|

Editor's Note: Below is a flashback on our short Clover Health (CLOV) research call from our Health Policy analyst Emily Evans. Emily delivered her original hour-long short CLOV presentation on February 9, 2021, when the stock closed at $13.16. It's down roughly -40% since, hovering around $7.75 at the time this was written (on 5/12/2021). Since then, Emily's written follow-up research and discussed her thoughts with Hedgeye CEO Keith McCullough on The Call, Hedgeye's daily morning call featuring our research team's latest analysis on their best stock ideas. Emily also recently released her own research subscription, Health Policy Unplugged. Click HERE to for a 10-minute introductory video hosted by Emily to learn more about her research process and the analysis subscribers receive. |

Emily's original hour-long presentation

Updated analysis from march 11, 2021 | CLOV: More problems than carter's got pills

The very last place you want to look for disruption in health care is an insurance company.

However, the natural temptation after watching CLOV go from $17 to $8 is to wonder if at least part of the story is true.

After a review of the state filings, the 4Q earnings call and the Clover Assistant presentation last week, it seems hard to accept much of the story they tell. While one should never assign to malfeasance that which is easily explained by incompetence or indifference, it seems to us that being a public company requires at least some consistency and clarity between the official reporting and the story telling.

We have already highlighted the enrollment data that suggests a long road to profitability for a little insurance company in New Jersey. Making the path to profitability and, with it, true disruption much more difficult, if not impossible, are the ongoing underwriting losses, capital demands and the opaque approach to the Direct Contracting Program.

No nifty website is going to overcome these things, especially in the face of pent-up demand for medical care post-COVID.

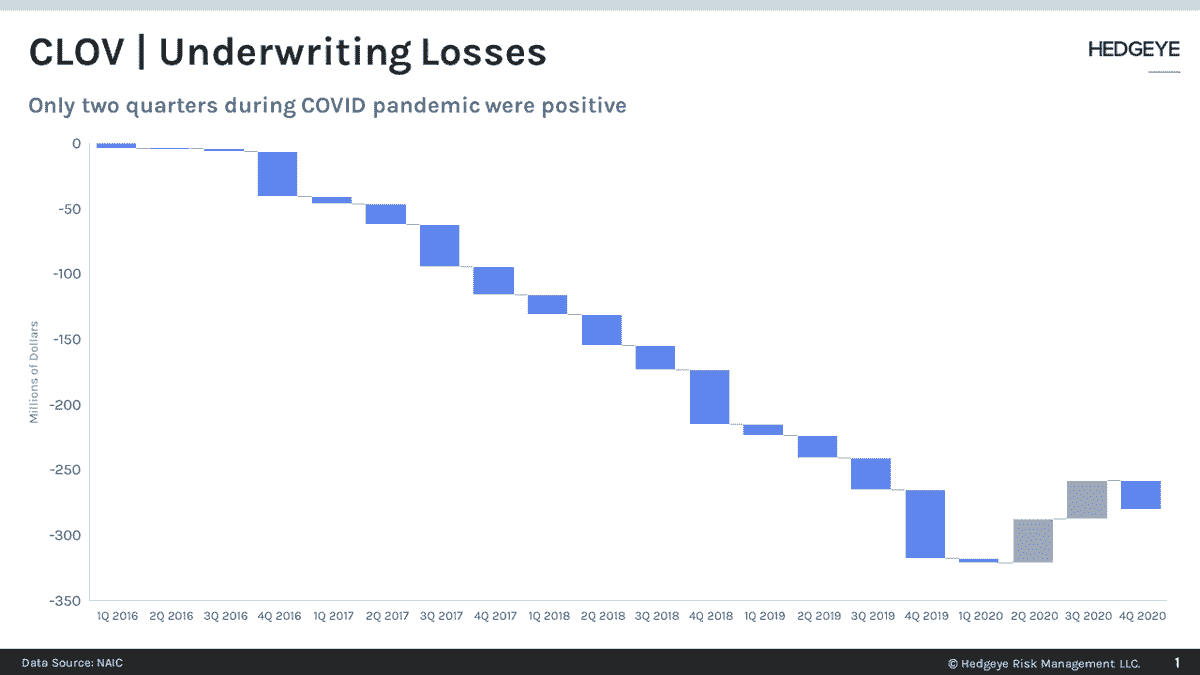

UNDERWRITING LOSSES & CAPITAL CONTRIBUTIONS

Based on disclosures made in state insurance filings, for 18 of the last 20 quarters, CLOV’s primary insurance unit, Clover Insurance Company (NJ) has experienced underwriting losses ranging from $323,000 in 2Q 2016 to $52,000,000 in 4Q 2019.

