Below is a complimentary Demography Unplugged research note written by Hedgeye Demography analyst Neil Howe. Click here to learn more and subscribe.

|

Why are market forecasters doing so badly? Soaring equity indexes next to basement long bond yields seem to be making nonsense of all the tried-and-true rules for assessing "likely price trends," compelling Old Wall gurus to widen their bullish-and-bearish targets or just give up prognosticating altogether. (Bloomberg Businessweek) |

NH: If you had told most veteran traders in March of 2020 that the S&P500 would double from its all-time low (on March 23) in only 354 trading days--by far the fastest doubling of the post-World War II era--they would have been skeptical.

If you had told them, in addition, that the market would maintain nearly all those gains after 18 months despite 2,000 pandemic deaths per day and employment still lagging some 5% below its pre-pandemic level, well, they would have thrown you out of the room.

Let's face it: This has been a humbling time for anybody who thought they knew anything about where markets would go.

Not only did the SPY double from its low on August 16, but last Thursday we celebrated another remarkable milestone: the 40th anniversary of the bond bull market.

On September 30, 1981, 10-year Treasuries closed at their all-time high, 15.84%. And it has been a long (if sometimes rocky) road downhill ever since. This too seems to defy all expectations, since the current yield is now not only hundreds of bps below current YoY inflation but roughly 90 bps below the inflation that bond investors themselves expect over the next decade. Even more befuddling: All this comes amid a bullish-ever year for stocks and a YoY acceleration in GDP.

This too we once considered impossible.

What other conventional nostrums seem to be getting annihilated? Well, just think about all those S&P500 valuation rules that long-term investors like to use to keep themselves grounded: indicators like Shiller's PE or price/sales or price/book or market cap/GDP (the so-called "Buffett Indicator"). John Hussman has for years been curating a sophisticated lineup of these metrics.

Here's my point: All of these measures have been screaming sell for at least the past year. But if you had traded on them, you would have been killed.

There are two ways out of this box. The first is to de-emphasize "absolute" valuation measures altogether and to approach the market as a short- to medium-term response to real and nominal accelerators. Fortunately, that is the approach we typically use at Hedgeye.

But for long-term investors who insist on objective rules, there may be another way out. That is simply to realize that all such rules are regime dependent. In other words, what works for one regime won't work for another. And recently we have been moving from one regime to another.

The Two Regimes

Let's define the old regime as neoliberal. The central bank's pursuit of macroeconomic stability is limited to intervention in short-term public securities, and its response to market panics is limited to the old Bagehot rule. The federal government keeps the budget close to balance over the business cycle--since it cannot expect the Fed to bail it out if it doesn't. The old valuation rules worked pretty well under the old regime.

Let's define the new regime as MMT, in practice if not (yet) in name. The central bank pursues full employment and blocks market downturns by buying any asset at any maturity pretty much without limit. And the federal government can raise spending or cut taxes at its pleasure since it counts on the Fed to monetize its excesses. The old rules don't work under the new regime.

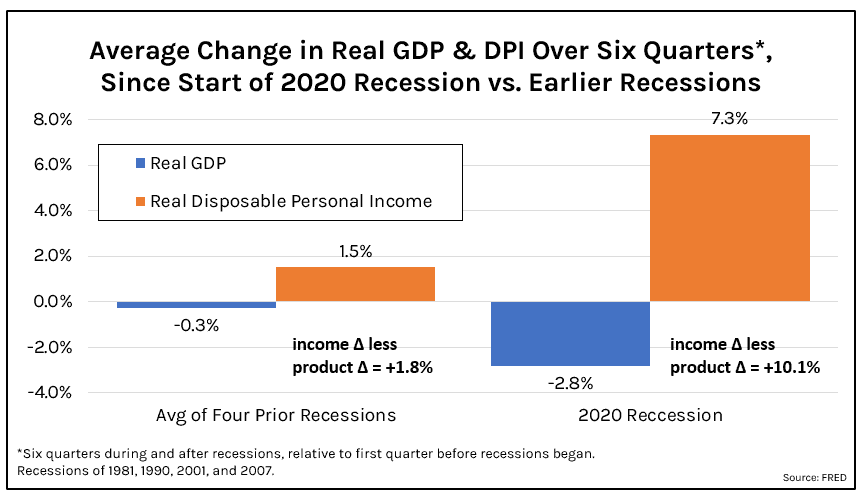

Why? Because it makes possible the sort of alchemy that could never happen under the old regime. Consider that real GDP, in the 6 quarters since the pandemic started, has averaged -2.8% relative to its last pre-pandemic quarter. No mystery here: We did, after all, go through a global recession. Real personal disposable income, on the other hand, has averaged +7.3% relative to its last pre-pandemic quarter.

