Below we provide a number of charts we’ve been looking at recently in Europe. Taken together, we’ve been impressed with the fundamental data from Europe over recent weeks (especially compared to the US). However, we caution that:

- August Data - we expect to see a sequential slowdown (month-over-month) in the fundamental data following the exuberance of the World Cup.

- Comparisons - European markets will be pinned against significant macroeconomic headwinds in the back half of 2H10, including suppressed growth, consumer demand, and confidence as a result of government austerity measures.

- Housing - continued downward pressure on the housing market, in particular in Spain and the UK.

- Legacy - ongoing uncertainty about European bank exposure to sovereign debt, which were largely unaccounted for in the 91 bank stress test, and continued fiscal and political weakness throughout the region (more recently seen in Hungary).

On the margin, we maintain a bullish bias on German Equities (EWG) and the British Pound (FXB).

See our commentary below on the charts:

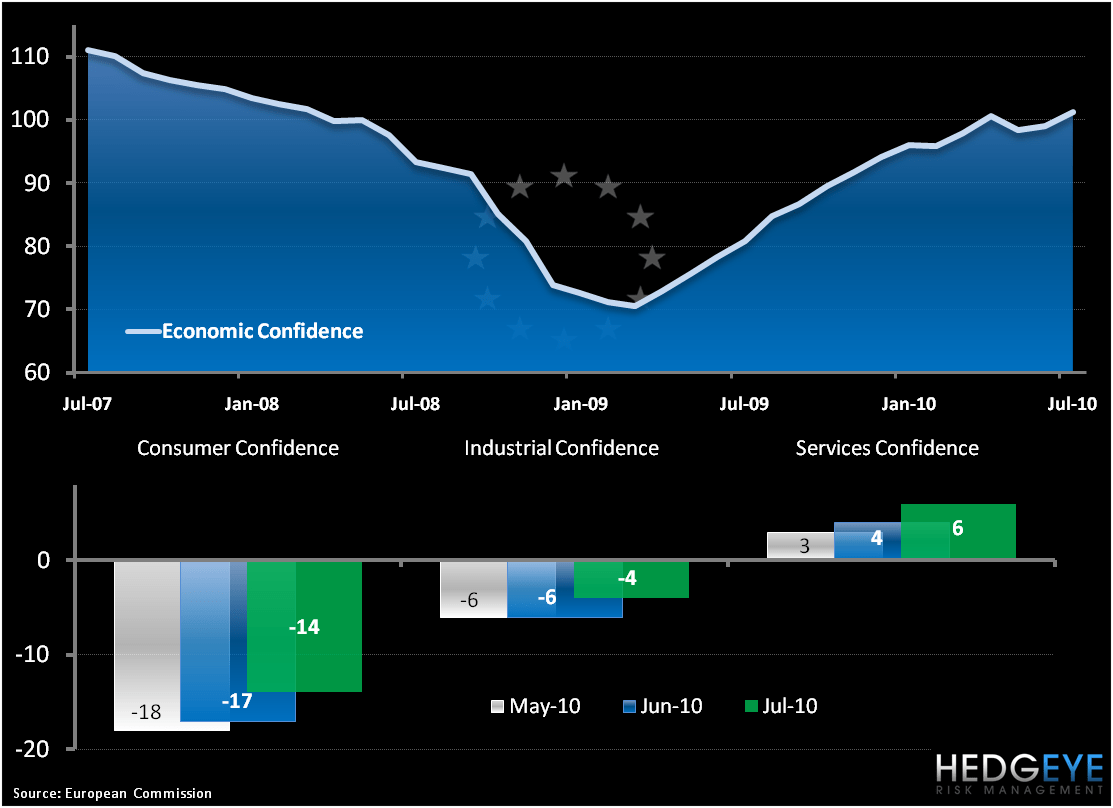

- Eurozone (16) Confidence has improved over the last three months. Can this trend be sustained, especially post the World Cup?

- The DAX and FTSE are trading above our intermediate term TREND lines, a bullish leading indicator. We’re still looking for the FTSE to confirm its move on a TRADE basis (3 weeks are less) before we act in the Hedgeye Virtual Portfolio.

