“If I shoot at the sun, I may hit a star.”

-P.T. Barnum

Yesterday we held our quarterly company meeting in New Haven, Connecticut. After Keith gave the opening remarks, we spent the next five hours having various leaders from within the firm talk about their business units. This was an opportunity for us to reflect on what went right and wrong in 2010, what we need to do in 2011 to continue to take market share, and to share best practices amongst colleagues. As I engaged with my teammates yesterday and watched their passion, one thought struck me repeatedly -- capitalism is alive and well in America.

Ironically, while going through the daily macro grind this morning, I happened upon a quote from another Connecticut capitalist, P.T. Barnum. Now, admittedly, P.T. wasn’t in the securities or research business, he was in the carnival business. Specifically, he started “P.T. Barnum’s Grand Travelling Museum, Menagerie, Caravan & Hippodrome”, which would eventually be coined as the “Greatest Show on Earth”. Barnum’s circus eventually became so successful that he purchased his own train to transport it in the late 1880s.

While we don’t have any Tom Thumb like characters walking through our offices in New Haven (who Barnum billed as the smallest person to walk alone), we do enjoy moments of levity at work as we look out at the Global Macro Three-Ring Circus every morning.

In the Geopolitical Ring this morning, we have Secretary of State Hilary Clinton. Just when it seemed that the news flow could get no worse for the Obama administration following the mercy crushing of the Democrats in the midterms (losing 63 seats in the House), we have one of the leaders of global transparency, WikiLeaks founder Julian Assange, taking aim at the State Department.

The most egregious foreign affairs circus act appears to have been spying at United Nations ordered by Secretary Clinton. According to a news report:

“Secretary of State Hillary Rodham Clinton ordered State Department employees to gather private information from high-ranking officials, including the United Nations Secretary-General Ban Ki-Moon, Security Council members’ ambassadors (including our allies, France and Britain, as well as China and Russia), prominent African military and political leaders and top UN directors.”

Obviously, this is not exactly helpful as the United States tries to rally support to contain North Korea.

In the Inflation Ring this morning, we have China front and center again. According to reports, China’s gold imports jumped almost 5x year-over-year in just the first 10 months of 2010. Since the Chinese central bank has to approve all gold imports, this is a direct signal as to their thoughts on inflation and the direction of the U.S. dollar. Like many commodities, even those with a less practical use like gold, China continues to be the key driver of incremental demand. Chinese investment gold demand is expected to reach 150 tons this year, up from 105 last year and 3 to 4 tons 10 years ago.

The fact that the Chinese are hoarding gold as a hedge against inflation should be no surprise given some recent inflationary data points out of China. The most noteworthy of which was October CPI, which was at a two year high of 4.4% year-over-year. Inflation and subsequent tightening of monetary policy in China continue to be the key factors that drive our view that global growth will slow into the first half of 2011.

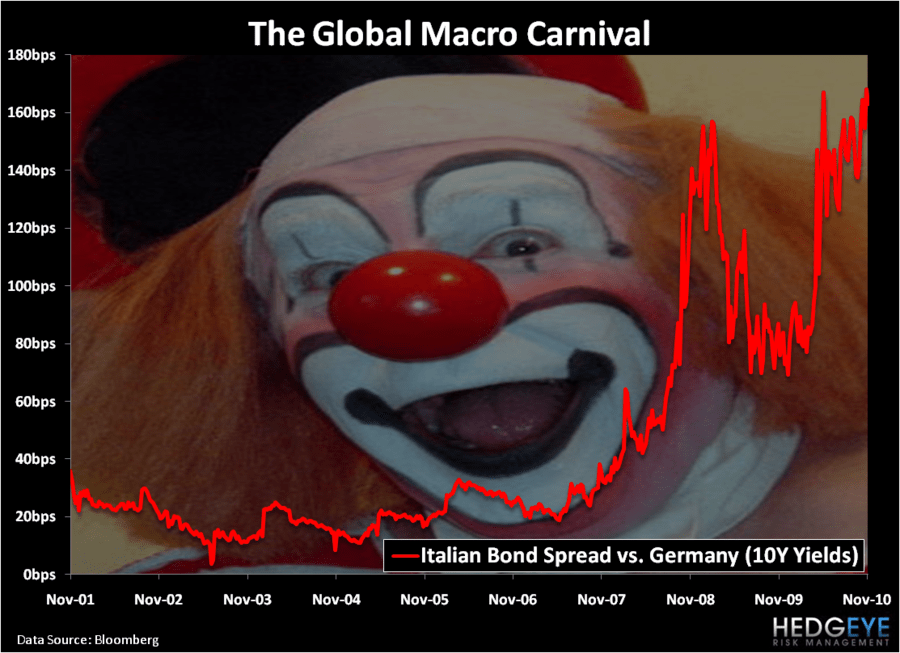

Finally, in the Sovereign Debt Ring, the PIIGS continue to be the main act in Europe. This morning Spain auctioned 2.5 billion Euros in notes with an average yield of 3.7% and a bid to cover of 2.3x. While the Spanish IBEX is up 2% on this news, the act of adding more debt to the Spanish balance sheet is far from a reason to celebrate. In fact, as of November 30th the spread of Spain’s 10-year debt over comparable German bunds climbed to an all time high.

Most pertinent, of course, are the long term and structural unemployment issues in Spain. Yesterday, our European Analyst Matt Hedrick wrote a note to our subscribers that highlighted Spain’s unemployment rate of 20.7%. No, that was not a typo, a full fifth of Spain’s employable adults are out of work. The second highest unemployment rate in the Eurozone is Ireland, which is currently at 13.5%. While the equity markets are giving Spain a golf clap this morning, to think the structural economic issues in Spain have gone away are laughable at best.

While P.T. Barnum passed away well over a century ago, his famous quote, “there’s a sucker born every minute”, continues to have relevance today . . . especially for those folks who are buying Spanish government bonds today.

Keep your head up and stick on the ice,

Daryl G. Jones

Managing Director