NewsWire 3/23/21

- According to the latest CBO budget outlook, the federal debt will nearly double to 202% of GDP by 2051. That's not all: Outlays will endlessly outpace revenue, every major trust trust will go broke by 2035, and net interest spending will be 2X the size of defense spending by the 2040s. (Committee for the Responsible Federal Budget)

- NH: Yesterday, I wrote about the economic scenario spelled out in CBO's latest long-term forecast (2021 to 2051). Today, we're going to look at CBO's fiscal forecast.

- I'll start off with some highlights of exactly what's in the report. These aren't pretty. But then I'll go on to lay out three basic reasons why I think the report actually underestimates the true magnitude of the challenges we face. How America confronts these challenges--in terms of politics and policy--is beyond the scope of my note. But forewarned is forearmed: Over the next five or ten years, big and unwelcome fiscal changes are on the way.

- OK, let's now focus on the report itself. I'll first summarize the report's major findings. Then I'll follow with charts.

- After the early 2020s, once the shock of the pandemic recession is over, federal outlays will grow every year as a share of GDP--hitting 32% of GDP by 2051. That's slightly more federal spending in a normal year (CBO by default is assuming 2051 is a normal year!) than we spent during the pandemic emergency year of 2020.

- This rise in "normal" spending is driven entirely by three trends: (1) the rising share of 65+ Americans eligible for Social Security and Medicare; (2) the continuously rising real per-capita cost in public health-care benefits--mostly, Medicare and Medicaid; and (3) the growing burden of annual interest payable on the publicly held federal debt.

- Revenues, meanwhile, will rise very slowly. From 2025 to 2051, as a share of GDP, federal outlays will be growing roughly 8X faster every year than revenues.

- Large and accelerating deficits are the inevitable result. Incredibly, over the projection period, the federal deficit is expected to hit its all-time low in 2026 and 2027 of "only" -3.7% of GDP. After 2042, the deficit will be continuously in the double-digits.

- All major federal trust funds will be insolvent within the next 14 years. The Highway Trust Fund will go broke by 2022; the Medicare Hospital Insurance Trust Fund by 2026; the Social Security OASI Trust Fund by 2032, and the Social Security DI Trust Fund by 2035. (CBO assumes benefits will continue to be covered after insolvency by general revenues or borrowing.)

- While historically low real interest rates help suppress the rising cost of net interest (perhaps unrealistically--more on that below), both interest outlays and the federal debt begin to accelerate upwards by the late 2030s.

- By 2031 the publicly held debt will exceed its previous historical highpoint (106% of GDP in 1946), and by 2051 it will reach 202% of GDP. Meanwhile, in that year, federal net interest outlays will reach 8.6% of GDP, which is 2.6X what we currently spend on national defense.

- All this looks and sounds pretty dire, to be sure. But some observers, after looking carefully at the CBO projections, may notice that they seem to imply a decade of relative post-recession fiscal stability during most of the 2020s. Yes, these observers may concede, the longer-term fiscal trends are unsustainable and we do need to correct them. But they could argue that America still has plenty of time to act in the mid- or late-2020s before things get out of hand.

- But do we really? I'm inclined to believe we don't have all that much time. Much as I hate to pile on after all the bad news delivered by the CBO, I would like to offer several reasons why the CBO's outlook may be understating the magnitude of the fiscal challenges we face--that is, why the CBO's outlook may actually be overly optimistic.

- I laid out one reason in yesterday's NewsWire (see "CBO Projects an Aging and Slower-Growing Economy"), in which I argued that the CBO may be imprudently optimistic about future economic performance. CBO's fiscal projections depend critically on the future size of the economy: If real GDP grows more slowly in future years, revenues will lag even further behind outlays--and the deficit and debt numbers will start accelerating sooner.

- But in this note, let's shelve my doubts about the CBO's economic baseline. Here I want to focus specifically on the CBO's fiscal baseline and offer three major reasons why I think it is flawed. The CBO does not bear responsibility for the first two flaws. But it does for the third.

- Let's look at the first flaw that is not the CBO's fault. Congress specifically directs the CBO to project future outlays, revenues, and debt according to current law. And Congress means that quite literally. So, for example, when this report came out, the American Rescue Plan stimulus package had not yet been signed. That means an extra hit of $1.9 trillion that was not counted. Nor of course was the infrastructure package now being discussed ($3.5 trillion over ten years), which probably won't be fully funded by new revenue.

- A realistic assessment of our fiscal future would recognize what is very likely to happen. But the CBO cannot recognize any of that, which means we are looking at trillions in near-term deficit spending that is left uncounted.

- Even worse, "current law" is riddled with benefit hikes and (especially) major tax cuts that are due to expire over the next ten years but that Congress and the American public fully expect to be permanent.

- These mirage-like sunset provisions exist because, according to BCA rules, major reconciliation bills (in which most of these goodies are legislated) require a budget balance beyond 10 years. So they are all due to expire at the 10-year mark--at which point Congress typically enacts them again. But of course the CBO does not expect them to be enacted again. In other words, the official CBO projection already benefits from an implied program of future fiscal austerity worth trillions which would shock most Americans if they knew anything about it.

- To appreciate this sunset effect, consider that CBO's total baseline revenue in 2027 is 1.7% of GDP higher than it was in 2019 (17.9% versus 16.2%). Whence all this new revenue? Mostly from the sunsetting of various tax cuts. Put another way: If Biden rescinds important parts of Trump's 2017 tax cut, he won't be adding new revenue; he'll just be speeding up the receipt of revenue that the CBO is already counting on.

- OK, now let me move on to my second problem with the CBO's fiscal outlook. It is increasingly dominated by autopilot spending and, over time, leaves ever-diminishing room for spending to prepare for future problems or to respond to new emergencies. Again, this is not the CBO's fault. The CBO's mission is simply to project the fiscal consequences of current law as spelled out by Congress. But that doesn't mean that current law gives us a realistic perspective on our fiscal future.

- To see what I'm talking about, let's divvy all federal outlays into two streams. One is "discretionary," meaning that it is appropriated each year and can be reallocated by Congress according to changing needs. The other is "mandated," meaning that the payments are legally required (e.g., to creditors) or are fulfillments of hallowed promises (e.g., Social Security and Medicare).

- Back in 1962, 68% of total federal spending was discretionary. Much of that went to national defense but also to a variety of ambitious public works projects, such as putting a man on the moon. By the late 1970s, the discretionary share dropped under 50%, thanks to a massive expansion in senior benefit programs. By the 1990s, after downsizing national defense, we were closing in on 40%. In 2019, we were at 30%, just over half of that for defense. The remaining 14% pays for everything else, from the interstates, national parks, and the border patrol to weather services, the NIH, and the entire federal workforce (including even the SSA bureaucracy that calculates and mails our benefit checks).

- So here's the problem. By 2051, the CBO assumes that the discretionary share will shrink to just 17% of all spending. If we keep defense spending fixed at its 2017 level as a share of GDP (3.1%, the lowest share since before Pearl Harbor), we still have only 7% of all outlays left over for everything else.

- To find an earlier year in which federal discretionary spending was so small relative to the size of our economy, you'd have to go back to 1929 or 1930, just before FDR's New Deal. The only difference, of course, is that back then the entire federal government was minuscule. By 2051, it will be massive. It's just that it won't be paying for anything that Americans have control over.

- As I've argued many time over the years, this is a fundamentally unserious perspective on America's fiscal future. There is no longer any leeway to shift budgetary resources to meet new needs, such as a national security crisis (involving threats abroad) or a domestic crisis (such as another pandemic). And as for public investments in anticipation of future threats, well, such dollars must inevitably be borrowed--if indeed a polarized Congress can ever be persuaded to appropriate such funds.

- OK Boomers, Millennials get it. Their parents came of age in an era in which Congress spent generously on America's future. But Millennials are coming of age in an era in which any new dollar spent on the future threatens to break the bank. So in response to each shock, we don't prepare for the next shock. We "save money" by stripping from our budget any room to prepare for the next shock.

- It's a bit like a floundering company getting acquired through successive LBOs, where each new buyer cannibalizes everything not needed to keep the lights on this month. While the books may show (bare) solvency, the numbers don't come close to reflecting the true cost of doing business going forward.

- I understand the CBO is just following Congress's orders here. But by following orders, the CBO does not produce a realistic or sustainable understanding of our fiscal future.

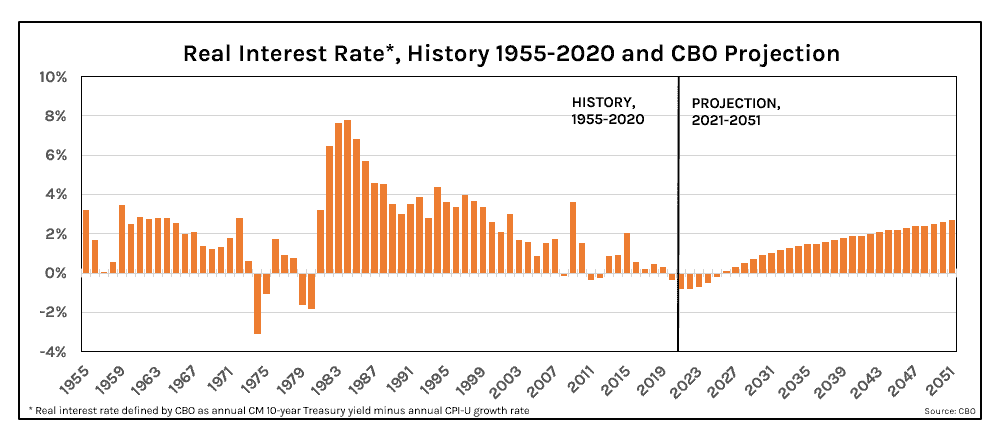

- Now let me turn to my third problem with the CBO's fiscal outlook. I want to focus on a critical assumption that the CBO really can do something about: the real interest rate. The CBO defines the real interest rate as the annual constant-maturity 10Y Treasury rate minus the annual CPI-U change. No, it's not an ex ante market measure of the real rate like the 10-year breakeven. But as a convenient way to gauge the "real" impact of net interest outlays, it works well enough.

- Currently, the CBO estimates that this real rate will average +1.2% over the entire projection period. In particular, per the CBO, the real rate will remain very low for many years to come. It will stay negative through 2025 and won't rise above +1.6% until 2038.

- Why does +1.6% in 2038 matter? Because this is the first year in which the real interest rate is expected to creep slightly above the real GDP growth rate, anemic as that growth rate may be. Until 2038, therefore, the national debt--even after compounding at its long-term carrying cost--actually shrinks a bit every year as a percent of GDP. For the next 17 years, in other words, America gets to take a wonderful holiday from meaningful fiscal trade-offs.

- When you look at it this way, the wonder is not that the CBO's debt projection by 2051 is so large. The wonder is that it is not massively larger. It would be if the projected real interest rate were higher.

- So let's examine the CBO's real interest rate projection--which averages -0.2% in the 2020s, +1.4% in the 2030s, and +2.2% in the 2040s. What's most striking about it? Again, it's the fact that it's so low in the early years. If you compare these rates with what the CBO assumed back in 2019, you find that they are lower during the 2020s by -0.5%, higher in the 2030s by +0.2%, and higher in the 2040s by +0.3%.

- That lower real interest rate during the first decade generates huge compounded savings on debt. Due to the pandemic, federal deficits added 16 percentage points of GDP to deficit spending in 2020 and 2021 relative to what CBO was projecting beforehand. But thanks to a lower real interest rate, CBO's 2021 projection of the debt in 2030 is only 7 percentage points larger than in CBO's earlier projection.

- Now let's ask a more important question: Are these real interest rates plausible?

- I don't think so. The US historical record is certainly not encouraging. Over the 140 years from 1881 to 2020, the annual real interest rate (calculated the way the CBO does it) has averaged +2.5%. In only 24 of those years (17% of all years) was it negative. And in only 30 years (21% of all years) was it under +0.5%.

- To be sure, America has experienced a couple of brief but brutal episodes of super-negative real interest rates. The two biggest of these were triggered by skyrocketing double-digit inflation coupled with vigorous financial repression by the Treasury and Fed during and just after World War I and World War II. So that's a possibility. But it's not a possibility envisioned in the CBO's projection. To the contrary, the CBO projects the CPI to level off at +2.2% annually and never rise above 2.5% in any year. Nor, without major legislative or regulatory changes, is financial repression likely.

- Without these two wartime episodes (lasting a total of 14 years) the average annual real interest rate since 1881 rises to +3.0%. And only 12% of all years were negative.

- A couple of other more recent episodes of negative interest rates occurred during the "stagflation" the mid-1970s and early 1980s and during the 2008 GFC and its aftermath. Yet not only does the CBO expect no exceptional inflation, it also expects something close to a full-employment economy every year after 2021. Unemployment is expected to fall steadily from 5.0% in 2022 to 3.9% in 2026 and never again rise above 4.5%. A low marginal rate of return on capital might make sense during a time of substantial underemployment. But that's not what the CBO is projecting.

- After looking at the last four years before the recent recession (2016 to 2019), the CBO may be assuming that near-zero "risk free" real rates will continue to prevail in the rest of the high-income world. If so, it may figure that this environment will act like financial repression by eliminating alternatives and keep global investors satisfied with near-zero U.S. Treasuries.

- But is it reasonable for the CBO to be resting the next 31 years on an environment that only prevailed for four years (2016 to 2019) before the recent recession? Are low global real rates a permanent crutch on which the US can reliably depend? Over the last four decades America has imported savings massively (through a negative current account) in order to take advantage of lower global rates. But how long and at what price will the rest of the world continue to be willing to export its savings?

- Under current law, over the next decade, the CBO expects the federal government to issue roughly $1 trillion in new debt every year--in addition to rolling over everything else it already owes. As the CBO itself acknowledges, the growth in publicly held federal debt will crowd out other borrowing and raise real interest rates. That's why the CBO is still pushing real rate past 2.0% after the early 2040s. Today, at 100% of GDP, federal debt already comprises over one-third of all debt securities and loans held by US domestic nonfinancial sectors. As it rises toward 200%, the federal share of the fixed-income pie will steadily expand.

- So again, back to our question: Who will keep buying it?

- Let's start with foreigners. The share of US national debt held by foreign entities has been rising over the years. It's now just over one-third (34%). Foreigners will continue to acquire some new debt for prudential and quasi-official purposes (FX reserves, bank reserves, swap lines, and so on). They will also keep buying so long as they trust the sustainability of America's economic leadership and so long as their own economies remain in low gear. But how long will these conditions prevail?

- I'm especially concerned about foreign perceptions of America's economic leadership. It is no secret that the U.S. international investment position is rapidly deteriorating. If I were an investor abroad, I might look at this trend and wonder whether to keep subsidizing America's bottomless appetite for low-interest funding.

- Let's move on to the Fed, which now holds 23% of this "publicly held" federal debt. Sure, the Fed will be happy to keep buying federal debt, but only if inflation stays quiescent. Unfortunately, that's a big "if."

- Then there's the remaining 43% of the national debt held by all the rest of us--the U.S. private sector (plus state and local governments). Even our patience may not endure year after year. We may start actively seeking portfolio alternatives if we come to believe our nation's economic policies are forcing us to risk senseless losses.

- In the near term, I foresee several scenarios that could trigger a shift toward significantly higher real interest rates. These include accelerating economic activity either at home or (especially) abroad. They also include sharply higher inflation expectations, which would widen the term premium for the rising expectation variability of both future inflation and the future real rate.

- Ironically, all these scenarios are predicated on good economic news, even while they hammer fixed-income assets, roil equities, and--after a while--cause enormous chasms to open up in our projected fiscal future. That in turn will have sobering political repercussions.

- Any of these scenarios, moreover, can unfold quite rapidly. Just look at what has happened to 10-year Treasuries over just the past three months. As of today, the CBO's "real rate" (10-year yield minus the YoY CPI-U) is slightly positive, at +0.05%. That's 85 basis points higher than the CBO's projected rate for both FY 2021 and FY 2022 (-0.80%). And this CBO projection was just published a couple of weeks ago!

- You might hope that the CBO would do a stress test to see what would happen if real rates swung rapidly against their assumptions. But it doesn't. While the CBO does include in the appendix to its 2021 report a scenario in which the real rate rises above its projection by an additional 5 basis points per year (that's an extra +1.5% after 30 years), the pace of this rise is ludicrously slow. (In case you're interested, yes, it does push up the eventual size of the net national debt by 2051--from 202% to 260% of GDP.)

- My final thoughts are these. In its long-term projection, the CBO succeeds in producing a logical and meticulously reasoned document, mostly based on sound neoclassical economic foundations.

- Where the CBO often fails, in both its economic and fiscal modeling, is in what I have called the "inertial optimism" of its assumptions. Here I'm referring to its tendency to stick with an assumption based on an older trend so long as it generates a favorable outcome (e.g., fertility rates), but to take risks with a daring new assumption (e.g., an entire decade in which the average real 10-year interest rate is sub-zero) so long as that assumption generates a favorable outcome.

- The CBO's worst failing, which shows up most prominently in its long-term fiscal outlook, is a sheer lack of political, institutional, or historical imagination. In its new report, CBO does blandly agree that "the much higher debt over time would raise the risk of a fiscal crisis in the years ahead." But it doesn't try to explain how or why.

- The CBO can't be faulted for carrying out Congress's instruction, which is to produce projections, not predictions, based on various unrealistic current-law assumptions. But it can be faulted for not providing readers a broader context for understanding these projections, including a more realistic range of alternative scenarios of how the future may play out. No command from Congress stands in its way here.

| To view and search all NewsWires, reports, videos, and podcasts, visit Demography World. For help making full use of our archives, see this short tutorial. |