This note was originally published at 8am this morning, December 07, 2010. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Everyone has a plan 'till they get punched in the mouth.”

- Mike Tyson

There have been a lot of interesting Mike Tyson quotes over the years, some fit for print, others less so, but this one seems apropos for the times. The Fed tells us they have a plan, and they’re implementing it. So far, the markets seem to like it. Let’s see how their plan fares once they get punched in the mouth.

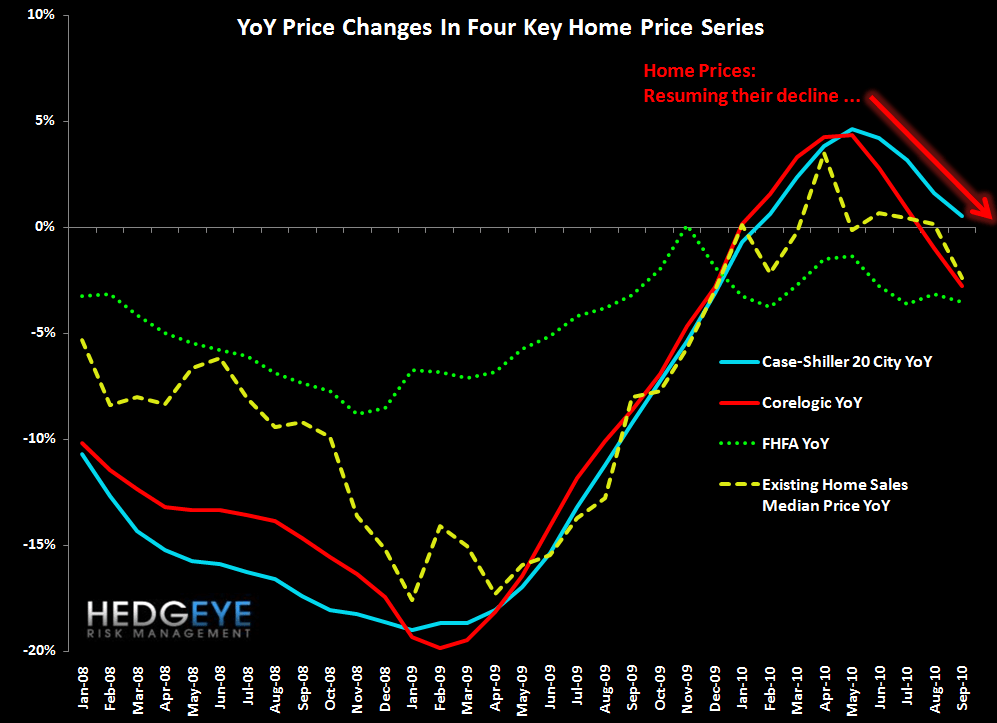

This summer we introduced our bearish thesis on housing with our 100-page report entitled: “How Low Will Housing Go in 2H10 and 2011”. In that report we laid out our three separate home price models: our supply model, our demand model, and our combination supply & demand model. The output of those models forecast home price declines ranging from high single digits to 20%+ over the next 12-18 months. How have we fared so far? As the chart at the end of this note shows, the four major home price series that we track (Case-Shiller 20 City, Corelogic, FHFA, and Existing Home Sales Median Home Price) are all heading south. After peaking in the April/May timeframe on the strength of the tax credit, three out of four home price series are now solidly in negative year-over-year territory. The lone holdout, Case-Shiller, is a 3-month rolling average, which is why it lags the other series in reflecting the degree of slowdown. The next few months of Case-Shiller data will show a comparable negative trend.

For reference, the Corelogic series is the series now used by the Federal Reserve. How has the Fed’s preferred series fared? According to Corelogic, home prices have rolled from being up +4.3% YoY in May 2010 to being down -2.8% YoY in September 2010, a negative -7.1% swing in four months. Looking month-over-month, the Corelogic series was down -1.8% sequentially in September (the most recent data available), which translates to the fastest rate of decline since February 2009.

