This guest commentary was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst. This piece does not necessarily reflect the opinion of Hedgeye.

Our earlier comment in The Institutional Risk Analyst about the Federal Reserve Board’s interest rate “tweak” and rescue for money market funds (“Fed Hikes Rates, Rescues Money Market Funds”) generated quite a few comments.

The consensus seems to be that the US is caught in a liquidity trap caused by near-zero interest rates, trillions in unnecessary fiscal stimulus and an aging population that is disinclined to spend much less borrow.

In classical terms, we are taught that spending must match taxation or the system is choked by hoarded cash. But what happens when the spending is pointless, asset prices are soaring and we are loitering at the zero bound of interest rates?

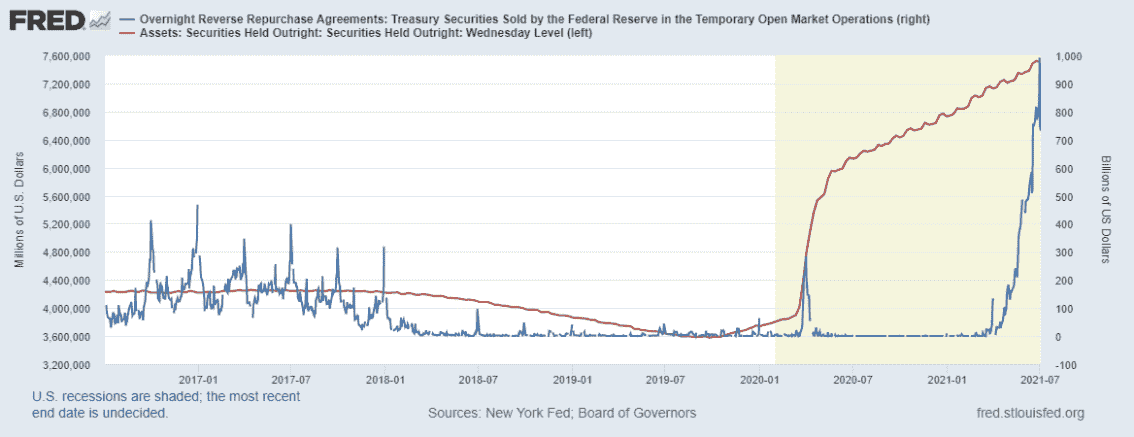

That’s why the fact that the Fed feels the need to again employ reverse repurchase agreements (RRPs) on a massive scale is notable.

Our profiles of Upstart Holdings (UPST) and Blend Labs generated a fair amount of reader mail and scores of subscriptions to our Premium Service by anxious investment bankers and public relations professionals.

We can only be flattered. For the record, we are interested in talking to any financial institution that has good things to say on-the-record about either UPST or Blend.

To us, the emergence of numerous examples of fintech “skin jobs” in the world of public finance is merely a symptom of the disease known as Quantitative Easing or QE. When you shift the risk curve and give crap issuers access to funds on investment grade terms, money moves -- quickly. A skin job, for those not paying attention, is a derisive term for a replicant in the 1982 Ridley Scott film “Blade Runner.”

Relatively substantial fintech firms such as Square (SQ) represented a software and business process “skin” applied to the world of legacy banking and consumer finance. These firms are disruptors in a sense that they force the legacy monopolies to adjust and improve.

The important point, of course, is that the dinosaurios do change and they will incorporate the features of upstarts into legacy offerings. And all this is made possible thanks to QE.

The once disruptor SQ, of course, eventually had to become a commercial bank in order to compete with the larger banks. Only insured depository institutions can have a master account at a Federal Reserve Bank and only banks have federal deposit insurance.

If you as a “disruptor” don’t have a master account or FDIC-subsidized funding, then you are the customer of a bank. Get used to it. And naturally enough, MMFs are customers of commercial banks.

The high tide of zero-cost investment capital that has floated literally dozens of IPOs and special purpose acquisition corps or “SPACs” has also tended to lower the quality of the offerings.

As the cost of capital declines, it seems, the real value of the opportunities available also decays. But when early-stage companies can raise equity capital from the likes of Softbank or dozens of other private equity firms, there is little or no credit discipline involved. Equity finance is about the future.

In a world of low or zero interest rates, expected returns are entirely based upon capital appreciation from a future sale. Duration and potential volatility are infinite. The return of and on capital depends fundamentally on a greater fool arriving to buy thy precious asset.

The issuer has no cash flow obligations in the form of dividends or interest payments. In the era of Meme Investing, profitability is discouraged. All focus and attention by investors depend upon the expectation of a future sale at a higher price point.

