The guest commentary below was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst.

Over the past several months, news reports have suggested that the global auto industry is about to disappear.

Ford Motor (F) announced a 10 percent reduction in executive ranks earlier this year. Daimler AG (DAI) has just announced additional job cuts. Analysts blame consumer angst regarding global warming and the imminent conversion of the industry to battery-powered electric motors.

But sad to say, we think that politically motivated climate change hype inspires unwarranted pessimism about the prospects for autos, a skew in thinking which seems to color every discussion about every industry.

A better explanation of downsizing in the auto industry is the end of a massive credit expansion and the continued industry rationalization that defies efforts to reduce overcapacity. That is, the same old story.

Everybody wants to have a domestic auto industry. Many times, these industries are heavily subsidized, as in the case of electric cars in the US, Europe and China. Private producers in the US and EU are constantly forced to cut costs to keep pace. In regions like western Europe, where regulation and taxation are extreme, operating auto manufacturing operations is increasingly problematic.

But if you want a real example of global deflation, forget the autos. Instead, take a gander at the earnings prospects facing global banks and particularly banks in Europe. The good news for American investors is that US banks are still easily the leaders in terms of capital and profits, but the outlook for global financial institutions is dreadful. Read about the most recent results for the US banking sector in The IRA Bank Book Q4 2019, which is for sale now in our online store. Credit is strong, but the outlook for earnings not so much.

The bad news is that banks in Europe and Asia face a period of restructuring and consolidation unlike any time in the century since WWI. Indeed, the vast demographic and financial expansion that drove global economic growth for the past 100 years appears to be ebbing around the globe. Markets outside the US seem to be particularly at risk.

One chief risk officer tells The IRA that just about every major European and Asian bank will be forced to downsize or eliminate their capital markets arms in 2020. "Everyone has the same problem," he demurs.

EUROGROUP Consulting, for example, reports that European banks are “struggling and losing out to American banks,” which have managed to strengthen their position in Europe, notably by relying on a large domestic market and a more favorable regulatory landscape. Simple stated, the insane, anti-growth regulatory and tax regime in the EU is killing the continent’s banks. And another big part of the problem facing EU banks and industrial companies alike, of course, is the tax known as negative interest rates.

When Fiat Chrysler (FCAU) and Groupe PSA, the owner of Peugeot, agreed in October to combine forces to create the world's fourth-largest carmaker by production volume, this was not a sign of the impact of global warming on consumer preferences. Instead, two of the least efficient players in the auto industry in Europe were finally forced to consolidate in an industry with chronic overcapacity. Look for more combinations in coming months, particularly in Europe.

Sales in the global auto industry peaked two years ago over 80 million vehicles, leading many observers to predict the imminent collapse of the sector. But what really seems to be at work here, in our view, is more of a normalization of production and demand to lower levels. The past decade of manic increases in vehicle sales were driven by low or negative interest rates, but the impetus for further growth seems to be ebbing fast. Notice that US sales of cars and light trucks has gone sideways since 2016.

A decade ago, when US auto sales were limping along at 10 million units annually, the US auto sector was in danger of extinction. The fixed costs involved in making vehicles could not support three independent US automakers at this level of volume. As we wrote in “Ford Men: From Inspiration to Enterprise,” the departure of Lee Iacocca from Ford Motor in 1978 led to Chrysler surviving as an independent producer for another three decades. The persistence of Chrysler and the acquisition by Fiat in 2014, in turn, weakened Ford Motor and General Motors (GM).

With the US auto industry now operating at over 17 million vehicles per year, however, many observers have come to believe that this level of production is “normal” and sustainable for North American sales of light vehicles. That may not be the case. The expansion of non-housing debt helped to fuel the boom in auto sales since 2014. The availability of credit has driven the surge in auto production in North America to almost 18 million units.

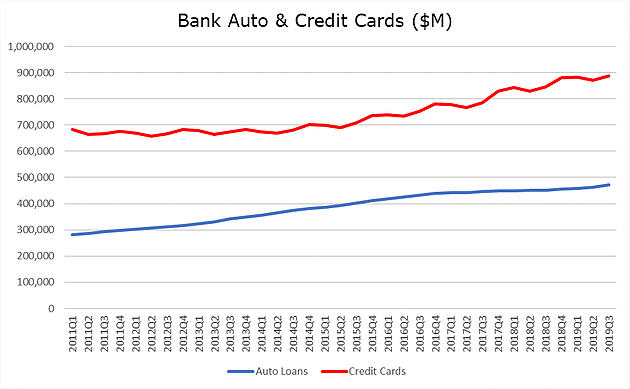

The FRBNY reported in November that total auto debt, including $475 billion in bank owned auto loans, is $1.3 trillion. The auto loan asset class has basically grown by one third over the past decade. Or to put it another way, subprime auto loans account for about half of the $1.6 trillion in asset-backed securities tracked by SIFMA. Total household debt is now $1.3 trillion higher, in nominal terms, than the previous peak of $12.68 trillion in the third quarter of 2008, according to the FRBNY.

“New credit extensions were strong in the third quarter of 2019, with auto loan originations reaching near-record highs and mortgage originations increasing significantly year-over-year,” said Donghoon Lee, research officer at the New York Fed. “The data suggest that households are taking advantage of a low-interest rate environment to secure credit.”

So, is the US auto sector facing the apocalypse? No, but you may indeed see sales dip back toward 16-17 million units in North America. And expect some frightful restructuring of automakers in Europe, including the operations of US automakers. Auto makers globally are reducing headcount at the fastest rate since the 2008 financial crisis, a year before both GM and Chrysler filed bankruptcy. We may indeed see further acquisitions and some restructurings in the auto sector in 2020. Our bet: Look for Ford to eventually cut a deal to combine with a major European automaker.

The ongoing restructuring of the global auto sector will be accompanied by an accelerating consolidation of the banks, particularly outside the US.

The hostile business and regulatory environment in the EU is killing the banking system in Europe, but the politicians there seem to be largely indifferent.

Unless and until leaders in Europe and Asia reject the insanity of negative interest rates and start to focus on the real problem -- namely excessive public sector debt -- banks in Europe will remain an endangered species and, to us, unsuitable for investors of any stripe.

EDITOR'S NOTE

This Hedgeye Guest Contributor piece was written by Christopher Whalen, author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington. This piece does not necessarily reflect the opinion of Hedgeye.