Editor's Note: Below is a brief complimentary excerpt from a new, deep-dive research note written by Demography analyst Neil Howe. To get a special deal on his new product Demography Unplugged click here.

TREND WATCH: What’s Happening? The spread between long- and short-term bond yields, after narrowing for more than two years, is now turning negative. This worries investment advisers—since “yield curve inversion,” perhaps the most ominous phrase in the financial lexicon, has directly preceded each and every recession since Elvis recorded “Heartbreak Hotel.” Others aren’t convinced that the term spread-business cycle relationship will hold up this time around, for reasons including the strength of the economy, QE, the low level of interest rates, and negative “term premia.”

Our Take: The arguments of the critics aren’t persuasive. The term spread reflects a rich variety of business-cycle dynamics—everything from central bank policy-setting, the timing of firm capex, and bank lending to consumer sentiment and rational investor expectations about the future. So when the yield curve inverts, the negative term spread cannot be explained away by any one errant variable. All eyes are now on the Fed, which doesn’t want to lose face by cutting rates again so soon after raising them. Markets, on the other hand, expect the Fed to do just that. Alas, it may be too late for the Fed to avert recession no matter what it does.

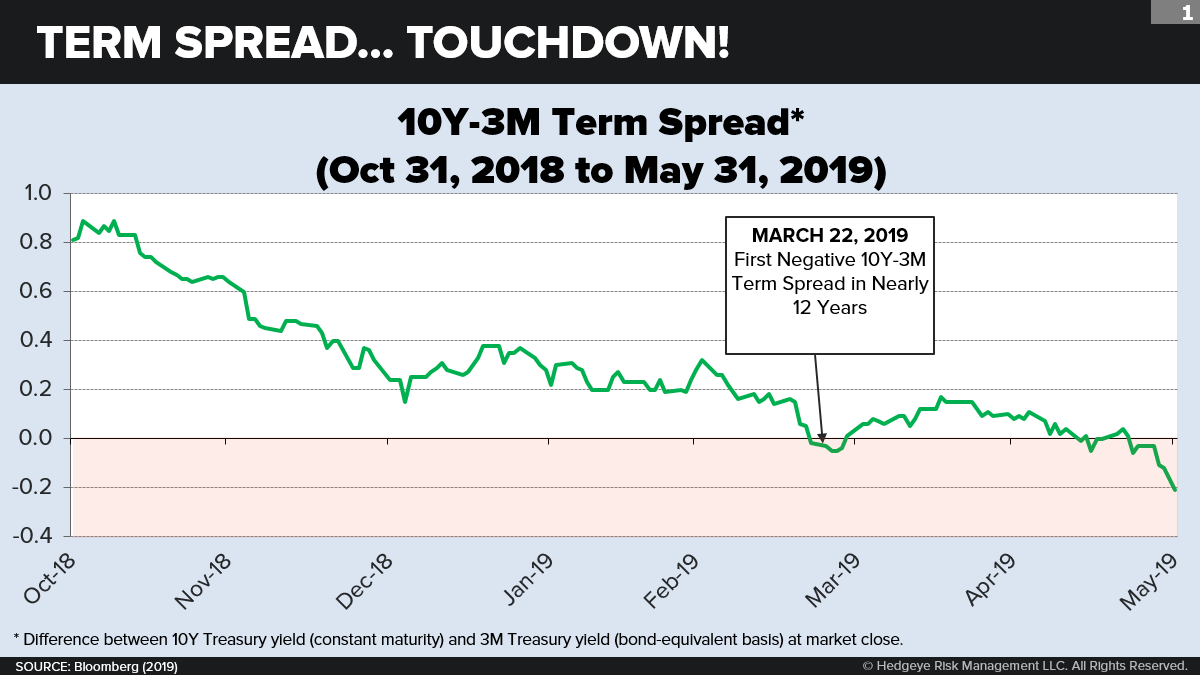

TERM SPREAD... TOUCHDOWN!

Like a flying stone starting to skip on the water, the long descent of the term spread (10 year minus 3 month) is at last beginning to turn intermittently negative.

Two months ago, on March 22, 2019, the spread turned negative for the first time in nearly 12 years (since August 27, 2007, to be exact). It stayed negative for six market closes in a row, until March 28. Then it went positive again. A couple of weeks ago, it went negative on two daily closes (May 13 and May 15). Now, two days before Memorial Day weekend, it went negative and—thus far—is staying negative.

As of market close today (Friday), the spread hit negative 21 basis points. The stone, at last, may have stopped skipping and started sinking.

We anticipated this was likely to happen ten months ago. (See “The Power of the Spread.”) In this note, we “revisit” the term spread.

Let’s cut to the chase. What does this yield curve inversion—or any yield curve inversion—have to do with the timing of the next recession?

SUBSCRIBE TO GET FULL ACCESS