Below is an excerpt from a new Demography Unplugged research note written by Hedgeye analyst Neil Howe. Click here to learn more.

| America’s public-sector pension schemes have a serious problem: The average scheme is only 72.4% funded. Despite efforts to ramp up contributions, the collective shortfall equals an eye-popping $1.6 trillion and will grow even bigger if the market takes a dive. (The Economist) |

I say this periodically, and I'll say it again.

State and local pensions are a volcano waiting to erupt.

The only question is:

Who is going to get hurt by the explosion? (See "America's Pension Battle Heats Up" and “Why Are Public Pensions So Messed Up?”).

Policy experts often report the size of this bulging volcano to be about $1.6 trillion (the official aggregate unfunded liability, computed by the Center for Retirement Research and quoted by The Economist). But this figure embodies a lot of optimism. It is based on GASB (Government Accounting Standards Board) rules that allow government agencies to discount their future liabilities at whatever rate of return they hope to get from their financial assets--something that would never be allowed in the private sector (per FASB).

If we discounted S&L plans at the same rate used by private firms (now about 4.5%), the unfunded liabilities would be over $3 trillion. If we used risk-free Treasuries of matched duration--maybe because some states constitutionally guarantee their pension benefits--then the figure would be well over $5 trillion.

How did we get into this mess? It started with a big expansion of state and local government back in the 1960s and 1970s, which meant hiring millions of young Boomers. And now those Boomers are retiring. It got worse through decades of benefit expansions (which rewarded politicians but added nothing to current outlays).

Add to that greater-than-expected longevity and disability. Add to that decelerating public employment. Then add further to all of the above a massive shift in pension assets from fixed income to equities, which allowed ever-higher discount rates and created the appearance of ever-smaller liabilities. Prudent accounting might have prevented the problem, but (again) the GASB rules are lax and S&L governments are under no obligation even to follow GASB.

As recently as 2001, S&L pensions as a whole--newly glutted as they were with equities at the peak of the dot-com bubble--were officially in surplus. But their net liabilities surged over the next two recessions--without falling much during the subsequent recoveries. (See the first chart below.) The average official funding level fell from 100% in 2001 to just over 70% by 2016, even while employer contributions, imposed by agencies struggling to catch up, were jacked up from 5% to 17% of payroll on average. (See the second chart below.)

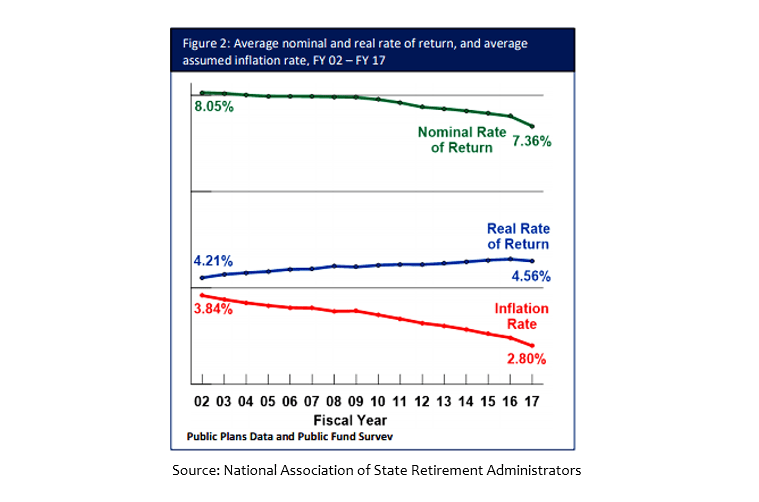

Since the Great Recession, S&L pension funds have lowered their average assumed nominal rate of return from 8.0% to 7.4%. But this decline doesn't reflect greater realism. More than all of it comes from lower assumed future inflation, which has little effect on net liabilities.

Meanwhile, the funds' assumed real rate of return has actually risen still higher as even more money gets pushed into hedge funds, private equity, real estate, and commodities. Astonishingly, these alternative asset types now comprise a greater share of S&L pension assets (27%) than fixed income (24%). (See the third and fourth charts below.)

Complicating the overall negative trend is the growing disparity between well-funded states, like South Dakota, Tennessee, and Wisconsin, and poorly-funded states with deteriorating balances, like Illinois, Kentucky, and New Jersey. In the best three, the average employer contribution rate is 8%. In the worst three, it is 32% and rising, even while the funding ratio in these states lingers below 40%.

Such is the variety and multiplicity of individual plans--there are roughly 5,500 of them--that no one knows which ones will first get into big trouble. Most likely, many will go at once during the next economic or financial crisis. And most likely, it will feature plans in the 24 states that are less than 70% officially funded. (See remaining charts.)

So who will get hurt? In extremis, the retirees themselves may get hurt--since in an emergency S&L governments can and will cut benefits if total pension outlays threaten to choke off basic public services to citizens. But don't expect much savings from this source.

Inevitably, most of the pain will be inflicted on the younger generations who reside in the state, county, or city. S&L employees will get paid less so that agencies can afford the huge payroll contribution fees needed to amortize past liabilities. Or local residents will get fewer services. Or be asked to pay higher taxes. (Meanwhile, the pensioners themselves are free to live somewhere else--like maybe a sunbelt state with no funding issues.)

We can already see some of this happening in California, where CalPERS is now requiring schools to push up their pension contribution for teachers from 18% to 35% of payroll by 2021. And new projections show that the rate will have to rise further to 38% and stay there into the 2040s. Why? To pay unfunded teacher pension liabilities. If you're a teacher, this may squeeze your take-home pay. If you're a parent, this may dim your view of what you're getting back from your taxes.

In the most underfunded states, I do see a tendency to defer endlessly the much-higher contribution rates needed to achieve full solvency. Some think tanks are justifying this by saying, well, so long as these plans never actually run out of money, they don't really ever need to re-achieve full funding. The idea, I guess, is that these states can adopt a sort of pay-as-you-go funding arrangement (like Social Security).

But there's a problem with this sort of "paygo" approach. Yes, it lightens the near-term tax bill. But it also generates a lower long-term rate of return on contributions than a funded plan, and--more seriously--it makes the system fatally vulnerable to population flight. At some point, even younger residents will see no point in sticking around in states where they're getting a worse deal and their taxes are going to pay for past liabilities. Especially since they will be paying for a generous and guaranteed menu of "defined benefits" to Boomers that almost no Millennial or Xer can expect to receive at the end of their own private-sector employment.

Indeed, this population flight may already be happening. (See "The 'Superstar' Metro May Be Fading.") Michigan may (with great effort) bail out Detroit. But who's going to bail out New Jersey or Connecticut or (even) California? The Economist calls Illinois "America's Greece." Care to see a Puerto-Rico style triage in Kentucky? There's an irony here. When stuff happens, the same states that have always proudly asserted their constitutional independence from any sort of federally mandated accounting standards will no doubt be pounding on the door of Congress, begging for mercy.

* * *

ABOUT NEIL HOWE

Neil Howe is a renowned authority on generations and social change in America. An acclaimed bestselling author and speaker, he is the nation's leading thinker on today's generations—who they are, what motivates them, and how they will shape America's future.

A historian, economist, and demographer, Howe is also a recognized authority on global aging, long-term fiscal policy, and migration. He is a senior associate to the Center for Strategic and International Studies (CSIS) in Washington, D.C., where he helps direct the CSIS Global Aging Initiative.

Howe has written over a dozen books on generations, demographic change, and fiscal policy, many of them with William Strauss. Howe and Strauss' first book, Generations is a history of America told as a sequence of generational biographies. Vice President Al Gore called it "the most stimulating book on American history that I have ever read" and sent a copy to every member of Congress. Newt Gingrich called it "an intellectual tour de force." Of their book, The Fourth Turning, The Boston Globe wrote, "If Howe and Strauss are right, they will take their place among the great American prophets."

Howe and Strauss originally coined the term "Millennial Generation" in 1991, and wrote the pioneering book on this generation, Millennials Rising. His work has been featured frequently in the media, including USA Today, CNN, the New York Times, and CBS' 60 Minutes.

Previously, with Peter G. Peterson, Howe co-authored On Borrowed Time, a pioneering call for budgetary reform and The Graying of the Great Powers with Richard Jackson.

Howe received his B.A. at U.C. Berkeley and later earned graduate degrees in economics and history from Yale University.