Airport traffic was down 2% which should contribute to a lousy September on the Strip. Shrewd timing by MGM and its equity deal.

August was a blockbuster month on the Las Vegas Strip and MGM took advantage by pricing its equity deal the week after the numbers were released. Nice timing. At least they released their full quarter numbers so we could back into the September performance. It didn’t look good then, at least in the Baccarat segment, (“STRIP BACCARAT TOOK A BIG BREATHER IN SEPTEMBER, 10/13/10) and it doesn’t look good now. With airport traffic down 2% and facing difficult hold comparisons, the other gaming segments will likely come in disappointing as well, particularly slot win.

When MGM pre-released earnings, our conclusion then was “a 50% move in the stock for this?” Indeed, the stock is down 19% in an up market and up sector since the day before they announced the equity deal. In addition to the dilution, the anticipation of a September slowdown probably contributed to the stock pressure so the actual revenue release may not be a huge surprise. However, it is clear that Las Vegas is not making the V-shaped recovery implied by the August numbers. One month does not make a trend.

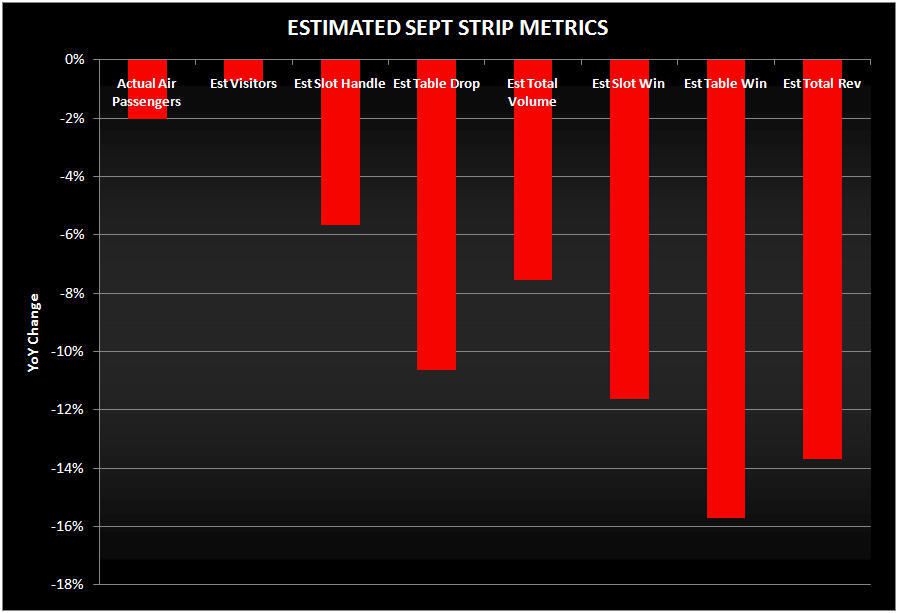

Here are our projections for September and the McCarran numbers: