1. Pet Care Black Book | CHWY, WOOF, STIC/BARK, NEBC/Rover On Wednesday, April 21st at 10am we are hosting a black book to review the state of the Pet Care industry and provide our latest view on the relevant stocks. Tickers to include CHWY, WOOF, STIC/BARK, and NEBC/Rover.

The Pet Industry is one that has seen strong tailwinds since the pandemic with rising pet ownership and spending per pet continuing to rise. Several companies have come public (or are expected to via spac) in recent months including WOOF, Barkbox, and Rover. CHWY meanwhile, which has been a Best Idea Long for us since May 2020, went up nearly 3x, but has since come in some. We remain net bullish on the pet category with CHWY still a Best Idea Long and WOOF making its way up our long bias list. We recently removed STIC from our short bias list around $10.50 after adding it at over $14 in Jan as we get closer to a closing of the Barkbox acquisition. The concern now is around comping the comp, though we think pet care and services is still poised for outsized growth and share of wallet gains.

2. Huge CTRN 1Q guide up. $2.75 to $2.90 vs street at $0.91. A 3x guide up, for a single quarter, where expectations had already moved up. The earnings ramp for the company has been massive. When we went long this we said $3-$4 in EPS for 2021, recently we’ve been thinking the higher end of that range. With this 1Q result without changing the rest of the year the model goes to over $5 in EPS. $1.50 in 2019 to probably $5+ in 2021. The company will guide the year on its 1Q call in May. The thesis continues to play out. Business improvement under new management. Strong long term earnings growth plan/targets. Huge 2021 comps from re-opening, government support/cash injection, and ramping consumer sentiment for its core consumer. We don’t think those tailwinds are done. With a market cap just approaching a billion this is underfollowed and under owned, and could make a good acquisition target for some of the bigger players in the space. A fair multiple here is probably around 25x, with EPS revision higher, prob looking at a $125+ stock.

3. DBI Clearing Out Nike. DSW (DBI) is promoting Nike (NKE) shoes at 40% and 50% off. The promotions are clearly a violation of Nike pricing policy and DSW’s retribution for Nike choosing to no longer sell to DSW. Our sense is that DBI is looking to clear out its Nike inventory (which is about 6-8% of total inventory) as fast as possible to make room for Adidas, Vans, and the other brands that are fighting for the space inside DSW being vacated by Nike. Good bold proactive move by DSW/DBI here.

4. China Duty Free beat driven by Hainan. CDFG parent company China Tourism Group Duty Free Corp reported preliminary Q1 results this morning with revenue of RMB18.1bn ($2.8bn) vs estimates of RMB17.9bn ($2.7bn) with the beat driven by sales on Hainan Island. The revenue corresponds to 127.5% yy growth due to COVID effects from last year, and up 3.7% quarter over quarter from Q42020. China Duty Free had ~RMB12.8bn ($1.96bn) in revenue specifically from Hainan Island in Q1, a yy increase of 329% and a quarter over quarter increase of 12% from Q42020. Yes, you read that right, 70% of China Duty Free’s revenue came exclusively from Hainan Island this quarter. China Duty Free still currently holds roughly 90% of the market share on Hainan Island, but as noted in our Best Idea Long Dufry’s black book we see that number moving toward 70% in the future as Dufry and other travel retailers expand and optimize operations on the Island. Additionally, this week LVMH called out that its duty free arm, DFS Group, is encouraged by the results it is seeing on Hainan Island. This market remains a gold mine for international travel retailers, and today’s results confirm our thoughts on the market size. Now we wait for the other players to capitalize.

5. Dufry Refi. Dufry announced this morning that it plans to issue €850mm in principal senior notes. These notes will come in two tranches, a Swiss Franc tranche maturing in 2026, and a Euro tranche maturing in 2028. Proceeds from the offering will be used for refinancing existing bank debt and general corporate purposes. Dufry expects that both tranches will be admitted to the Official List of The International Stock Exchange. The notes are only available for non-U.S. persons outside the US and exact terms and conditions will be finalized in the coming days. We’ll see where pricing comes back, but we suspect the company is looking to reduce interest expense with this refi.