The supply and demand imbalances were at the root of our housing call this past summer and nothing has changed on that front. The market is more dislocated today than it was when we made the call in the summer. At the time we made our call in June there were 3.99 million homes on the market for sale and existing home sales were running at a rate of 5.37 million, which equated to 8.9 months of supply. Today, there are 3.86 million home on the market for sale (October), while existing home sales are running at a rate of 4.43 million, which equates to 10.5 months of supply. Existing home inventory peaked at 12.5 months of supply in July. Based on our conclusion that home prices take one year to fully respond to supply and demand imbalances, we would expect to see July 2011 be the low watermark for year-over-year price trends in housing. The more important takeaway, however, is that between now and July 2011 the trends should continue to get worse. While it is possible that the market’s “bad news is good news” mentality will persist and ongoing weakening in home prices will simply translate into greater and greater expectations for further quantitative easing, we continue to think that bad news is simply bad.

Another point to consider is the impact QE2 is having on the housing market. While recent demand statistics have been modestly upbeat (i.e. October pending home sales up 10.4% month-over-month), the reality is that mortgage rates have backed up sharply in November. The Bankrate 30-year conforming mortgage index has ballooned from 4.20% a month ago to 4.70% yesterday. For reference, a 50 bp backup in 30-year rates has a 5% negative effect on affordability.

It’s also worth pointing out that no amount of stimulus or quantitative easing seems to increase banks’ willingness to underwrite residential mortgage loans. In the most recent Senior Loan Officer Survey released November 8, the net percentage of lenders tightening access to prime mortgage credit rose to +9.3% from -5.5% quarter over quarter meaning that the average American is now finding it more difficult to get a mortgage than they were over the summer. The trend was similar for access to nontraditional mortgage credit: +9.5% of respondents reported tightening standards, up from +4.5% last quarter. This isn’t helped by the fact that banks are currently engaged in trench warfare with Fannie & Freddie as well as the entire private-label MBS universe over mortgage putbacks. Further, there are 8.5 million borrowers who have either been foreclosed or are currently non-performing on their loan. This is a large slice of the overall homeownership pie that has been semi-permanently eliminated from the buyer pool (7 years for most lenders to look past a mortgage default). All of this has cast a pall over banks’ willingness to underwrite new mortgages.

Many investors forget just how slippery the slope of negative home prices can be. Falling prices don’t happen in a vacuum: they have two insidious offshoots. First, they generate a tangible negative wealth effect. For reference, for all the excitement resulting from the upward move in equities recently, consider that as a rough rule of thumb, every 100 points of upside in the S&P is roughly equivalent to a 5-6% rise in home prices based on there being total direct equity wealth of $10.8 trillion and total residential housing wealth of $17.1 trillion. That said, the wealth associated with housing is much more broadly felt as 65% of American families are homeowners, a far higher proportion than those with material equity wealth. Second, negative home price trends increase pools of underwater borrowers. We have shown that there are presently 11.3 million borrowers (20% of all borrowers) who are underwater. 4.9 million of whom are underwater by more than 25%. A 20% decline in home prices from here would increase those who are underwater to 21.9 million (46% of all borrowers) and those underwater by 25% or more would rise to 9.4 million (20% of all borrowers). Laurie Goodman, a Senior Managing Director with Amherst Securities, one of the leading providers of mortgage data analytics, has shown that loans with LTVs greater than 120% are currently defaulting at an annualized rate of 19.1%, while those with LTVs between 100-120% are defaulting at an annualized rate of 11.3%. Those are scary statistics when one considers that there could be 22 million borrowers in a negative equity position with a 20% drop in home prices from here.

The real question is, what will a 20% drop in home prices feel like for the markets and for the consumer? Our guess is that it will feel a lot like getting punched in the face by Mike Tyson.

Josh Steiner

Managing Director