Not only have Americans been living beyond their national income by roughly 10% over the past year and a half, they've been living over 7% better than if there had been no pandemic at all.

Since 1960, in fact, Americans have never enjoyed anything close to this growth in real disposable income over any six quarters--starting at any moment in the business cycle.

We accomplished this, of course, by massive federal borrowing. In FY 2019, before the pandemic, the federal government was already running a deficit of nearly 5% of GDP (an all-time record for a peacetime economy at full employment). Over the next two years, we jacked that up to roughly 12.5% of GDP. So that's an extra deficit kicker of +7.5% of GDP--which translates into about 10% of personal disposable income.

So that's one way the new regime behaves differently. In the past, it would have very difficult to add an extra 10% onto our real disposable income by debiting it from our national balance sheet. Now it's effortless. From 2007 to 2021, the publicly held federal debt has risen from 35% to 103% of GDP, with nearly a third of that borrowed in the last three years.

But that's not the only innovation. Sure, the Fed made this sleight of hand seem effortless by monetizing most of that extra borrowing. But by buying down yields across all maturities and risk premia--and by promising to keep them down indefinitely--the Fed stoked a further speculative frenzy. With almost every nominal yield running under the inflation rate and with market volatility suppressed, borrowing to buy almost anything became a slam dunk.

Amazingly, corporate buybacks (led by Big Tech) surged in Q1, even as Covid deaths hit record highs and GDP was still underwater. In Q3, buybacks may be hitting an all-time high at nearly $1T (annualized). Rising leverage and falling equity risk premia can keep equity indexes rising regardless of the condition of the underlying economy.

The New Endgame: Inflation

Yet maybe it's not quite accurate to say the old rules don't work under the new regime. After all, you can't simply banish the concept of valuation. It would be more accurate to say that the old rules don't work in the same way under the new regime. They used to work directly and relatively swiftly. Today, they still work--but indirectly and with a lag.

The name of that indirect route: inflation. Quite simply, rising inflation expectations lower the boom on the entire MMT credit factory (even MMT proponents admit as much). And they do so in a particularly harsh and unforgiving manner. The first to change course is the Fed. Once it can no longer pretend that rising prices are "temporary" and once yields trend clearly upwards, the Fed has no choice. Taper tantrum or not, all the QE largesse will begin to contract, the long end will rise, and ultimately the short end will rise as well.

Rising yields won't just raise the discount rate on equities. It will de-leverage markets by toppling debt pyramids across all asset classes, starting at the high-risk, high-leverage end.

Finally, and most destructive, is the fiscal aftershock. Never before have long-term federal deficit and debt projections been so precariously dependent on super-low long-term Treasury yields. The CBO currently assumes, despite full employment and large and growing deficits (as a share of GDP) through the 2020s, that the 10-year yield will remain well below the rate of the GDP growth. This assumption miraculously stabilizes the national debt until the early 2030s.

But let's say we change that assumption and shift yields up by 100 or 200 bps by the mid-2020s. Then the debt projection explodes. Instead of looking forward to debt at an (already unsustainable) 150% of GDP by 2040, we could be looking at 200% to 250% or more. (See "The (Dire) Fiscal Side of the CBO's 2021 Long-Term Forecast" and presentation.)

In this case, Congress--like the Fed--would have no choice. It would have to raise taxes or cut spending. Which means that fiscal contraction would compound the impact of monetary contraction.

Sure, it would be better for financial markets if the fiscal contraction were regressive. That way, inflation via personal consumption would be suppressed and investor returns held harmless. But in today's political climate, I have zero expectations that would happen.

Limited Options

There's only one way in which rising debt levels could result in unchanged income and consumption in future years. And that would be if productivity growth rose to cover the higher debt service.

That might result if, for example, all the borrowed funds--past and future--were being allocated to some sort of productivity-enhancing investment. But that hasn't happened and isn't likely to happen in the foreseeable future.

The latest data on labor productivity show no break from the (lower) post-GFC trend. Yes, we're seeing a slight productivity surge, but no more than what happens after every recession due to the lingering shrinkage in employment. The output-per-hour gains post-2020 have thus far been less impressive than they were post-2009.

Beyond that, it's just a question of deciding how we want to confront our real income shortfall.

One option would be to raise taxes or reduce public spending on ourselves. You might call that the honest way. But I suspect fiscal tightening will come as a last resort, something we do under duress.

Another option would be for households to voluntarily save more in anticipation of the higher taxes they will someday pay, or the smaller benefits they will someday receive, as a result of the public borrowing. But almost no economist any longer believes in long-term "Ricardian equivalence" (as this assumption is called, in honor of the political economist David Ricardo). The fact is, Americans no longer care much about public debt. Even conservatives nowadays tend to agree with Dick Cheney: "Ronald Reagan proved that deficits don't matter."