6a. GME Developments. Multiple news items on GME this week driving some volatility. First there was an old wall downgrade to sell from neutral, with a price target change from $12 to $10. Somehow that incremental $2 downside makes it a sell with the stock at $160. Then later that day it was reported by Reuters that GME is in search of a new CEO to replace George Sherman. This could be read several ways, as the company has retained an outside agency to aid in the search. It could mean Ryan Cohen doesn’t want the job, and would rather supervise from the chairman seat. Or it could simply be that the company(board) is doing its due diligence vetting Cohen among other potential qualified candidates for the CEO job. If the job was just handed to Cohen and something went wrong, there could be a governance case against the board. Perhaps makes sense to get a third party thumbs up. The company also announced its retiring some debt which likely removes some covenant restrictions and frees up the ability to do strategic M&A when it would like to which is at least part of the new strategic plan.

6b. Replay | GME | Fireside Chat With Rod Alzmann Here is the replay of our call on GME with Rod Alzmann to review the past, present and future of GME and the story and the stock from here. Rod is one of the original retail investors that was very bullish on GME. He is cofounder of gmedd.com which shares research, news, and insights on GameStop. We discuss the evolution of the bull and bear debate, the current standing of the GME thesis, and where the company might be going under Ryan Cohen's new leadership. Replay Link: CLICK HERE

7. The KSS activists have settled with the company. 2 board seats and increased buyback authorization. KSS is also adding Christine Day (former LULU CEO) to the board. Our take is this is net bearish for the stock. We said the activist campaign wouldn’t go very far, the group has now conceded twice (first time reducing target seat count) and settled. A continued campaign and potential total management changeover would likely keep investors more bullish on the optionality. The settlement means we can focus on fundamentals again. This is a board upgrade, so perhaps we see some better execution, but we have serious doubts the KSS earnings headwinds and structural positioning can be fixed. The buyback authorization doesn’t mean much to the bull case, as the company will have to invest in Sephora buildouts and ecommerce growth, while the BS is leveraged, so cash generation is more relevant to share repo than the authorization itself. Given the reopening trade and incredibly strong near-term sales trends across retail, we’re not pounding the table on this name yet. Longer term we think risk/reward makes sense on this name short side.

8. Wayfair announced Way Day is returning to April. In 2020 it was moved to late September due to the pandemic. Much like Amazon Prime Day way day keeps getting longer, what was once a day, then 36 hours, is now 2 days. The company will need this type of event to moderate the coming slowdown in revenue as much as possible as it laps significant growth that came in 2Q 2020 from the combination of increased home furnishings demand with consumers locked at home, increased online purchasing demand with stores closed, and ceded share from the likes of Walmart, Amazon, and Target that were heavily focused on consumables and essentials. Though, Wayfair has been enjoying stronger than normal gross margins, which could be pressured by a promotional sales event. Perhaps the bigger issues on the Way Day change is how will the company comp the comp in September and 3Q given it won’t have Way Day to tap into at that time of the year. We’re short Wayfair.

9. SFIX Founder and CEO Katrina Lake stepping into an Exec Chair role -- out as CEO. Rarely does a CEO 'transition out' from a position of strength. Things can't be going well at SFIX right now. We're short the name since 2/20 at ~$76. I still think this name ultimately revisits its IPO price – though my gut tells me that it should have a sequential improvement in 2H as more dressy apparel (wear to work) sees a resurgence. The point is that if you missed the short so far you might have another shot at a higher price.

10. DLTR Advertising. DLTR announced Chesapeake Media Group which looks to be a new advertising platform to monetize real time direct marketing to DLTR customers, particularly customers at the Family Dollar banner where brands are more plentiful. It’s an interesting idea for DLTR to set up a marketing platform as it does have a large store and customer base. Family Dollar states it has 14mm users of its smart coupons program. It’s hard to say today what this means in terms of incremental earnings opportunity, but certainly seems like an positive development. We expect management will discuss it’s rationale and the potential earnings impact more on upcoming 1Q earnings call.

