This guest commentary was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst.

At the end of last week, we featured an update from Michael Whalen about the latest developments in the world of new/old media, specifically television and streaming content. After a week of bank earnings, it seemed like a everybody might need a laugh, at least in relative terms. Like many other industries, in media fragmentation is the order of the day.

As we predicted in the Q2 2020 IRA Bank Book, loss provisions for all US banks will be higher this quarter than last. The total level of loan-loss reserves for all US banks is now just shy of $200 billion, still well-short of the peak of $250 billion in 2009-2010.

Our guess is that loan loss reserves could reach half a trillion dollars before we are close to the peak for COVID-19, but some in the banking industry are more constructive.

Source: FDIC

This week in The Institutional Risk Analyst, we are doing a little teach-in on bank loss accounting and earnings. As many of our readers know, when a bank puts aside provisions for future loss, this income is shifted to an off-balance sheet account where reserves, loan losses in the form of charge offs, and credits recognized in terms of recoveries, are reconciled.

Let’s use Goldman Sachs (GS) as an example. Loan loss reserves were $2.86 billion at the end of March, but jumped to $4.39 billion in Q2 2020, this after the addition of $1.59 billion in provisions in the second quarter.

Goldman’s loss rate was 55bp vs an average of 26bp for the 123 banks in Peer Group 1, which is all depositories above $10 billion in assets. In cash terms, GS had net charge-offs of $225 million in Q1 2020 and $260 million in Q2 2020. By comparison, GS had a $688 million accounting restatement in Q1 2020 that was disclosed to federal regulators. At GS, you see, nothing is extraordinary.

Provisions for future losses at Goldman are up sharply, but actual realized losses net of recoveries are not yet elevated. Following the industry trend and guided by internal credit metrics, GS and other banks are likely to continue to build loan loss reserves for the next several quarters, a fact that will depress earnings and also the hopes of a lot of Buy Side managers for a rebound in financials.

But it this right? Will the bank credit reserve build continue? The answer to that question will move a lot of money into or out of bank stocks in coming weeks. The calculus depends fundamentally on your view of the economy and in particular corporate credit.

In the 2009-2010 period, loan loss reserves for all US banks rose to $250 billion, but actual losses net of recoveries tracked at 20% of that then astounding number. This is why we use the early version of Basle I to measure loss given default or “LGD” for bank loan analysis. It informs your perspective of net loss rates and thus the trajectory of future provisions and thus earnings.

Source: FDIC/WGA LLC

What does all of this mean? So far, the pace of bank credit loss reserve build in 2020 is larger than in 2009, twice as big to be precise.

At the current loss rate, we expect to see the industry consume total operating earnings with credit expense in 2020 and some of 2021 as well.

We also expect to see realized losses net of recovery jump sharply higher in Q3 and several quarters thereafter. Banks such as GS, Citigroup (NYSE:C) and JPMorgan (NYSE:JPM) that managed to ride the wave of volatility in Q2 2020 are unlikely to see that extraordinary gain repeated in Q3 2020.

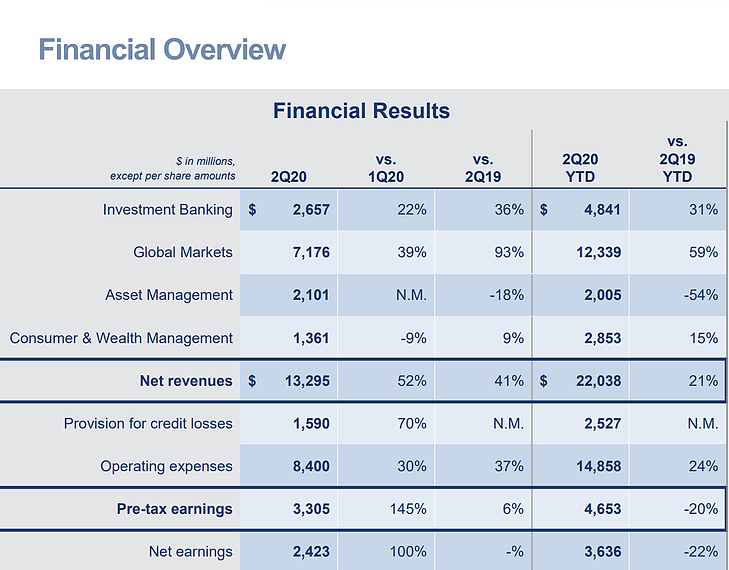

The record increase in revenue for Investment Banking and Global Markets at GS, for example, is extraordinary and again illustrates the volatility of the firm’s financial results. Also, the growth in deposits seen at GS depends greatly on whether the Federal Open Market Committee continues to monetize the national debt at the current pace. The Q2 2020 results for GS are shown below.

Source: Goldman Sachs

Estimating the actual source of the losses coming at banks is more difficult because of the breadth of the COVID-19 disruption and the efforts being used to obscure the actual credit situation facing many debtors. Many issuers, for example, are using financials adjusted for COVID19 losses on the theory that these losses are “extraordinary,” “unusual,” “infrequently occurring” or “non-recurring.” In the age of COVID19, nothing is extraordinary.

Bank do not consistently break out provisions by loan category or sector. JPM, to its credit, does provide detail on business line provisions expense. The chart below shows the provisions by business line and particularly shows the big surge in loss provisions for consumer exposures.

Source: JPMorgan

When people ask us: How bad will it be for the banks?

Our short answer is dreadful, yet the scope of the task still remains uncertain. Will loss provision builds be sufficient in Q2 2020? JPM held out the possibility that "worst case" reserve builds may have peaked in Q2 2020.

JPM's Chief Financial Officer, Jennifer Piepszak, summed it up nicely:

|

“In addition to the obvious impact on consumer, its protracted downturn is expected to have a much more broad-based impact across wholesale sectors that we’ve seen in the first quarter. Given the increased uncertainty of the macroeconomic outlook, how customer payment behavior will play out and the future of government stimulus and its ultimate effectiveness as it relates to both, consumers and wholesale clients, we've put more meaningful weight on the downside scenario this quarter. And so therefore, we're prepared and have reserved for something worse than the base case. And given CECL covers life of loan, if our assumptions are realized, we wouldn't expect meaningful additional reserve builds going forward.” |

We are heartened to hear Piepszak’s optimism about the “base case” for credit losses at JPM. JPM CEO Jamie Dimon went further and suggested that an additional $20 billion in reserve build would leave him over-reserved for the base case scenario in the Fed’s latest stress test exercise.

But the reality is that nobody in the industry yet knows what will happen with corporate exposures as the year grinds to a conclusion. We suspect strongly that provisions for commercial exposures at JPM and other major banks will be higher than reserves for consumer losses by year end.

Piepszak notes in response to a question from John McDonald at Autonomous, the most heavily impacted COVID sectors are “Consumer and retail, oil and gas, real estate, retail and lodging, and sub-sectors, as you think about real estate.” That takes in a lot of the US and global economies.

ABOUT CHRISTOPHER WHALEN

Christopher Whalen is the author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington.

This piece does not necessarily reflect the opinion of Hedgeye.