The verdict is in—the Fed wasn’t dovish enough.

As you know, the Fed cut rates 25 basis points this week. But the future path for rates is murky at best. There’s more than a fair amount of dissent on the FOMC.

Take a look at the “dot plot” (individual Fed governors’ interest rate targets) for the end of 2019.

Here’s what’s happening:

- Five members approved of the 25 basis point cut (but those same governors expect rates to hold steady at the current target of 1.75% to 2% for the rest of the year)

- Seven members favor at least one more cut by year end

- Five members think rates should end 2019 between 2% and 2.25%

So what’s next?

Outspoken former Fed advisor Danielle DiMartino Booth has an interesting idea you should consider. She discussed it during a new discussion with CEO Keith McCullough (just before this week’s rate cut announcement):

|

"I think Powell’s dream would be for it to be two [rate cuts] and out… I think he wants out of the cutting cycle. I don't think he wants to get dragged into the negative interest rate debate. I don't think he wants to follow Mario Draghi down that rabbit hole. I think he liked it when rates backed up last week. He's a bond vigilante at heart.” |

This conversation is a must-watch if you’re interested in learning what Fed Chair Powell is watching (and why) to determine the future path of rates.

Below we’ve transcribed an important excerpt from DiMartino Booth’s discussion with McCullough.

* * * *

Keith McCullough: Hi, I'm Keith McCullough. Welcome back to another Real Conversations. This is going to be a wild and exciting one. I’m here with Danielle DiMartino Booth, who's founder of Quill Intelligence.

Let’s get right into it. Everyone probably wants to hear you preview what you think is going to happen at the FOMC meeting tomorrow. So let’s start there.

Danielle DiMartino Booth: So there's going to be a quarter point rate cut. No surprises. We know that's happening. I think Powell’s dream would be for it to be two [rate cuts] and out. I think that if he tries to indicate that in the press conference, he’ll be testing markets.

McCullough: You think he’d like that?

DiMartino Booth: Oh, I think he wants out of the cutting cycle. I don't think he wants to get dragged into the negative interest rate debate. I don't think he wants to follow Mario Draghi down that rabbit hole. I think he liked it when rates backed up last week. He's a bond vigilante at heart.

On the face of it, he's got every reason to be hawkish at the press conference. Except for this little thing called the attack on the Saudi refineries or GM striking for the first time since 2007.

McCullough: Remind me. What happened in 2007?

DiMartino Booth: Oh, I don't know. The repo market completely seizing up and then the Fed having to come in and rescue it today. So aside from those couple of things going on I think Powell would prefer to talk about green shoots.

McCullough: We don't want to go down this rabbit hole on the repo market, but a lot of people are asking about it today because it happened. Can you talk about this for a bit?

DiMartino Booth: We know about banks try to push down their reserves at the end of the quarter and at the end of the year it becomes most acute. We know about window dressing. So there's always going to be this pressure building.

But by the same token, you've got a lot of other factors. You've got foreign central banks that are parking reserves at the Fed because the reverse repo rate pays more and is higher than what they can get just by sitting on T-bills. And there's a collateral issue. Basel III has got unintended consequences because banks can't hold what they used to hold. And that can take off on another whole tangent then about bond ETF liquidity.

Still, I think there's a lot more going on here than just quarter end and year end. I think it has to do with cycle end and the market trying to figure out what the limits of liquidity truly are. It's all about the liquidity.

McCullough: You hold that it’s all about the cycle and liquidity as where you've been on this. For me, I don't hang my hat on making a big recession call because I don't need to. You can make a lot of money on the long side of treasuries or gold and on the short side of stocks. You just have to be right on the late cycle of it all.

Danielle, I’m checking out your Twitter stream. Her tweets are wicked good. The first one actually has to do with this, what are the corporates, what do the CEOs think about late cycle?

DiMartino Booth: I hear a lot that the consumer's doing just fine. That's great. But credit card spending is going through the roof, which explains the July Retail Sales strength.

But if I'm in the C-suite, my chief concern is that I'm in the late cycle and my second concern is wage inflation. You know you have to cut costs. You know, your labor costs are too high. All you have to do is marry the two and say layoffs. Yup. We're just going to trim headcount. And it's as simple as that. I think CEOs and CFOs know what's coming.

We’ve had massive benchmark revisions to nonfarm payrolls. We're like, ‘Whoops, we miscounted. Sorry.’

McCullough: They never miss out the other way.