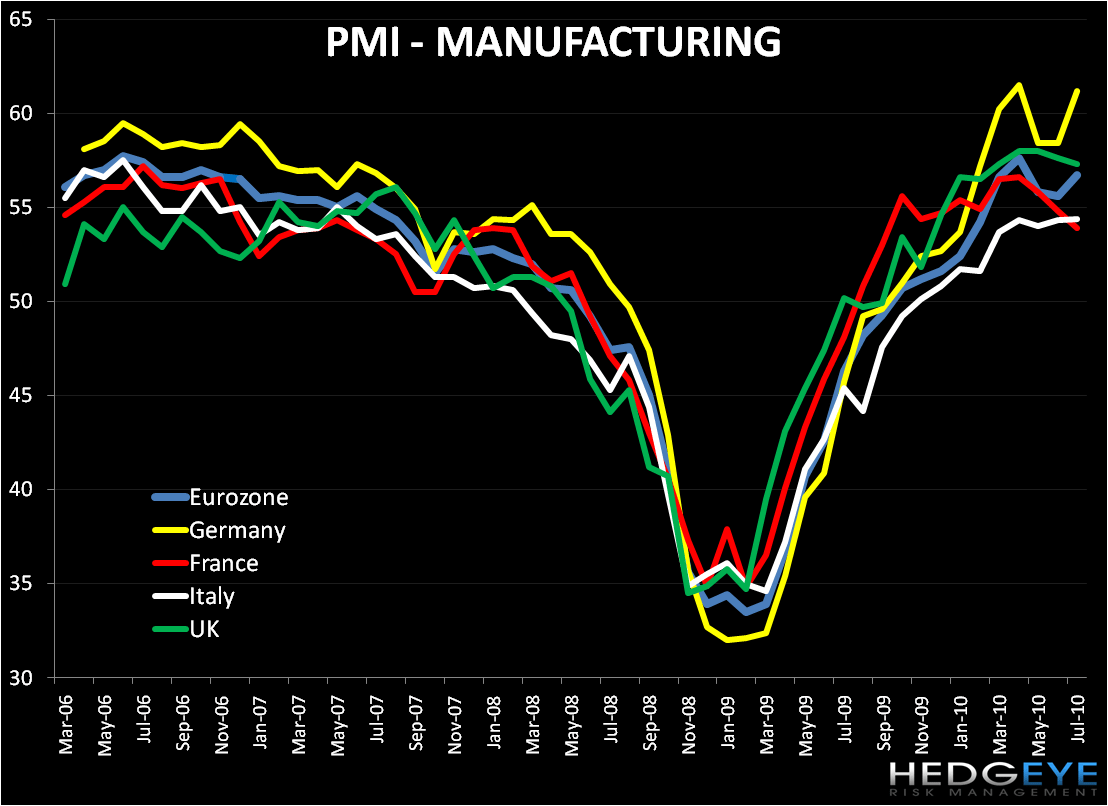

- PMI Services have largely declined for western European economies over recent months, especially in Italy and UK. Germany and France, on the other hand, have shown strength and we’ll be looking to the next two months of data to determine a trend. We continue to believe that should Western European economies slide, Eastern Europe will follow due to its trade dependence on its western neighbors.

- While the Manufacturing sector contributes a much smaller share than the Services sector across European economies, the manufacturing PMI is nevertheless an important leading indicator that we follow. Here, Germany is leading its peers. Overall, we’d expect manufacturing to slip before services in 2H10.

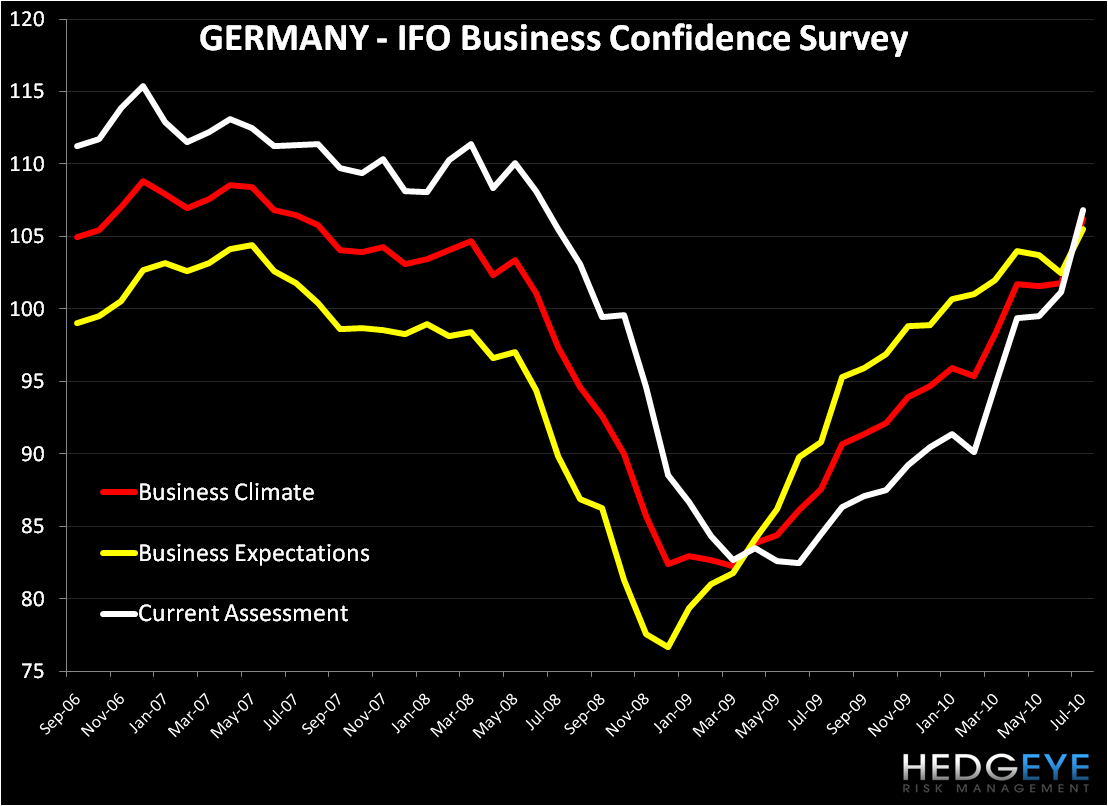

- Germany is one economy in Europe that we have a bullish bias on. For now, business confidence (below) and consumer confidence surveys have been decidedly bullish since the beginning of 2009. The recent weakness in the EUR-USD (compared to recent years) has bolstered sentiment for Germany’s export oriented economy.

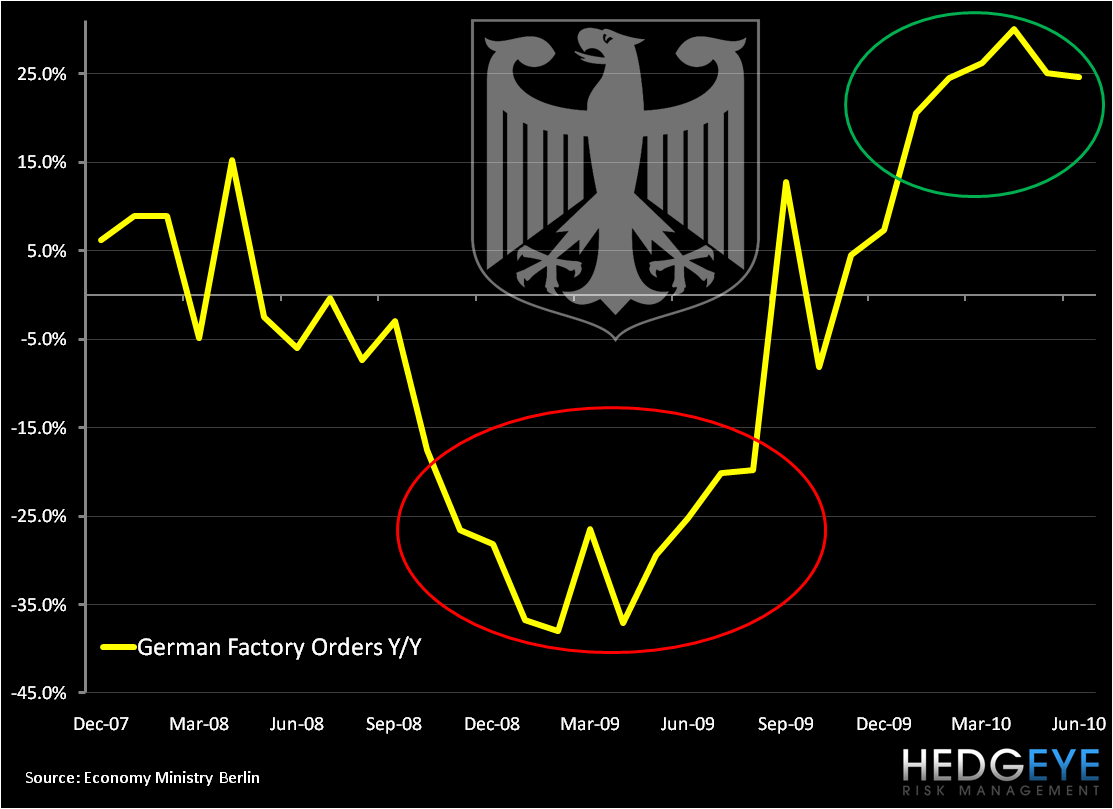

- One number we focus on is factory orders. On an annual basis we continue to caution that the recent moon shot numbers need to be considered in light of the compare—rock bottom trough levels. This “easy” compare will fade in September. However, the most recent data on a month-over-month basis saw factory orders improve 3.2% in June.

- The cash for clunkers programs issued in 2009 throughout European countries boosted sales for German automakers. Reviewing Q2 earnings calls from European automakers, sales were largely mild or flat on the continent, with sales growth particular strong from China. Due to the headwinds we’ve presented, our fundamental outlook suggests that demand from Europe and the US should stay low or erode further.

- On the TAIL (3 years or less) this chart below will continue to be an important one to return to. We expect Asia (in particular China) to increase its market share of imports from Europe as exports to the US decline.

Matthew Hedrick

Analyst