This note was originally published at 8am this morning, October 28, 2010. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“However many people you may consult, you are the one who has to make the hard decisions. And at such moments, all you really have is yourself.”

-William Deresiewicz

Those were the closing sentences of a lecture that William Deresiewicz gave to the plebe class at the US Military Academy at West Point in October of 2009. The lecture was titled “Solitude and Leadership.” It was posted in The American Scholar on March 1, 2010.

The timing of this lecture was critical. It was given by an ex-Yale professor at a time in American history when leadership was failing us. Deresiewicz is a literary critic who has no qualms calling today’s Yalies “professional hoop jumpers.” He taught Yale kids for 10 years; his opinion isn’t irrelevant. Whether we like reading it this way or not, the rest of the world thinks we’re still failing. Americans need to stop making excuses for losers. America needs winners.

Winning starts by having conviction in what you do, taking a stand, and beating someone. Whether on the field or in your portfolio, you can see the score during each second of the game. Don’t blame “depressions.” Embrace adversity. Confront your opponent. You have to play this game with passion.

Winning continues by staying true to what got you to start winning in the first place. Grit, guts, and determination works for some. Patience, poise, and flexibility works for others. You, at the end of the day, have to focus on being you.

Winning becomes your culture when you inspire your teammates to walk through walls with you. You cannot do this alone. American Solitude is having as much conviction in yourself as you have in your teammates. You have to trust them if you want them to trust you.

I’m giving you my 3 cents on this today because I’ve been travelling the American roads less travelled for the better part of the last 2 weeks. I’ve been in 8 different states (Connecticut, New York, New Jersey, New Hampshire, Massachusetts, Maine, Florida and Missouri). I’ve met with a lot of different people. I’ve also spent a lot of time on my own.

American Solitude is taking the time to think. As Deresiewicz said, “solitude can mean introspection, it can mean the concentration of focused work, and it can mean sustained reading.” Solitude can also mean friendship. “Long, uninterrupted talk with another person. Not Skyping with 3 people and texting with 2 others at the same time… talking to one other person you can trust.”

Whether your solitude is an hour long conversation at an airport bar in Kansas City, Missouri with Howard Penney or speaking with someone you never have enough time to listen to, we need to make time for conversation. Attempting to observe this interconnected world from behind your trading or manic media desk is a very dangerous place.

When I get back from the road, the first thing that people tend to ask me is “what are people saying?” or “what’s sentiment out there?” As if the cosmos lined up in a way where my perfectly qualitative sample survey can be disguised as quantifiable edge. Whether it’s right or wrong, that’s Wall Street.

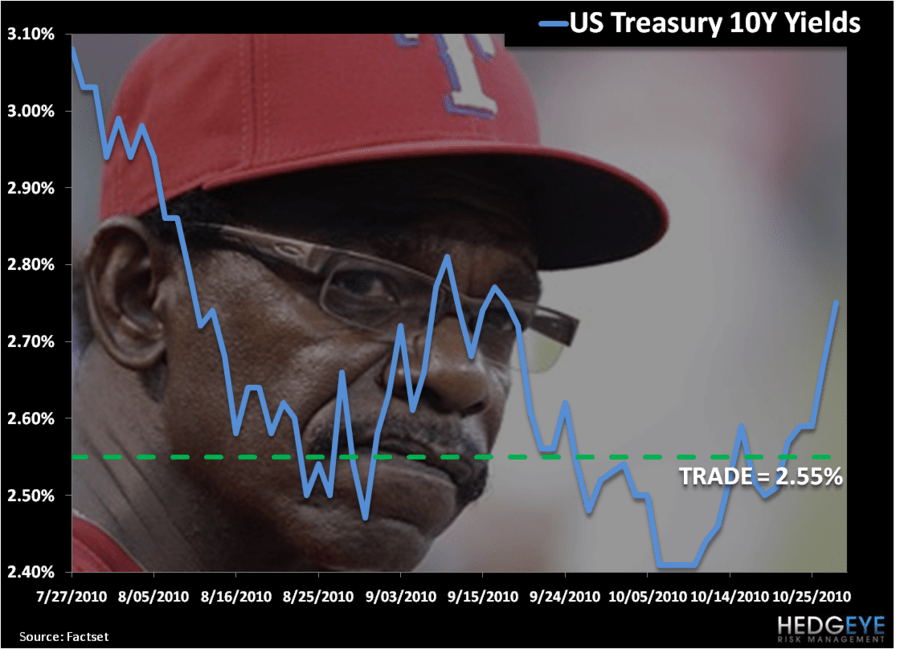

The #1 headline on Bloomberg this morning is “FED ASKS DEALERS TO ESTIMATE SIZE, IMPACT OF DEBT PURCHASES.” So, after creating massive disconnects in global expectations and seeing both inflation and interest rates rise this week, look at what the New York Federal Reserve is doing this morning – giving conflicted and compromised bankers a “survey” on the size and impact of Quantitative Guessing. This isn’t leadership – this is a joke.

Can you imagine if another Washington (Ron Washington, the Manager of the Texas Rangers) took a stinking survey days before game-time? What in God’s good name would his players think? Ben Bernanke has stated this plainly, so take his word for it – he has no idea what QE’s impact will be.

A better question to ask yourself is what aren’t people talking about? What’s the risk that the current market debate is about the bark on a QE tree as opposed to the burning forest of credibility in the US economic system? What if the Chinese or Japanese sell Treasuries and rates rip higher?

What people aren’t talking about on Wall Street is the crisis of leadership in this country. We’re hyper focused on what group-thinkers at the Fed will do next. At the same time, the politicized members of this conflicted institution are being held hostage to where the political wind blows. We’ve stopped thinking about re-thinking US monetary policy altogether.

I often get asked for my advice – what would I do? First, I say stop. That’s it. Just stop what these people are doing to your hard earned savings. Put that in your survey Bill Dudley. Stop. Then start to un-learn bad policy and re-learn the lessons of the US Military’s 2009 plebe class:

“We have a crisis of leadership in America because our overwhelming power and wealth earned under earlier generations of leaders, made us complacent, and for too long we have been training leaders who only know how to keep the routine going. Who can answer questions, but don’t know how to ask them. Who can fulfill goals, but don’t know how to set them. Who think about how to get things done, but not whether they’re worth doing…”

Yesterday was a win for my team. We sold volatility (VXX) on strength and we covered some shorts (XLY and HCBK) on weakness. We bought oil (USO) and we bought casino operator Pinnacle Entertainment (PNK). If the government is going to sponsor shortened economic cycles and amplified volatility, I’ll just as soon assume the position of American Solitude and trade this market proactively. Every man for himself.

My immediate term support and resistance lines for the SP500 are now 1168 and 1192, respectively. In the Hedgeye Asset Allocation Model, I now have a 61% position in Cash, 24% in Bonds, 12% in International Currency, 3% in Commodities, and 0% in both US and International Equities. In the Hedgeye Portfolio, I remain short both the US Dollar (UUP) and US Equities (SPY).

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer