PSS’s Q3 results came in strong at $0.69 (less $0.06 tax benefit) vs. $0.51E and even better than our above consensus expectations at $0.60. We’re not going to rehash all the puts and takes of the quarter. But the meat of it is that comps at Payless improved on the margin. The bears will point to high inventories. As always, the company gave both side of the trade something to hang their hats on.

Comps: The directional change was something we fully expected. Keep in mind that…

a) PSS was not on trend last year with the rapid shift towards boots in the fall of ’09. It goes without saying that boots are the highest ticket footwear units in the store.

b) Same goes for toning. PSS sat there and watched companies like Sketchers, Reebok, New Balance and Avia jump into the category once owned by MBT. Due to the nature of PSS’ model, it will catch fashion trends after the peak in the bell curve. What’s in the stores now? Toners and boots – and at 2x the price point of PSS core.

c) Remember last fall when PSS went in to Back-to-School with a $8.99 price point? That’s as low a price point ANY shoe retailer (incl WMT) has ever seen. The reality, however, is that the consumer did not show up regardless. The kicker is that PSS also paid up in heavy SG&A spending to support the initiative. You can complain that it was a failed initiative, but the reality is that now they’re comping that.

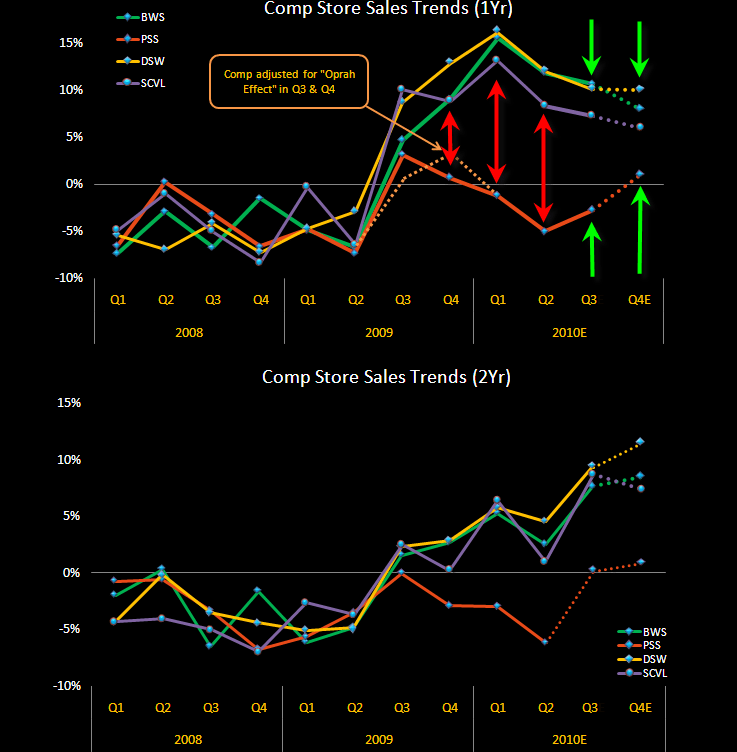

d) Ultimately, the material divergence between PSS comps and peers contracted for the first time in 5 quarters. The chart below captures it all. It’s worth noting this has been one of the primary factors that bears have pointed to over the past year (and they’ve been dead on), but that trend has now turned considerably more positive on the margin.

Inventories: Margins came in up +130bps above expectations with less promotional activity and favorable Oprah compares offset in part by higher freight costs. But inventories came in high – very high. And let’s not mince words – for a zero-square footage growth retailer, +22% inventory is ugly. We can chalk up some of it due to…

- Remember that the company flat-out ran out of product last year during the ‘Oprah Event.’

- On the margin, PSS is bringing in higher priced product.

- PLG remains exceptionally strong, and was low on inventory last year. In addition there is a slight impact from PLG store growth.

- Rubel himself admitted that clearing inventory is not a 1-quarter process. It’s also worth noting that despite higher inventories, margins didn’t contract on a sequential basis like it did for all other footwear retailers. Does that mean that the gross margin hit is yet to come? Perhaps. But like it or not – inventories have been too low for this company to comp on a unit basis for the better part of 3-years. Based on all the feedback and sentiment we’re hit with daily, our sense is that trading slightly lower gross margins in favor of comp would be bullish here.