overview

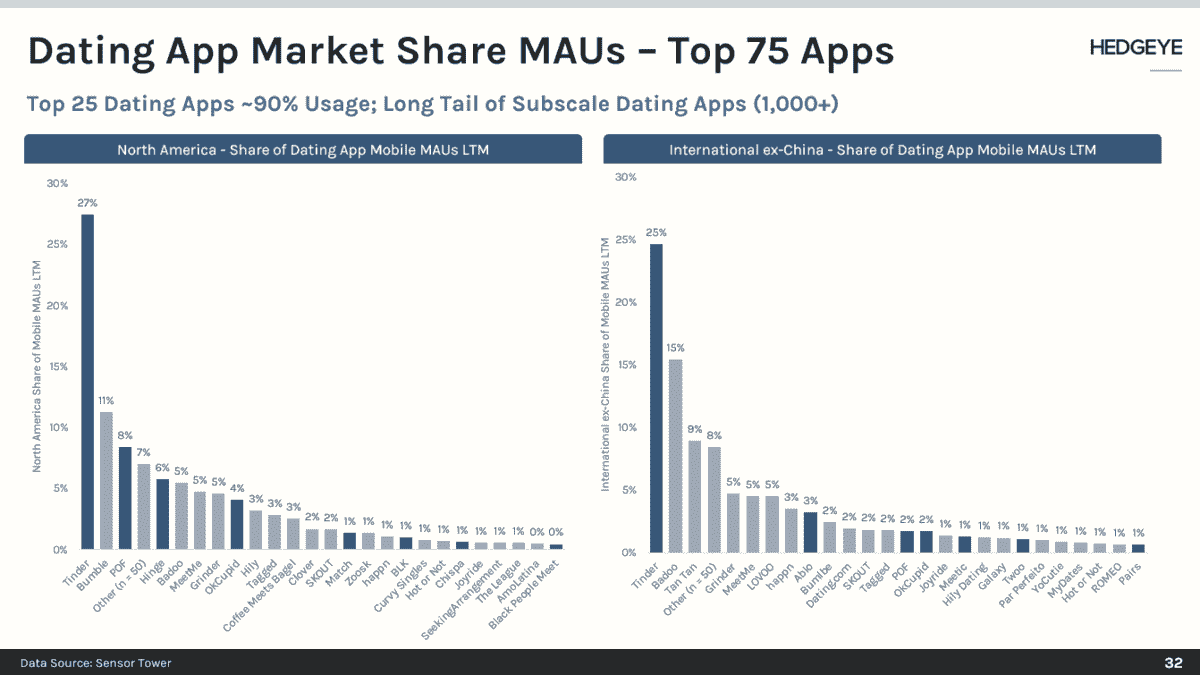

We are adding Bumble (BMBL) to the short bench in the Hedgeye Communications Position Monitor. Our short bias on BMBL was born out of the work we did on Match Group (MTCH) in September 2020. Bumble owns the second most popular mobile dating apps in North America (Bumble) and International ex-China (Badoo) after Tinder. Bumble's success in North America results from its mission-based branding and differentiated use-case where "women make the first move." Since its founding in 2014, the Bumble app has served as an off-ramp for Tinder users seeking a different experience - not surprising that MTCH reportedly tried to buy Bumble in 2017 for $450M. However, we believe that off-ramp is increasingly shifting in the direction of Hinge (acquired by MTCH in 2019) and will erode Bumble's incremental growth and profitability over time. Meanwhile, we view Badoo as a mature brand that will be costly to revitalize and scale outside their existing markets.

We have been waiting for the IPO to add BMBL to the list. The company held its public debut last week, with 50M shares pricing at $43 (vs. $37-$39 range) and the stock settling at $75/share with an enterprise value of approximately $14B. At this valuation, BMBL is trading at an estimated ~15x '22 EV/Sales - a premium to MTCH's ~13x. While Bumble is growing faster than MTCH ('20 Sales ~19% YoY vs. MTCH ~17%), its adjusted EBITDA margins are 12pts lower ('20 26% vs. MTCH 38%). We don't believe a premium valuation is justified as MTCH offers similar growth potential with w/higher margins and better diversification.

We will move BMBL to an active short based on price and proximity to catalysts, including lock-up expiration and more difficult growth comparisons in the 2H21. Be on the lookout for a research roundup for pro subs early next week.

Please call or e-mail with any questions.

Andrew Freedman, CFA

Managing Director

@HedgeyeComm

203-562-6500