A century ago, Bernard Baruch would bristle at being called a “speculator,” a contemptuous term focused on financiers of a certain ethnic background. Baruch noted that “a speculator is a man who observes the future, and acts before it occurs.”

But in today’s markets, speculation is more a matter of faith than empirical observation, giving investors and economists a common point of departure. We have no visibility on markets or credit thanks to QE.

Watch members of the dismal science struggling to understand the interplay between fiscal spending and the open market sales of securities by the Federal Reserve Board via RRPs.

The idea that the Fed must insert a hard floor underneath interest rates comes as a surprise to many, but since the central bank has largely nationalized the heretofore private market for federal funds, it does not really matter.

Fed funds is a purely government market controlled by economists. Notice that the yield on T-bills is now tracking the rate on RRPs, the new de facto lower limit for US interest rates.

Paul in Paris notes that the Fed’s reverse repurchase agreements have matched almost precisely the flow of funds out of the Treasury General Account (TGA) and into US banks. Bingo.

The fellow wearing the lion costume working the buttons and leavers behind the big curtain is not Bert Lahr, but Fed Chairman Jay Powell. He is trying to fine tune global dollar liquidity.

Some observers see RRPs as a means of preventing rates from rising, but we disagree. The increase in interest paid on bank reserves (IOR) and the RRPs are about defending the lower bound and, indirectly, protect banks and MMFs from the disaster of negative interest rates.

Yes, the Federal Reserve Board did direct an increase in rates several weeks ago, but only as an expedient to prevent rates trading further into negative territory.

Back in June, when there was talk of the reflation trade ending, our friend Ralph Delguidice reminded us that there was indeed basis expansion. This was only a short-lived promise, however, just a teaser really.

The Treasury and agency market promptly tightened in the past several weeks along with secondary market spreads for agency securities. But please don’t confuse that movement with the continued downward pressure on short-term interest rates.

“Mr. Pozsar thinks the Fed's monetary easing has skewed investors' incentives,” reports Julia-Ambra Verlaine of Dow Jones. “Ultralow rates and central bank bond buying have kept the yield on the 10-year Treasury note, a key reference rate for borrowing costs throughout the economy, hovering around 1.5%, below the rate of inflation. The three-month Treasury pays less than the reverse repo facility.”

"If a money dealer could borrow at zero and do something with the money, he or she would do it," said Mr. Pozsar. "The opportunity set is so poor."

We demur to that last point. Of note, US banks have a cost of funds around 15bp, yet lending is flat to down.

We wonder if Pozsar’s observation about skewed investor incentives is not the key observation for both lenders and well as managers to consider. Meanwhile, with well over $1 trillion in funds parked in RRPs at the FRBNY, we need to ponder the shift in reserve balances from banks to MMFs.

The deposits being gathered by the FRBNY via RRPs, as noted earlier, are essentially an offset for the cash being spent by the US Treasury via outlays from the TGA.

Poszar and others note correctly that this vast recycling of liquidity is “sterilized” in monetary terms, but that does not mean that the operations have no significance to banks or markets.

Specifically, we anticipate a shift in deposits out of banks and into the Fed that could further complicate liquidity in Q3 2021. Again Poszar: “We’re looking at $1.3 trillion of flows from bills into RRPs by the end of August!”

Although banks will certainly be selling securities to the FRBNY as part of QE and will thereby will create new short-term deposits, the vast scale of RRPs dwarfs the monthly levels of new QE purchases and thereby implies a shift of hundreds of billions in liquidity out of banks and into the sterile sanctum of the central bank. In essence, the Fed's operations to remove cash from the system via RRPs is an offset to the fiscal operations by the Treasury.

MMFs, don’t forget, keep their cash in a large commercial bank. But when Vanguard does a RRP with the FRBNY, the MMF gets a risk-free asset and the cash leaves the markets entirely.

Managing this liquidity juggling act is the next challenge facing Jay Powell and his colleagues on the Federal Reserve Board. As former Chairman Ben Bernanke told his colleagues years earlier, once you start QE you cannot stop.

As in December 2018, September 2019 and April 2020, the Federal Reserve Board is playing the Wizard of Oz, trying to navigate the ebb and flow of dollar market liquidity as Congress spends trillions more that we don’t raise via taxes.

The likelihood that the Fed gets it wrong and plunges the markets into another liquidity crisis a la December 2018 is fair to middling. Buckle your shoulder harness and have a great week.

ABOUT CHRISTOPHER WHALEN

Christopher Whalen is the author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington. Currently, he serves as the editor of The Institutional Risk Analyst.

This piece does not necessarily reflect the opinion of Hedgeye.