11. GPS is switching its credit partner. It was previously signaled by the company that they would consider other offers at the end of the SYF contract. The portfolio, reported to be $3.8bn as of March 31st, is being transferred to Barclays. We estimated the revenue share for GPS to be about $420mm (at 100% gross margin rate) in 2019. It makes sense for GPS to shop around the portfolio for the best terms. Another ‘right move’ by management to get the company in a more profitable position. GPS has been falling on our short list this year as we think the rate of change on re-opening and earnings revisions could take this higher. Is a real recovery EPS priced in here? Potentially, but the catalyst calendar does not favor a conviction short at the moment.

12. BBBY Losing Share In a Hot Category. BBBY traded down post earnings – it’s no stranger to big moves on earnings day. While the company beat, putting up $0.40 vs the Street at $0.31, the problem yet again was the topline. This is an environment where we’re seeing everything home-related put up mind-numbing sales results, and BBBY missed by a percent. Yes, one paltry percent. I know I’m nit picking. But the upside in this model has entirely been on the cost side, and there’s only so much people will pay for cost cuts. We need real revenue growth. In fact, the company guided 1Q revenue growth of ‘over 40%’, which falls short of the Street at 46% -- and is very unimpressive given that it’s going against a -49% top line in 1Q of last year. Tough to pay up a high-teens multiple for such muted top line trends when the sector it’s in is so hot.

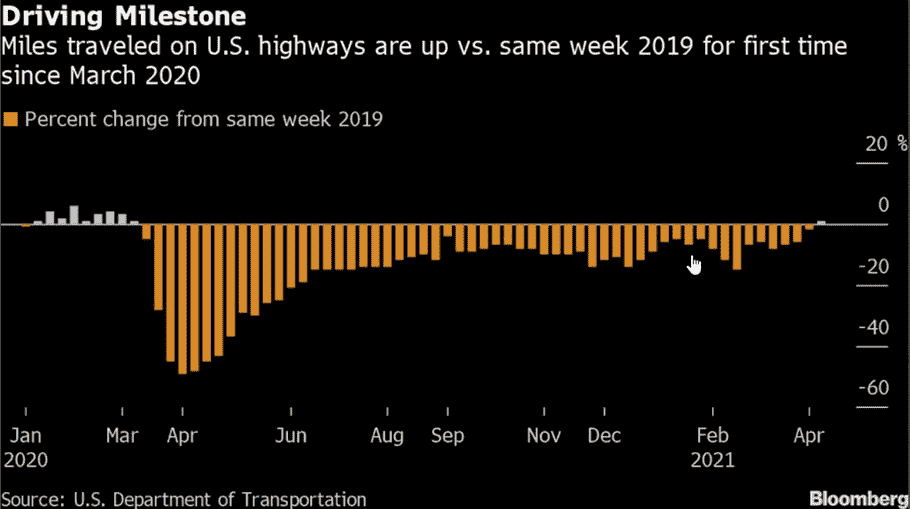

13. Miles Driven Inflect. AAP-ORLY-AZO-MNRO-VVV Bullish. For the first time in over a year, Miles Driven vs 2019 turned positive – bullish datapoint for the Auto Parts retailers…AAP is our horse in that space, and we’d expect a positive preannouncement from the company in the coming days ahead of its 4/20 analyst meeting – where we expect the company to outline the bridge to finally narrow the margin gap between competitors, with a very specific and quantifyable plan as to how to get it done.