Far more likely, we will confront our real income shortfall through price acceleration. As higher inflation becomes expected and incorporated into market returns, it will dis-inflate today's lofty market valuations--especially once the Fed has to push yields from well below inflation expectations to well above them.

But I don't see a replay of Fed Chairman Volcker's aggressive moves 40 years ago. Instead, I see policymakers raising rates as little as possible and tolerating as much new inflation as they dare.

So long as it doesn't slip out of control, after all, inflation solves several big problems--economic, fiscal, and social: It helps keeps the economy running "hot." It tends to reduce debt-to-GDP ratios over time. And it takes from creditors and gives to debtors, pulling down inequality. It also transfers a large share of our fiscal burden from Americans to foreigners (who hold over a third of that debt). America first, anyone?

Creditors may try to flee from Treasury debt, but if they do we should anticipate regulations preventing mainstream financial institutions from exercising that choice. Yes, I mean financial repression. Today's investors should plan ahead accordingly.

Those who bet against rising inflation are looking for a different scenario--in which Congress gridlocks over all the new spending programs, the remaining pandemic freebies dutifully sunset over the next three years, the Fed hikes as needed, and the economy reverts to its old disinflationary norm. In effect, the old regime returns and the old rules can still work.

That's a possibility. But I don't see the future playing out that way. Americans, IMO, are desperate for a system change. They are pushing both parties toward their populist edges. And they do not want a mere return to the status quo--however much that might please creditors.

There's no going back to the old regime. It's time for investors to figure out how to thrive in the new regime.

Lessons of History

Rather than look at what happened 40 years ago, let's look at what happened another 41 years before that. It was December 1940, and the 10-year Treasury yield hit not its highest but its lowest yield ever (that is, from 1880 until the GFC).

It was 1.95%. At that moment it seemed comfortably above the inflation rate, which was having trouble staying above zero in the wake of the demoralizing 1937 recession.

All that changed a couple of months later when Congress, alarmed by the fall of France and the precarious fate of Britain, began running large deficits in order to turn America into "an arsenal of democracy." By the fall of 1941, both employment and inflation were surging. By December of 1941 came declarations of war.

Thereafter, for the next 16 years, as inflation raced upwards during World War II, the postwar boom, and the Korean War, real yields were consistently negative, sometime catastrophically so. The U.S. Treasury, with Fed compliance, rarely allowed the 10-year to rise over 2.5%.

Even financial markets became another regulated "front in the war," and many large asset holders found themselves locked into these notes.

No one called it financial repression at the time. It just seemed like fair burden sharing. Americans were sacrificing through inflation, higher taxes, rationing, and service at the battle front. Why not exact a bit of extra sacrifice from creditors as well?

Looking back over the last 40 years, we tend to think history can only move in one direction: toward disinflation, lower rates, deregulation, greater inequality, and a cooler-running economy. Lest we forget: It can move for several decades in the opposite direction as well.

As for valuation measures, the problem isn't that they're wrong per se. It's that they work differently under different regimes. For the most part, they will continue to work under the new regime.

We just need to wait until all the rules of that regime, and their consequences, become fully operative.

| To view and search all NewsWires, reports, videos, and podcasts, visit Demography World. For help making full use of our archives, see this short tutorial. |

* * *

ABOUT NEIL HOWE

Neil Howe is a renowned authority on generations and social change in America. An acclaimed bestselling author and speaker, he is the nation's leading thinker on today's generations—who they are, what motivates them, and how they will shape America's future.

A historian, economist, and demographer, Howe is also a recognized authority on global aging, long-term fiscal policy, and migration. He is a senior associate to the Center for Strategic and International Studies (CSIS) in Washington, D.C., where he helps direct the CSIS Global Aging Initiative.

Howe has written over a dozen books on generations, demographic change, and fiscal policy, many of them with William Strauss. Howe and Strauss' first book, Generations is a history of America told as a sequence of generational biographies. Vice President Al Gore called it "the most stimulating book on American history that I have ever read" and sent a copy to every member of Congress. Newt Gingrich called it "an intellectual tour de force." Of their book, The Fourth Turning, The Boston Globe wrote, "If Howe and Strauss are right, they will take their place among the great American prophets."

Howe and Strauss originally coined the term "Millennial Generation" in 1991, and wrote the pioneering book on this generation, Millennials Rising. His work has been featured frequently in the media, including USA Today, CNN, the New York Times, and CBS' 60 Minutes.

Previously, with Peter G. Peterson, Howe co-authored On Borrowed Time, a pioneering call for budgetary reform and The Graying of the Great Powers with Richard Jackson.

Howe received his B.A. at U.C. Berkeley and later earned graduate degrees in economics and history from Yale University.