|

Below is a brief excerpt from a complimentary research note written by our Consumables analysts Howard Penney and Daniel Biolsi. We are pleased to announce our new Sector Pro Product Consumables Pro. Click HERE to learn more. |

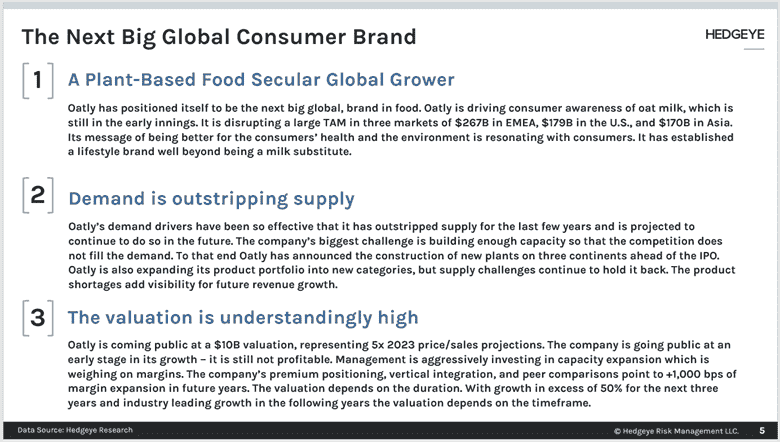

Oatly is going public this week. At the top end of the $15-17 range, the market capitalization would be close to $10B.

The valuation may seem steep, but Oatly could be the next great global consumer products company reminiscent of the greatest consumer growth stories we’ve seen IPO in recent decades (e.g. CMG, LULU, UA).

Oatly is already a proven global consumer products company as a Swedish-based brand with a significant presence in the more progressive EU/UK market as well as a market leader in the US. In addition to global growth prospects, the company is positioned to benefit from strong secular tailwinds as consumers shift to plant-based milks.

Oatly has several large growth opportunities. The company is driving consumer awareness of oat milk, which is still in the early innings of adoption.

Oatly's demand drivers have been so effective that it has outstripped supply for the last few years and is projected to continue to do so in the future.

It is growing geographically - the penetration in its home market of Sweden is much higher than the markets it has entered recently, like the U.S. It is rare for a consumer brand to be growing in two continents this early in its expansion, but Oatly has already entered its third continent.

Oatly is also growing with new products - adding yogurt, spreads, butter, cheese, etc. Only two countries even have the full product assortment.

Oatly is challenged to expand its manufacturing capacity to keep up with demand. The IPO is raising funds for future growth. The company has announced new plant construction in three continents ahead of the IPO.

In the U.S., we have documented frequent out of stocks. Perhaps the company's biggest near term challenge is to build enough supply to keep up with demand.