the bailouts of Greece and Ireland, we expect yields to remain elevated over the intermediate to longer term as the Sovereign Debt Dichotomy plays out in Europe, which will further hamstring peripheral countries that require debt servicing to meet their fiscal imbalances.

German Data

Returning to German fundamentals, the data (while admittedly a bit stale), presents a positive picture.

German Industrial Production reported today showed a +11.7% year-over-year gain in October, or +2.0% gain over the previous month. Reported yesterday, German Factory Orders rose +1.6% in October month-over-month, or +17.9% year-over-year. Here we’d note the comp of -8.2% in October 2009, and caution that comparisons will get more difficult into year-end (see chart).

German Export and Import figures for October were also released today and showed a contraction in Exports of -1.1% in October month-over-month, while Imports rose +0.3% versus the previous month. Despite the “wet Kleenex” for October exports, Germany’s exporting base looks poised to remain strong into year-end.

Further, German consumer and business confidence surveys have looked strong over recent months, as has Manufacturing and Services PMI, bolstered by an unemployment picture that has improved nearly every month over the last year. Unemployment currently stands at 7.5% in Germany versus 10.1% in the Eurozone or such extremes at 20.7% in Spain or 13.6% in Ireland.

The German Economic Ministry recently revised its GDP forecasts up to 3.4% in 2010 and 1.8% in 2011. For comparison, the only other countries that will see growth in this area code in Europe are: Poland 3.20% in 2010 and 3.50% in 2011; and Sweden 4.35% in 2010 and 3.15% in 2011, according to Bloomberg estimates.

Today we shorted Spain (via the etf EWP) in the Hedgeye Virtual Portfolio with the IBEX 35 rebounding off another dead-cat bounce. Spain remains broken on immediate TRADE and intermediate term TREND durations, and we believe will likely be the on the near horizon to need European and international assistance to contain its fiscal imbalances.

Matthew Hedrick

Analyst