DiMartino Booth: Exactly. We've had five back to back revisions to nonfarm payrolls to the downside. The first thing they taught me at the Fed was monetary policy works with a lag of nine to 24 months. The second thing they taught me at the Fed was if you're looking for an inflection point in an economic cycle, look for three revisions to nonfarm payrolls, one way or the other. You're coming out of recession, or you're going into recession if you get three. If you get four, that's kind of a fact.

McCullough: But three in a row would be what I would call a trend. I always define a “trend” as three months or more.

DiMartino Booth: It's a trend of downward revisions. That's looked at as an inflection point in the economic cycle. You get to four, it's a fact. You get to five. That's the fact Jack. And CEOs know this. They know it. They're seeing it. And the only person who is not seeing it, because by the way, Jay Powell gave a speech in Zurich the day nonfarm payrolls came out and he knew that there were five months in a row of downward revisions and he just got up to the podium and said, ‘We have a very strong labor market.’ I'm like, God love you Jay Powell.

McCullough: Powell said that? Former Fed chair Janet Yellen wouldn’t have missed that with her 19 indicator labor market model that she uses.

DiMartino Booth: Oh, she threw that away. You forget that. I was there when she threw the baby out with the bath water because it turned against her.

McCullough: Getting back to your point about CEOs and the labor market, let’s throw up a slide on this because I like to contextualize where we’re going here. On this slide, you show pretty simply on the left side, we show jobless claims, which has only gone down for the last decade. So anybody under the age of 35 on Wall Street just thinks that this goes down all the time. This is in the face of the opposite of thing, which is earnings only going up on the right side, consumer confidence looks just like the stock market. So what could possibly go wrong? One could go up and the other one could go down.

DiMartino Booth: Right.

McCullough: And what you notice is that jobless claims don't go up slowly. They go up all at once and it's been in waiting like that forever now. So that’s the point, I basically just make the argument that earnings go negative year over year. That means that you have to fire people. So jobless claims will start to go up. It's not a crazy forecast to make.

DiMartino Booth: It’s not crazy. And it's pretty simple math to do, but because we’ve had really bad monetary policy throughout the entire recovery, we've had sclerosis in the labor pool and therefore companies have been much more remiss to let go the labor they fought so hard to get. So we're seeing stickiness in jobless claims that we wouldn’t otherwise.

McCullough: But that happens 100% of the time at the end of the cycle.

DiMartino Booth: Right. But this is the longest labor market expansion in US history.

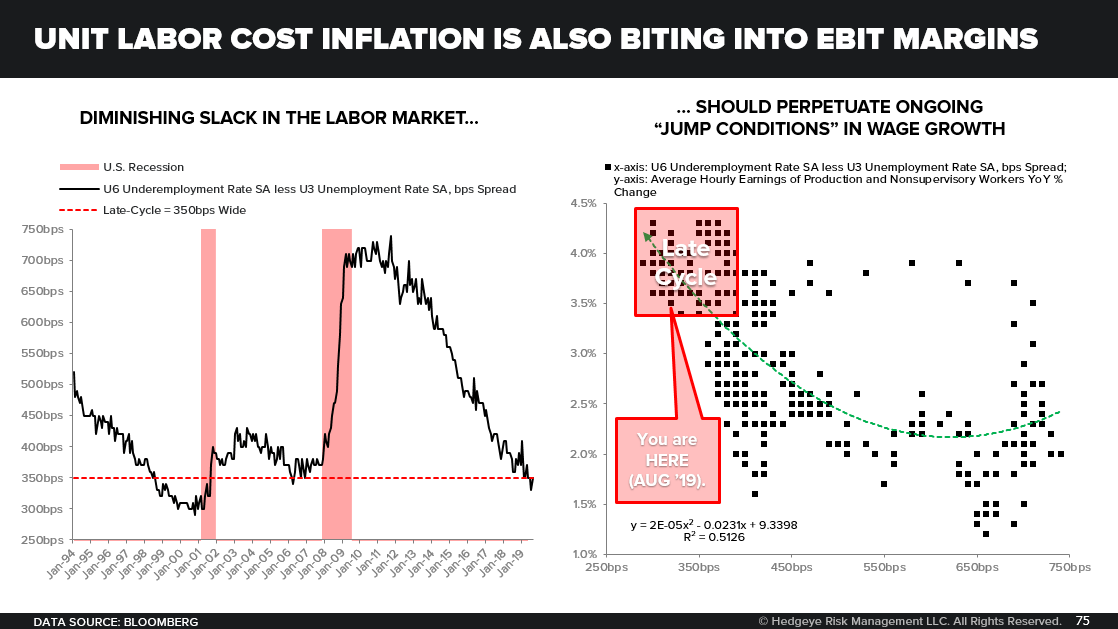

McCullough: Let’s look at another chart, Danielle knows this one too. This shows a simple relationship, which is U6 minus U3. You're the only person I'll talk to on TV that knows what that is. But again, U6 is a measure of the underemployed and U3 is the traditionally quoted unemployment rate. What this shows is that employers are overpaying at this point of the cycle for part of the labor force that’s never been paid.

DiMartino Booth: They're both off their lows.

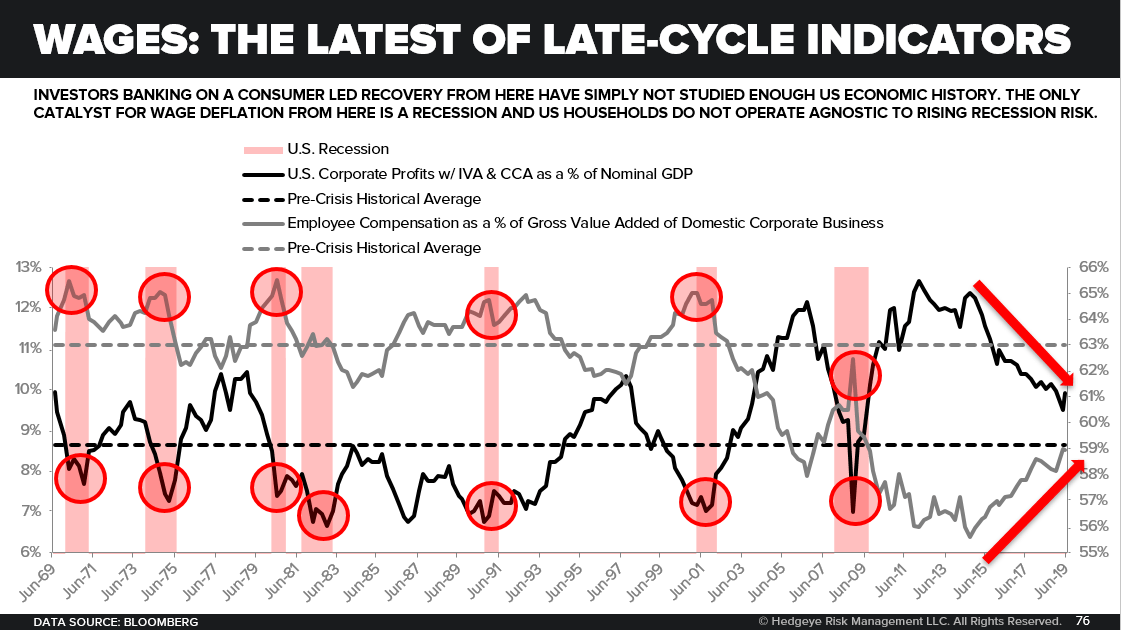

McCullough: Yes. But generational lows, like if you go to the next chart, you see labor versus capital. Labor has never, that's labor against capital going all the way back to the late 60’s.

If you look at this chart, it's never the gray line, which is Labor, has never come off these lows. It was always high and rising. If you look at the 80’s and 90’s that's why people like Reagan and Clinton. The people were getting paid and profits are the upside down of that.

So I always go back to this and I say, ‘What could possibly go wrong? It's going in the opposite direction where it should, but it's coming from the most asymmetric point.’ So now what? How does the Fed deal with that? What is there a model at the Fed that says jobless claims rising and corporate profit recession equals let's try to be done after two cuts?

DiMartino Booth: It surely should not equate to a mid-cycle adjustment.

McCullough: It's certifiably bananas.

DiMartino Booth: It is. It really actually is. And it, and it goes against again what the Fed teaches you on Day 1, which means that they're either in denial or trying to put a good public face on this.

McCullough: What do you think that they're trying to put a good public face on?

DiMartino Booth: Well, I think that they know that this is a confidence game. Jay Powell understands that he has to keep credit volatility contained.

McCullough: That's a big thing and he has to do it at all costs.

DiMartino Booth: Yes. At all costs.

I'm sure the day of the Ford downgrade, Powell probably has a nervous tick thinking, ‘Here's another big debtor in the market being downgraded after what happened with General Electric.’ Publicly, they’d probably say it was only Ford's first downgrade to junk. It was GE’s second.

McCullough: Very stable industry across U.S. economic history.

DiMartino Booth: Oh yeah, Standard and Poor's has come out with a new report today that says the global auto industry is going to stay in a slump in the next two years. And GM is striking. There is so much evidence the Fed is choosing not to see. It's frightening.

I think that in Powell’s mind, at least, keeping confidence high right now, keeping the stock market high is priority number one because the stock market has never been as tethered as it is to the real economy.