THE HEDGEYE EDGE

Three of our top four shorts in the Restaurant Sector are in the Casual dining sub-segment.

We have been saying for months now that the aggressive discounting at Applebee’s is disrupting the Casual Dining industry. One quick example of how the value discussion has changed over the past 12-months occurred on the Brinker International (EAT) conference call.

During the 2Q18 conference call, the word ‘value’ was mentioned 11 times, and now 12-months later on the 2Q19 call ‘value’ was mentioned 38 times. Driving the value proposition for Chili’s is the 3 for $10 platform and we heard that the program “is a relevant and compelling offer that's sustainable into the foreseeable future.” If this is to be true, what will the margin structure of the company look like going forward?

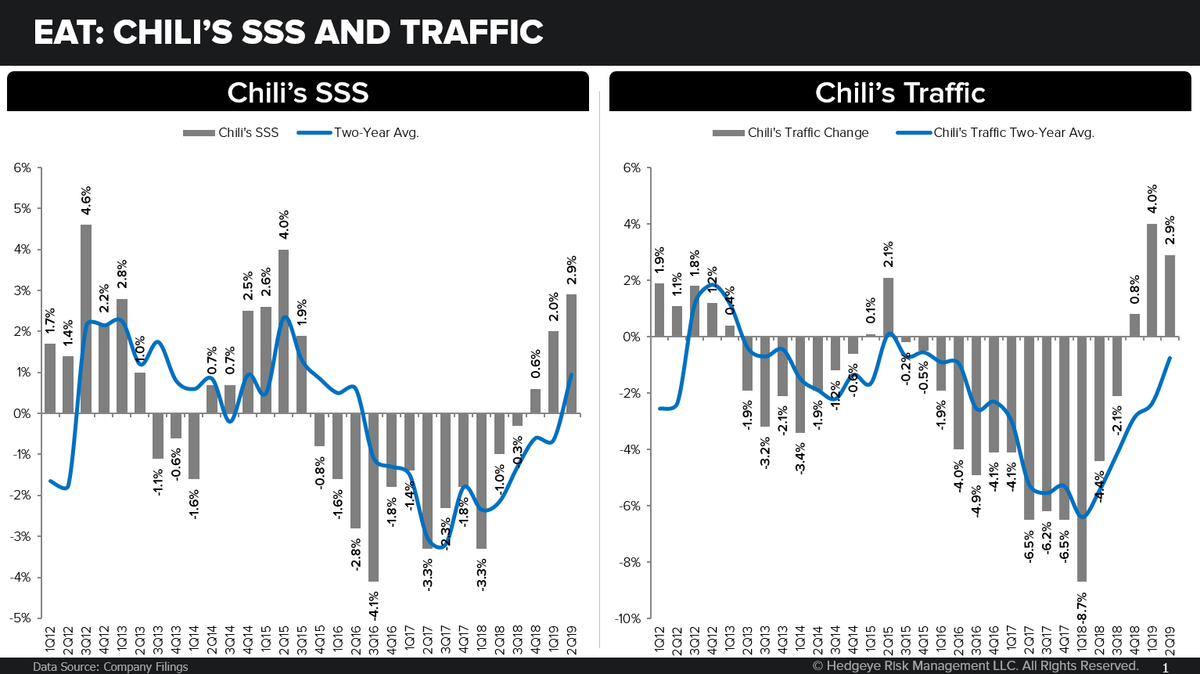

THE GOOD NEWS: TRAFFIC HAS IMPROVED

The good news is that the focus on value has improved traffic at Chili’s. In 2Q18, Chili’s traffic was (4.4%) or (5.5%) on a two-year stack. Today, Chili’s reported traffic is up 2.9% or (0.8%) on a two-year stack. The menu simplification has clearly helped drive traffic, but the value of the 3 for $10 offer has driven the value seeking customers back to Chili’s. Now we must ask the question, are these value seeking customers the type of customers Chili’s is seeking?

BUT AT WHAT COST?

The bad news is that all the focus on value is lowering marginal profitability. In 2Q18, on a trailing 12-month basis restaurant level margins were 15.4%, they are now 150bps lower, including the impact of the sales leaseback. We currently don’t see a pathway for margins to improve from current levels and some downside remains if the value promotions continue to gain preference.

CASH RETURN CYCLE IN THE REAR-VIEW

Management has done what it can to return cash to shareholders over the past three years. The balance sheet has the appropriate amount of leverage, so it is unlikely that another big share repurchase program is in the immediate future.

ELEVATING CAPEX

In FY19, EAT is embarking on a 3-year remodel program, which has some negative implications for the P&L in FY19. In short, expenses are rising without the benefit to the top-line. It will not be until 18-24 months from now where the sales will be growing faster than expenses.

We commend the progress the company has made growing traffic, we would like to see sentiment settle into the new normal before we get more positive on the stock.

ONE-YEAR TRAILING CHART