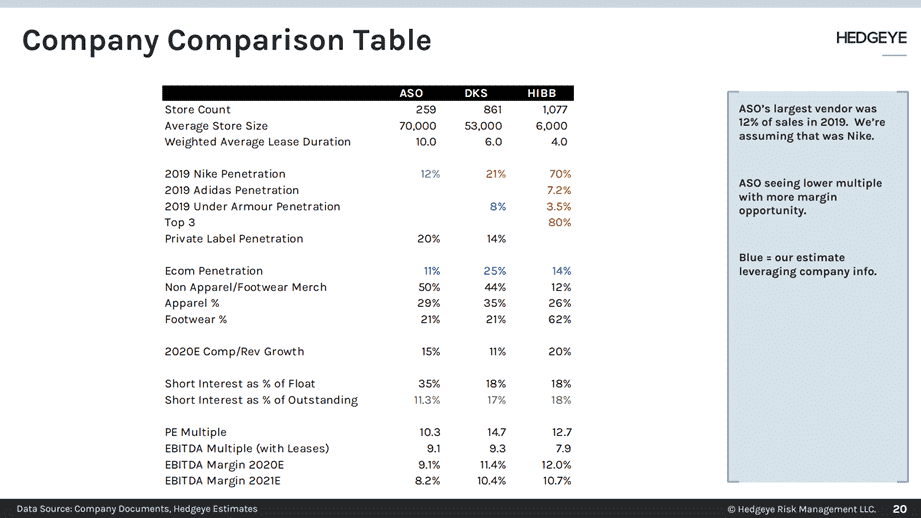

14. ASO buys Redfield. Academy Sports purchased the Redfield Brand from Leopold. Redfield carries various sport/hunting optics like binoculars, scopes, and sights. Leopold has been looking to concentrate on its core brand so ASO likely got a good price here. The brand should be a nice private label complement for ASO which has a strong hunting/shooting customer following. We highlighted the margin opportunity in our presentation on Sporting Goods in February. ASO has the highest private label penetration, yet margins are well below competitors. It suggests the opportunity for continued merch/gross margin improvement which is what the management team has been working to execute under Ken Hicks. This deal should be another opportunity to drive higher profits on ASO’s sales. For our sporting goods Black Book Replay and Slide Deck Link: CLICK HERE

(numbers as of our Feb black book)

15. LVMH Beat. LVMH fired on all cylinders in Q1 reporting overall sales of €13.96bn vs. estimates of €12.76bn. Sales and organic growth in all segments of the business beat consensus estimates with Fashion & Leather Goods leading both categories posting revenue of €6.74bn with 52% organic growth vs. estimates of €5.97bn and 33% organic growth. Asia was the largest market for LVMH in Q1 representing 41% of revenue, followed by the U.S. at 23%, Europe at 18% and ROW at 11%. In the U.S. LVMH noted that it is beginning its Sephora partnership with Kohl’s this year and expects to be in 850 stores by 2023. LVMH also deliberately mentioned its duty-free business on the call stating that while international travel is still low the DFS team is focused on “reducing selling expenses and cost structure” while also searching for growth investments such as their store in Hainan. The fact that LVMH specifically called out Hainan is a bullish circumstantial data point for our Best Idea Long Dufry, who we believe poised to capture most of the Hainan sales outside of China Duty Free Group. Overall a strong start to the year for LVMH.

16. WMT swapping employees to full time. Walmart expects that 2/3 of its U.S. hourly workforce will transition into full-time roles with the same week-to-week schedules by Jan 31, 2022. Walmart currently has 1.2mm hourly workers in the U.S. so roughly 740,000 of them will become full-time employees. The company is following the full-time labor strategy that has been successful in its distribution and fulfillment centers where over 80% of the employees are full-time. With an already robust and growing pickup and delivery business, more full-time roles allows Walmart to increase these operations while keeping them running efficiently. Beyond the expected efficiency, perhaps there is a regulatory consideration here, as full time workers can create the value needed for higher hourly pay, that would push WMT’s average wage up much higher and reduce the risk of the potential for an escalating federal minimum.

17. Massive March Retail Sales. It was a strong headline MoM beat with 9.8% vs 5.5% expected for total retail and food. Total retail was up 28% YY. Retail excluding food, Gas, and auto was up 36%, that’s on top of down 6% yy. Some of the sub stores categories growth numbers are massive. For example sporting goods, toy, hobby stores were up 74% on top of down 16%. Big numbers, we’re starting to get some very positive preannouncements and we expect more. Obviously stimulus is helping, but April compares get way easier, May is easier than march for most. We’ll likely have a lot of earnings announcements that are well above consensus through 1Q earnings season coming over the next 8 weeks or so.