While Wall Street generally expresses ennui in the face of consistent losses while pointing to some generally unreasonable TAM, insurance regulators are not nearly as accommodating.

Underwriting losses can and do trigger state requirements for additional capital contributions. According to NAIC filings, the company accepted capital contributions totaling $235 million between ~2015 and 2020. Additionally, sometime before 1Q 2016, the insurance subsidiary received $40 million in return for a “surplus note.” These capital contributions were made by CLOV, the parent company, to the insurance subsidy.

While the original source of the funding is not disclosed, the S-4 indicates that on “December 27, 2018, CLOV entered into a Convertible Agreement with qualified institutional buyers, including entities affiliated with the Corporation for an aggregate principal amount of up to $500 million to support the Corporation’s growth in the MA market.”

Read the rest of the article, including a deep dive on $clov's DIRECT contracting practices and limited cost controls, here.

Key excerpts from the original webcast on february 9, 2021

|

What is Clover Health (CLOV)? Well, it's basically an insurance company in New Jersey. They’re in a regulated space of a heavily regulated market. Through Q1, it only had about 64,000 members. |

They have some growth in Georgia, but it’s marginal at best. They have about 2,800 members there at the moment, which is driven largely by the Walmart relationship.A lot of their members are in New Jersey, and so is the vast majority their growth. Even with 2021 data, what we have with CLOV is a local state-based insurance plan.

To great fanfare, Walmart announced they were launching Walmart Insurance Services late last year. Now based on the press releases from Clover, they say this partnership is a huge opportunity.

But really, this is a bake-off.

Walmart has engaged with a variety of health insurance companies to run plans for them, as they explore which health insurer does better than others. Humana, Anthem, Simply Health, Clover, and more, are all involved.

When it comes to enrollment growth, Clover is mostly just growing with the population – they really have no secret sauce. They’re middling along, so to speak.

|

Their market share gains are modest. The company talks about how they’re getting 50% of new eligible enrollees, and I really couldn’t find that in the data. The way they define their markets is vague; they don’t say if it’s at the county level, multiple counties, etc. So I couldn’t see where they pulled that number from. This is what you’d expect from a local insurance plan, not from a disruptor or a company “out to change the world”. And you’re not likely to change the world with an insurance company. |

The amount of money they pay out for benefits, versus the amount they take in for premiums, is at a shortfall. The parent had to inject about $20million just to meet the state commissioner’s required solvency requirements.Frankly, Clover is not very good at what they do either.

Not only is this not a profitable company, it’s not even one that can meet the solvency and capital requirements form the state it operates in.

There’s no real evidence they’re capturing a higher acuity or doses that have gone unnoticed from the annual payments via the federal government.

Their premium income is actually lower than their benefit expense… so that’s an underwriting loss. There aren’t good expense controls. Another interesting feature is their unpaid claims over 120 days, which have been increasing throughout 2020.

|

The vast majority of Medicare Advantage plans are 4-5 stars. Clover Health? 3.5 stars... for years. This isn’t a great performance, in categories the company has said they’re great at… it’s supposedly their “secret sauce”. Not to mention, their surveyed customer satisfaction is subpar as well. Humana or Anthem, well they’d probably have to fire someone, if they didn’t meet that 4-star threshold. |

Clover is pitched as a technology company. This platform is not particularly innovative. It’s pitched to doctors as a way to increase reimbursement, while it’s pitched to investors as a world-changer.Clover just cannot capture providers in their open network, meaning they cant capture clients, meaning they can’t capture government bonuses for high-star companies.

Those two aren’t the same thing.

Remember – the physician’s are paid to use the Clover system, which primarily explains why Clover is so prevalent in Fort Lee and Jersey City, where doctors are operating on very thin margins. So, I’m sure they’re happy to improve their reimbursement. That motivation will decrease.

So what is the Clover system? Who knows.

The idea that Clover Health is going to be a transformative technological answer to Medicare Advantage, let alone health insurance more broadly, is proven out to be false here.