As we stated on earlier this week when we backed off our SFIX short into this print – if there was ever a time for SFIX to put up great numbers, this is the quarter to do it. Nearly every apparel company is smoking top line and gross margins, as we’re seeing the best selling environment for apparel in a generation. SFIX certainly didn’t disappoint, putting up $0.19 vs the Street at ($0.12) and our estimate of ($0.08). But that’s where the good news ends. Nearly everything we heard validates our concerns about this business model, the company strategy, and the long-term earnings power of the company. The stock is ripping after-hours to the high end of the Hedgeye Risk Range, and we’re subsequently taking this name higher on our Best Idea Short list. We said it when we made the short call at $79, and will say it again now…this stock is likely headed back to its mid-teen IPO price.

So what didn’t we like?

- First off, the quarter included a $0.17 per share benefit from reduced marketing expenses, which were pushed into 1Q. Adjusting for that the company barely broke even. Never good when a company beats a quarter due to reduced brand investment.

- Secondly, total net new customer additions were only 58k for the quarter, which is absolutely horrible. We were modeling 225k. We also saw a 4% boost in spending per customer vs our estimate of 5%. We won’t beat the company up on that one, as 4% is decent. But in this killer apparel environment where even low-quality retailers are beating on the top line, the combination of the two metrics is mediocre at best.

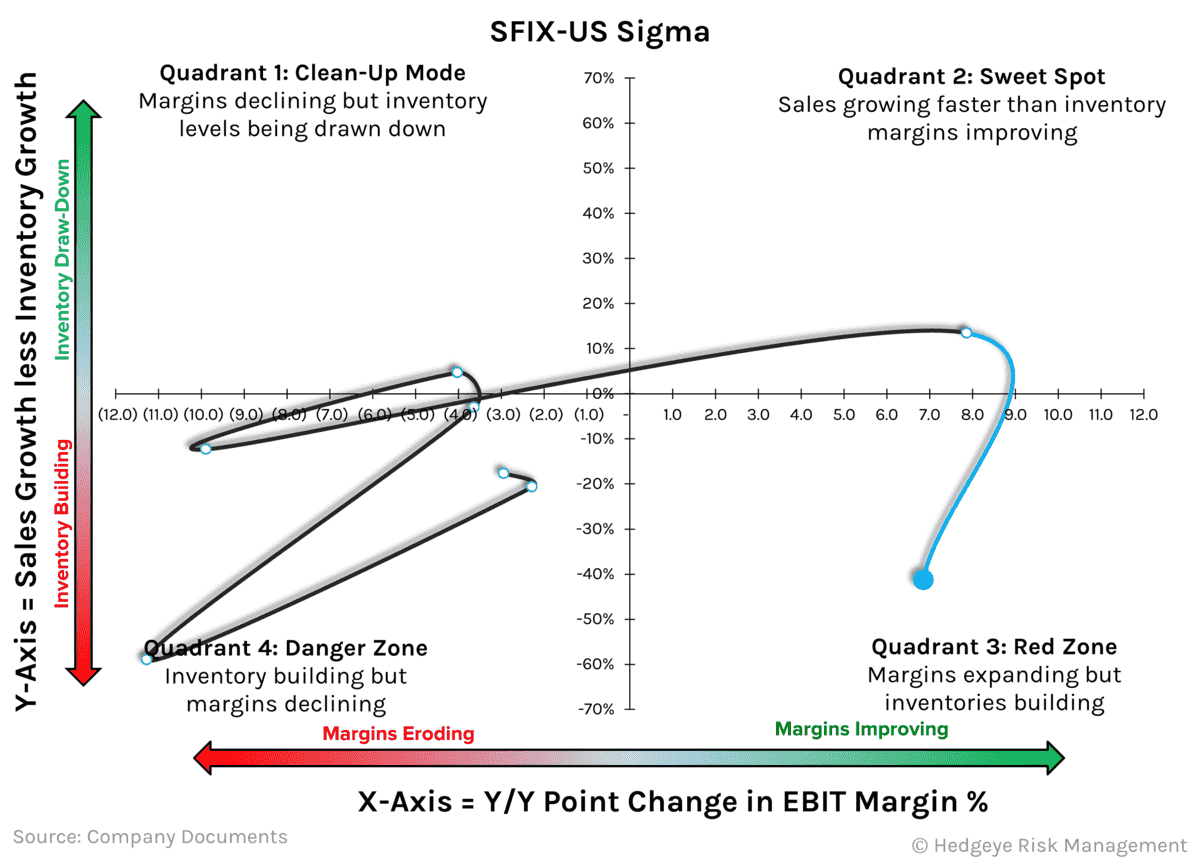

- Inventories for the quarter were up 70%. I repeat…70%. That’s on 29% sales growth. Guidance for the first quarter is for 14-17% revenue growth, and for the year it’s 15%+. Aside from a lower growth profile relative to what we’ve seen historically and vs 2020, that’s VERY gross margin bearish in the face of such high inventories. Check out the SIGMA chart…super beared-up.

- Operating cash flow went from $71mm in ’19 to $43mm ’20 and -$16mm in ’21 amidst the greatest apparel consumption landscape we’ve seen in generations. That’s the same time we’ve seen profitability off the charts for most retailers at completely unsustainable levels. If this does not tell you that the company has run out of TAM, then I don’t know what does. Most of the bulls we talk to on this name are tech investors – and whether they look at good ‘ol fashioned metrics like cash flow is debatable. But this trend is utterly staggering.

- Management guided revenue growth down to the teens vs the historical benchmark of 20%+. That’s in the face of the biggest initiative for the company – Freestyle, formerly known as Direct Buy – since it started its Fix offering. It’s cannibalizing its core with a more capital-intensive business. That’s one of our biggest sticking points with the company’s strategy. It ran out of TAM – which is a curated and customized stylist/AI-driven assortment tailored to affluent women. That was a profitable business…which tapped out at about 800k-1mm customers. Then it went to men, then kids, then Europe…all of which have been margin-dilutive. The company should have stopped once it fully penetrated its core customer and churned out cash flow and bought back stock. But it didn’t. It’s new Freestyle program sidesteps the core competency of curating product for customers, and allows people to pick their own threads. To be clear, that’s what Nordstrom and Macy’s do. SFIX is becoming an online version of a department store. There are clear negative implications there for sales predictability, gross margins, inventory turns and capital intensity. We don't think management is planning for having to compete like we think it will be forced to. This company was something special in its early pre-IPO days. Now it’s become just what the tech investors don’t want to admit – a retailer. Retailers trade on earnings and cash flow. A $40 stock definitely doesn’t respect that reality. Best Idea Short