The Short Case on American Express Has Grown More Compelling

We hosted the latest installment of our initiative to take on the large and still growing payments industry last week. We offered a fresh perspective and detailed contextualization of the risk and return profiles underlying the various players in the space. If you are an institutional investor interested in accessing our entire, deep-dive slide deck email sales@hedgeye.com.

Having begun with a thorough study of the industry's largest two players, Visa (V) and Mastercard (MA), we next look beyond the 4-party transaction model and in the direction of the closed-loop networks, beginning with the largest and most recognized closed-loop player, American Express (AXP).

While we have previously shared our thoughts on the relative prospects of American Express, we offered a thorough, refreshed look at the short case on AXP, which in our view has since grown more compelling.

KEY POINTS OF DISCUSSION

- Rewards costs, associated rewards service costs, contra revenue and marketing spend, when viewed in the aggregate, have grown very quickly in the last few years. Accounting changes have helped to obfuscate the magnitude of those cost increases. While this spend has helped to fuel solid top-line growth it begs the question whether this level of ongoing spend ramp is sustainable, and, if not, whether revenue growth will come under growing pressure in the future.

- Has AXP's target market of affluent, high-income earners been compromised by the entrance of large issuers with capital to deploy and expanded revenue opportunities to offset the increased cost of rewards programs? Can brand value combat this large and persistent competitive threat or has American Express' product offering reached full commodity status?

- Is AXP's purported value proposition of higher spending cardholders proving less convincing for merchants and increasingly unable to justify its higher fees? As Visa and Mastercard, with their lower transaction costs, continue to expand acceptance among cardholders, do merchants face any significant consequence in forgoing American Express acceptance?

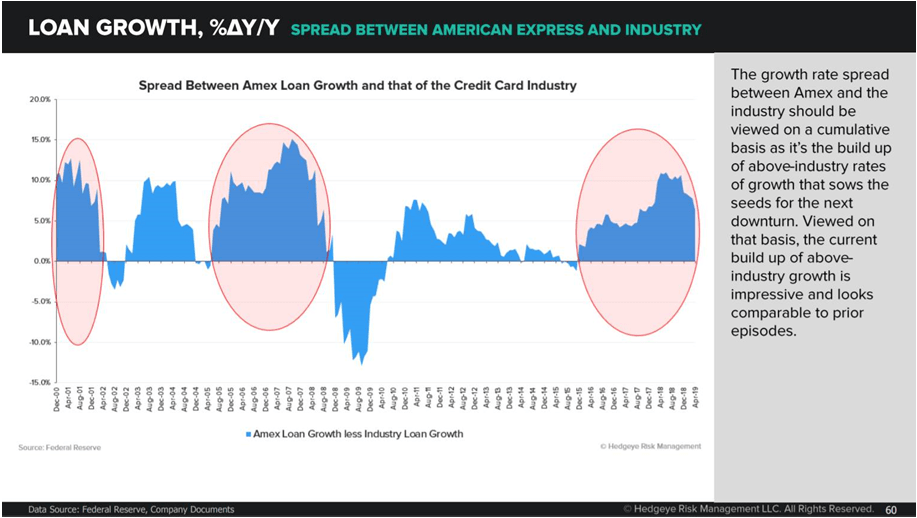

- With mounting pressure on the core business, can the pursuit of increased lending reliably drive sustainable future growth despite being more capital intensive, more cyclical, and lower return than the payments business?

- Alternatively, do bearish sentiments carry enough merit to dissuade investors from a stock trading at a slight discount to the S&P 500, with persistent mid-single digit, fx-adjusted revenue growth still largely achievable, and bolstered by strong capital return in the form of a ~3% annual share buyback and 1.25% dividend yield?

|

Email sales@hedgeye.com for institutional access.