“The tighter you squeeze, the less you have.”

-Thomas Merton

Thomas Merton was a Trappist monk who wrote “The Seven Storey Mountain”, one of National Review’s 100 best non-fiction books of the last century. After seeing most of my short positions get Tightly Squeezed last week, I figured I’d spend part of my weekend studying my personal performance purgatory.

Rather than opine on what is and what is not an unrealized gain or loss, long time readers of this strategy note know that the score doesn’t lie – people in this business do. Here’s my entire book of positions (with cost basis and performance) in the Hedgeye Virtual Portfolio as of Friday’s close:

Now the point here isn’t that this portfolio doesn’t look as bad as it will if this market keeps going higher. There are no rules against buying or covering anything at any given time. The point is that it’s possible to express a very bearish point of view without getting smoked. But you need to get the timing right.

On the way down, perma-bulls can get crushed. Since its October 2007 high, the SP500 is down -22%. On the way up, perma-bears can get squeezed. Since its March 2009 low, the SP500 is up +81%. My role as a Risk Manager isn’t to be perma-anything.

My role is to attempt to be duration-agnostic and manage the multi-factor and interconnected risk that I see across global markets and time horizons. If I miss being long the top or short the bottom, sometimes that’s just the way it goes. Both tops and bottoms are processes, not points.

Here’s a brief rundown of the Hedgeye Portfolio’s current SHORT positions (in order of actions taken):

- Capital One (COF) – I shorted it again on Friday as Josh Steiner’s research continues to lead us to believe that putback liabilities aren’t priced in.

- Bank of America (BAC ) – I shorted it again on Friday after Josh Steiner highlighted some admissions in BAC’s 10Q that putback liabilities are real.

- Russell 2000 (IWM) – I shorted it on Thursday with the Russell +17.5% YTD and immediate term overbought in order to short small cap beta.

- The Euro (FXE) – I shorted it on Wednesday in conjunction with covering the short position I’d held in the US Dollar since June 7th.

- SP500 (SPY) – I shorted it again on Thursday as I continue to believe that Quantitative Guessing (QG) = JOBLESSS STAGFLATION.

- Italy (EWI) – I shorted it again on Thursday as Berlusconi’s leadership issues persist as do Italy’s sovereign debt problems heading into 2011.

- US Homebuilders (XHB) – I shorted it again on Thursday ahead of Friday’s pending home sales number (which was bad) and 30-year rates going up.

- Hudson City (HCBK) – I re-shorted this Josh Steiner idea (tri-state residential mortgage exposure) after covering it well, lower.

- Chipotle (CMG) – I shorted it again on Wednesday as Howard Penney’s research continues to indicate that the topping process is underway.

- Zimmer (ZMH) – I re-shorted this Tom Tobin idea (peak margins and pricing pressure) after covering it well, lower.

- Emerging Markets (FFD) – I shorted it again last Monday as global macro risks of mean reversion to the downside continue to mount.

- American Express (AXP) – I shorted it on 10/28 as Steiner thinks an imminent growth slowdown at Amex will lead to further multiple contraction.

- Illumina (ILMN) – I shorted it on 10/27 as Tom Tobin things growth expectations and multiple expansion are peaking ahead of a 2011 slowdown.

- Japanese Yen (FXY) – I shorted it on 10/8 as “Japan’s Jugular” remains one of our 3 core Hedgeye Macro Themes for Q410.

- Short Term Treasuries (SHY) – I shorted it on 6/23 with the expectation that at some point in my life, the yield on my savings account won’t be zero.

So, what does this tell you? Well, what it tells me is that what I’ve learned shorting stocks for the last decade continues to hold true. Unless you get the timing right, short-and-hold is not an effective risk management strategy.

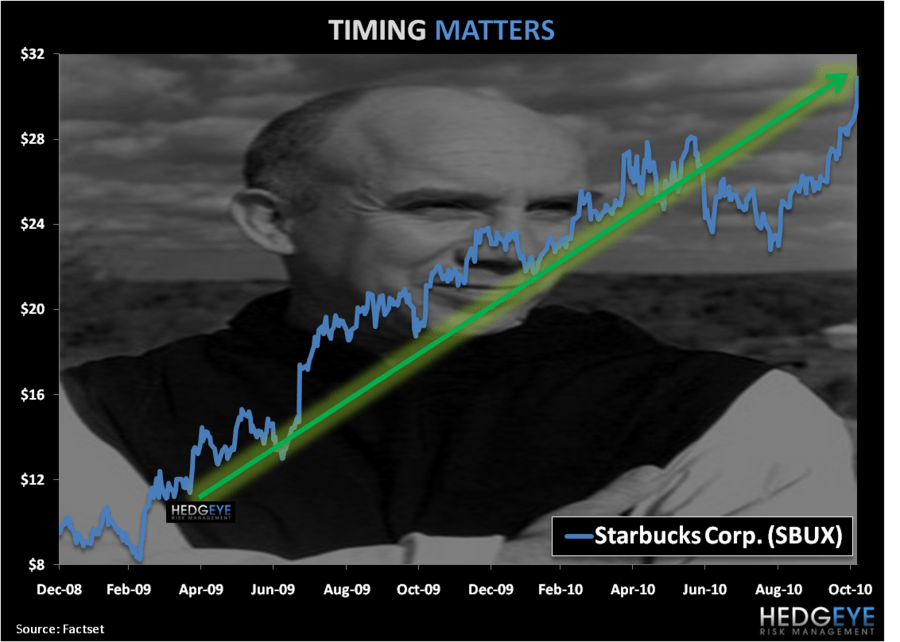

Neither is buy-and-hope. Unless, of course, you get the timing right. While it was nice to see Howard Penney’s long Starbucks (SBUX) position continue higher out of Thursday’s earnings report, the only reason why we have a +168% long term gain here is that we had it in us to buy it when consensus didn’t want to buy anything Consumer Discretionary in early 2009.

When I look back on November 8th 2010, after being Tightly Squeezed for the entire week prior, will I have had it in me to hold the line on these short positions? I’m human, so I doubt it – but that’s probably the best reason why I should.

My immediate term support and resistance levels in the SP500 are now 1195 and 1227, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer