Editor's note: This note was originally published July 03, 2014 at 12:33 in Macro. For more information on our market and economic research options click here.

Solid report overall as NFP goes >200K for five months in a row for 1st time since Jan 2000 (although that wasn’t a particularly positive harbinger), employment gains were broad based, the Unemployment rate flirts with a 5-handle, and the U-6 and total LT unemployed continued to decline.

On the other side, total part-time and involuntary part-time both increased significantly while the slope in private wage growth remained negative – with real earnings growth likely to be negative for a second month in June.

THE GOOD:

- NFP: Solid Report with NFP = +288, Private = +262, 2Mo Revision = +29K

- Household Survey: Net gain of +407K in June with Employment growth accelerating across all age buckets except 20-24 YOA

- Unemployment Rate: Unemployment Rate dropped to 6.1% from 6.3% prior alongside the +407K increase in total Employed and a -325K decrease in Total Unemployed

- U6/LT Unemployed: U-6 Unemployment dropped to 12.1% from 12.2% while the ranks of the long-term unemployed dropped -293K MoM on an absolute and -1.8% to 32.8% as a % of total

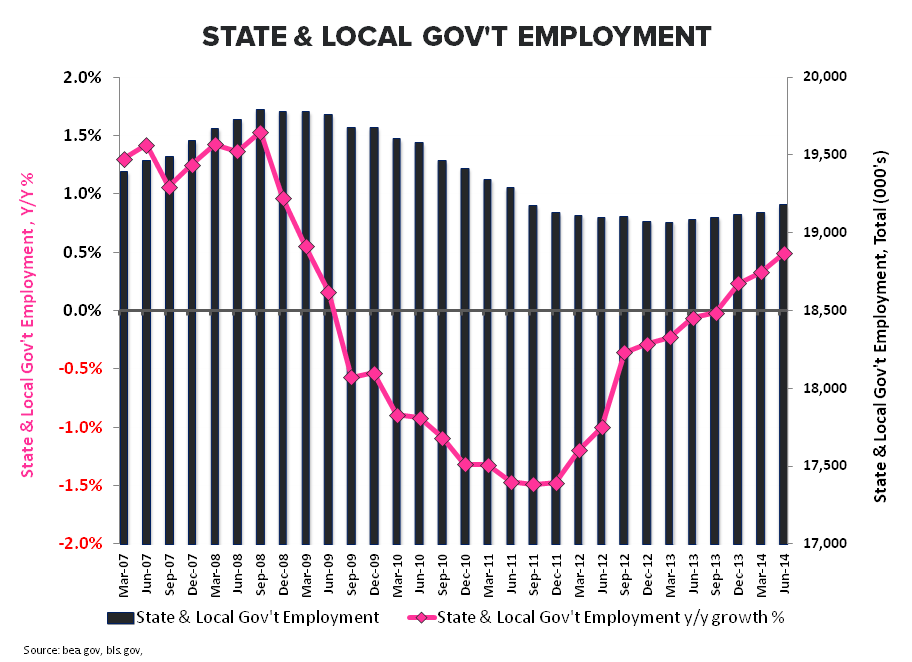

- State & Local Government Employment: increased for a 10th consecutive month in June while the rate of job loss at the Federal level improved 10bps sequentially to -2.0% YoY. Aggregate government salary and wage growth has finally begun to contribute positively to aggregate disposable income growth in recent months

- Initial Claims: The employment data has followed the steady improvement in the initial jobless claims data in recent months and this mornings update to claims was again positive with both headline rolling claims and the YoY rate of improvement in NSA claims holding near the best levels YTD.

THE MIDDLING & (STILL) MOROSE:

- Hours Worked: Ave weekly hours worked for private employees continued to track sideways at 34.5

- U-6/U-3 Spread: The spread, which sits as part of the FOMCs dashboard of “slack” indicators, ticked up sequentially with the magnitude of decline in the U-3 rate outpacing that of the U-6.

- Ticking Clock: At 61 months as of June, the current expansion continues to surpass the mean duration of expansions (59 months) over the last century. We continue to think this reality weighs into the feds policy calculus – they need to get out of QE if only to give themselves the opportunity to (credibly) get back in if need be.

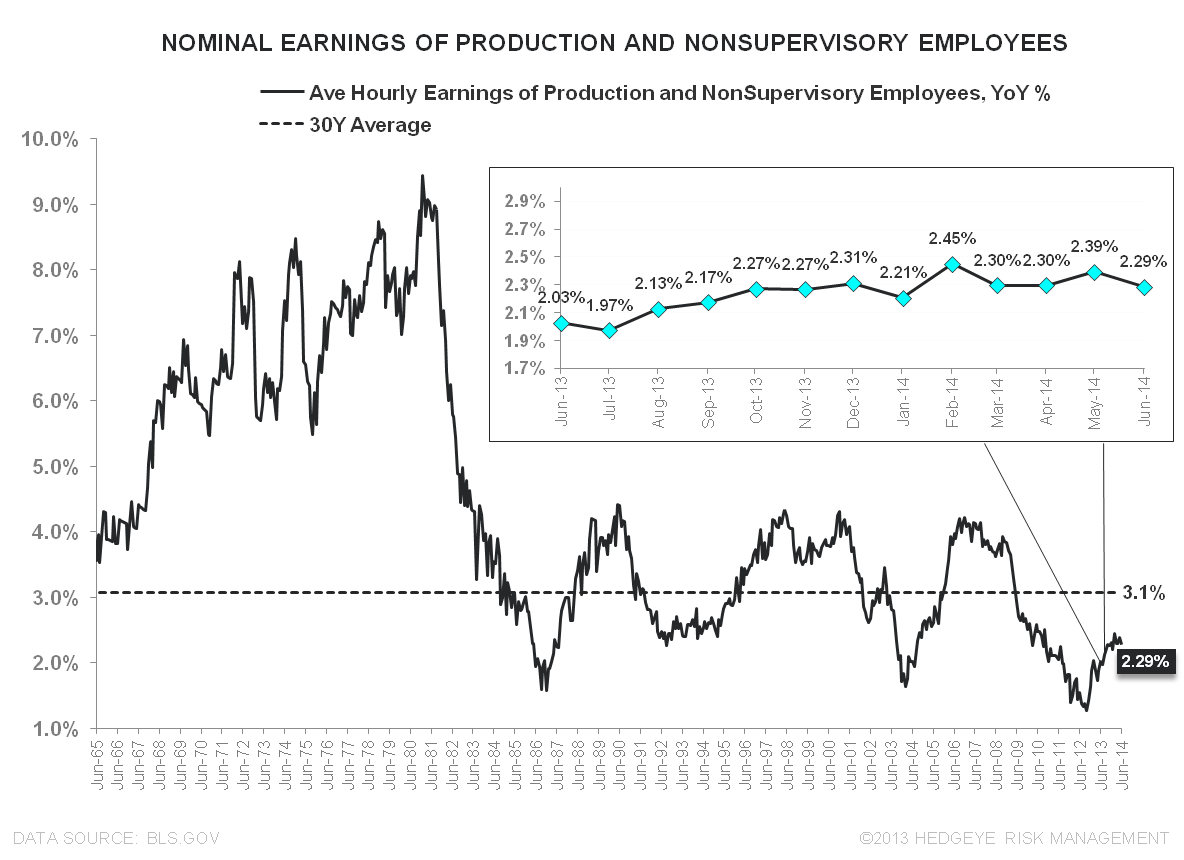

WAGE GROWTH: Average hourly earnings in the Private sector grew 2.0% YoY, down from +2.1% in May and continuing the stagnant 2.0% +/- 20bps that has prevailed over the last two years. Average hourly earnings for Production and Nonsupervisory employees also decelerated -10bps to +2.29% YoY.

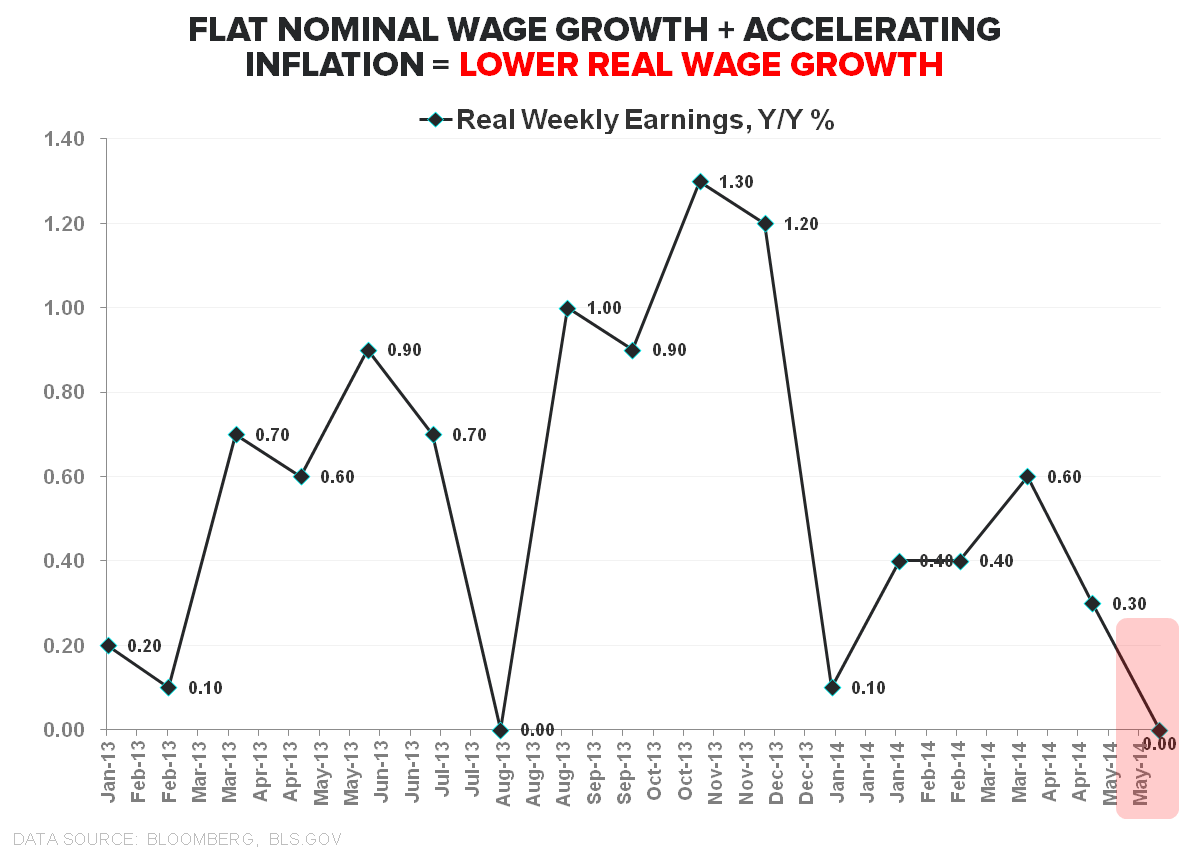

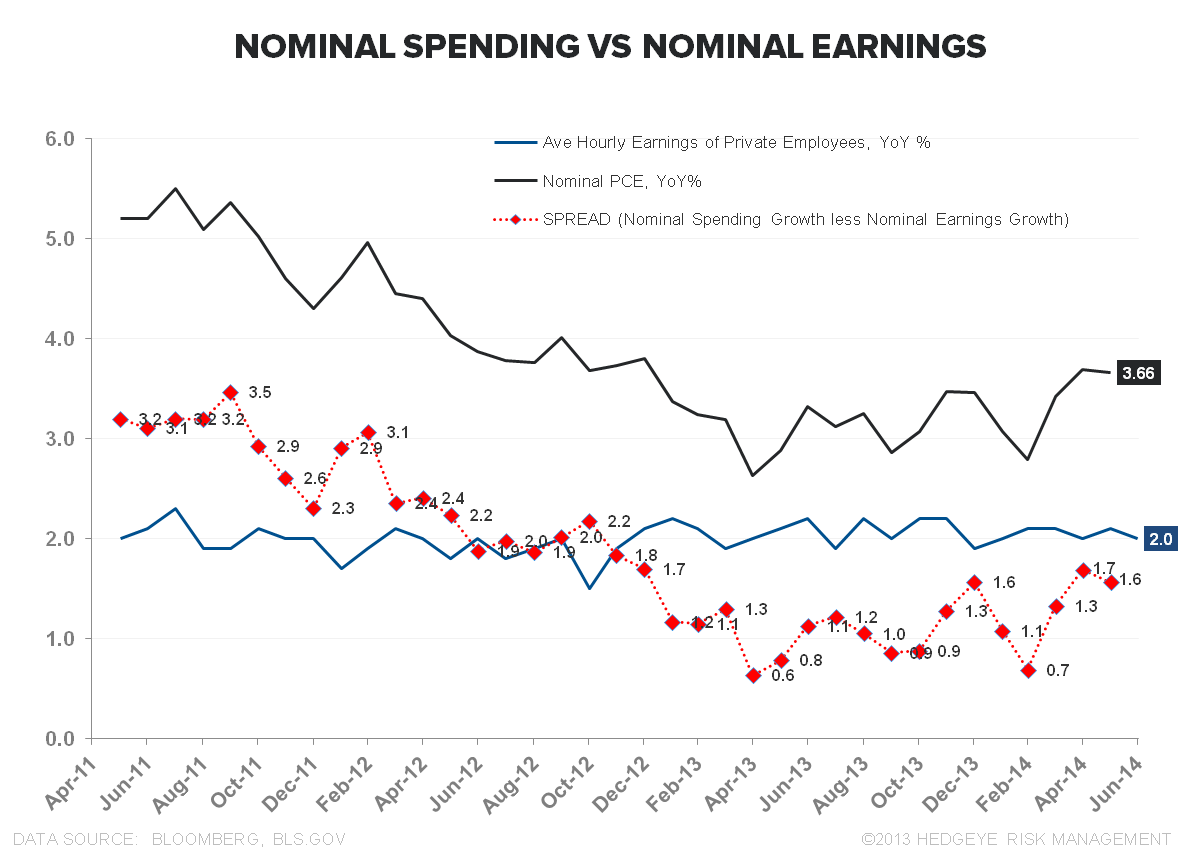

With nominal earnings growth static, real earnings growth likely to be negative for a 2nd month in June with the official release, and the spread between spending and earnings growth having re-expanded the last couple quarters, we continue to think the upside to consumption growth remains constrained in the immediate/intermediate term – particularly if inflation continues to march northward and the savings rate remains at current levels.

WAGE RAGE: Wage Growth Refuses To Accelerate, Does it Matter To The Policy Outlook?

Conventionally, wages are viewed as a lagging indicator, with wage inflationary pressure building as the labor supply declines and the economy moves towards constrained capacity. There’s a view that the FOMC won’t move to raise rates so long as real wage growth is flat or declining, which it is currently.

It’s somewhat difficult to make a particularly cogent empirical argument in either direction, however. The longest historical dataset for (real) wages is that for Production & NonSupervisory Employees which goes back to 1964 (the BLS series for total private employment reported inside the NFP release only dates back to 2006).

The problem with using this series stems from the well documented, secular plight of middle and low income earners where flat/negative real wage growth has characterized the last four decades.

In fact, the current post-recessionary trend in real wage growth compares favorably with those observed over the last half century.

We’d agree that the collective policy bias of the current FOMC body argues for dovish conservatism in the face of negative real wage growth alongside sub-target, or moderately above target, inflation levels.

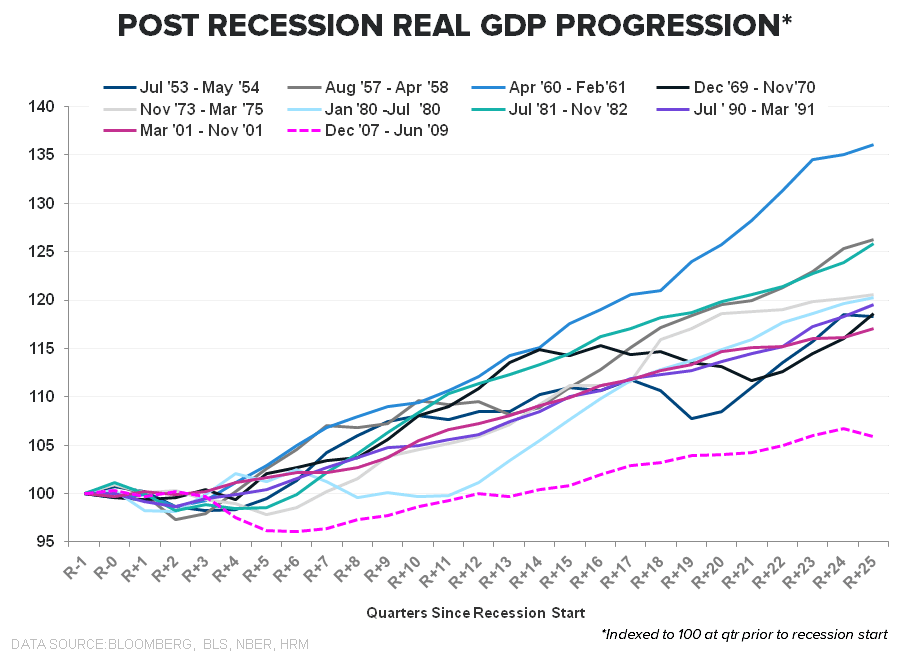

THE WORST EVER...& EVER IS STILL A PRETTY LONG TIME

The painstakingly slow progression of growth out of the Great Recession has been exhaustingly documented and the duo of negative post-recession GDP prints observed in 1Q13 and 1Q11 sit as the two worst of any post-war recession with a recovery greater than 61 months (the duration of the current expansion).

The five month run of positive labor market data has been encouraging - though not fully corroborated by broad macro strength post the immediate weather-distortion bounce.

We’d advise keeping growth optimism anchored over the intermediate as growth compares get harder and inflation comps easier in 3Q and the conflation of rising inflation, static nominal wage growth, and an ongoing deceleration in housing should drive a sequential deceleration in domestic economic growth.

The reality of the intermediate/LT is that household balance sheets remain over levered, demographics are going the wrong way, and policy driven increases in inequality will continue to feed the growing phantasm that is the U.S. middle class.

Yellen’s acute attention to the prospects for secular stagnation and hysteresis isn't misplaced.

Enjoy the Holiday Weekend,

Christian B. Drake

cdrake@hedgeye.com

@HedgeyeUSA