This commentary was written by Dr. Daniel Thornton of D.L. Thornton Economics.

The Federal deficit in 2018 was $1.09 trillion, the second deficit in the last three years and the sixth in the last 10 years to exceed $1.0 trillion. The deficits for the other four years were large, averaging $583.4 billion. During the past decade the public debt doubled, increasing from $7.5 trillion to $15.8 trillion. The total public debt, which includes the debt the government owes itself, i.e., the Social Security, Medicare, and other so-called trust funds, is now $21.9 trillion. This might not be so bad if we could blame the recent massive deficits on the financial crisis and recession, but we can’t. These large federal deficits are just the most recent and most egregious in a trend that began about 1970. This essay explains the why the deficit/debt problem is going to be so difficult to solve; which, in turn, explains why Congress has buried its head in the sand in the hopes that somehow the problem will just resolve itself. Indeed, some in Congress and others running for public office are proposing new programs that will exacerbate the problem.

To understand the deficit/debt problem, it is useful to see how different the last 50 years have been relative to the previous 170 years. Figure 1, which is from an article I published in the Federal Reserve Bank of St. Louis Review in 2012, shows government deficits from 1800 through 2011 as a percent of the economy’s output (in either Gross National Product, GNP, or Gross Domestic Product, GDP—the measure that we’ve used since 1991), and the Congressional Budget Office’s (CBO’s) 2011 projections to 2020. Historically, most large

deficits were associated with war; the large deficit shown between WWI and WWII was due to the Great Depression when the deficit peaked at 6.6 percent of GDP. With that exception, between wars the government tended to run surpluses both in absolute terms and relative to the economy’s output.

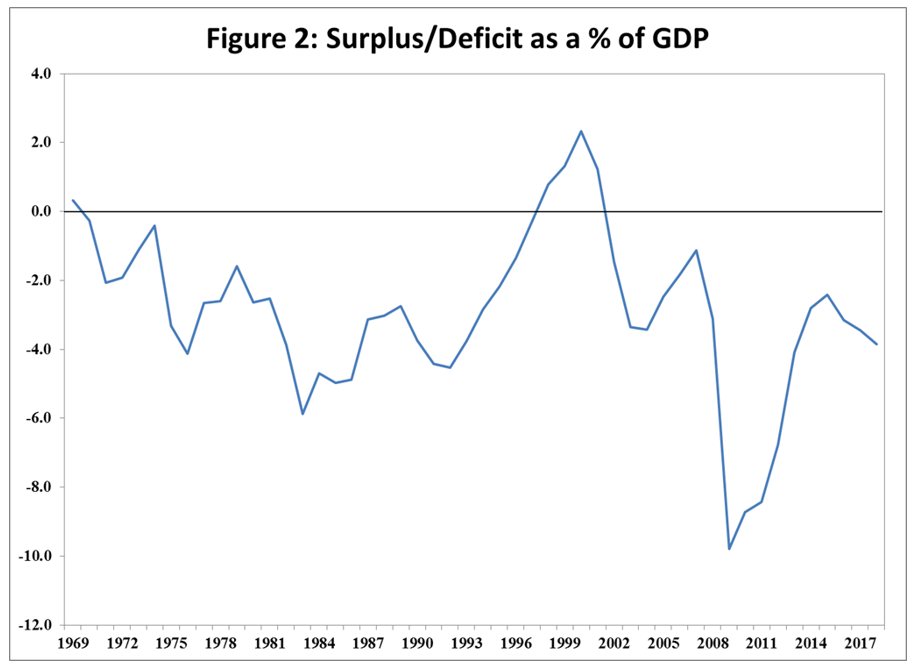

Prior to the financial crisis and recession, the CBO was projecting a budget surplus up to 2011. Despite the fact that the financial crisis and recession had ended by 2011, the CBO projected continuous deficits leveling off at about 3 percent of GDP out to 2020. Of course, that’s not what happened. Figure 2 shows the federal surplus/deficit as a percent of GDP from 1969 through 2018. There was a small surplus in 1969. With exception of the four years from 1998 to 2001, only deficits. The periods 1973-75 and 1980-1982 are associated with

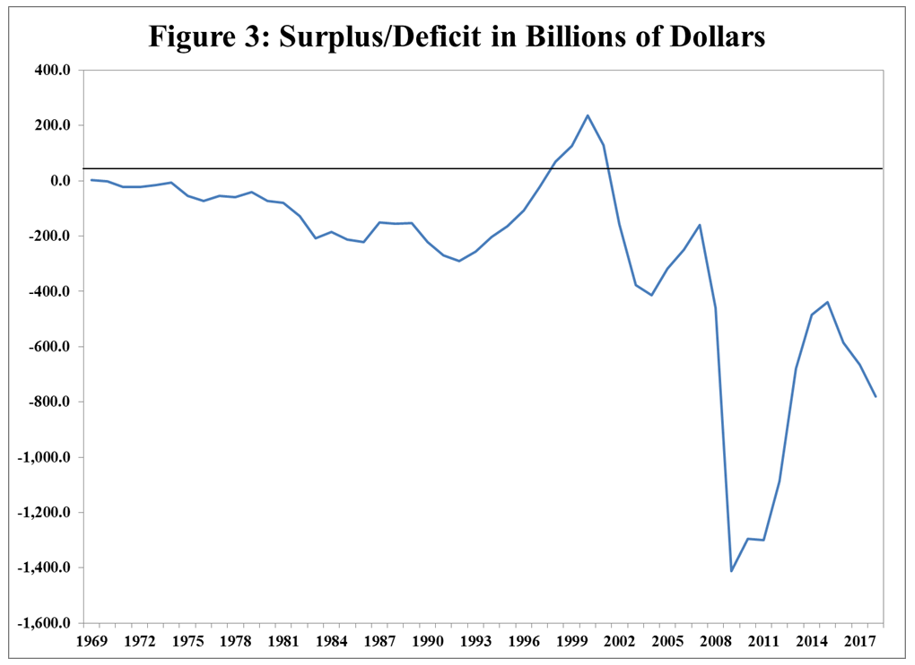

recessions. But the large and accelerating deficits shown in Figure 2 cannot be blamed on declines in output. This is obvious from Figure 3, which shows the deficits in billions of dollars. While the deficits through mid-1970 appear smaller than in Figure 2, they are large by non-war historical standards and they grow over time. More important for the point being made here, the enormous deficits from 1983 to 1999 occurred during an extended period of economic expansion that was punctuated by a very mild recession, which lasted just eight months. That the deficit/debt problem is accelerating is also witnessed by the fact the deficits averaged 5.3 percent during the most recent economic expansion, an expansion that is on a path to be the longest in the post-war period.

There can be no doubt that the deficit/debt problem has been accelerating since 1970. In a Wall Street Journal op-ed piece on February 1, 2015, Dennis Teit, who retired from the House Budget Committee, argued that the post-1970 deficits occurred, and will continue to occur, because in the mid-1970s Congress “elbowed” the president aside. Specifically, when Nixon impounded funds that Congress wanted to spend, Congress passed the Budget and Impoundment Act of 1974 which, among others things, specified that the president may request that Congress rescind appropriated funds, but if the request is not approved by both the House and the Senate within 45 days, the funds are dispersed (see Thornton 2015 for more details). However, it is doubtful that Teit’s explanation, per se, accounts for much of the deficit/debt problem.

To understand why, it is necessary to analyze the government’s spending. Government expenditures are classified as either discretionary or mandatory. Figure 4 shows the percentages of total government expenditures that are discretionary, mandatory, or interest payments. Discretionary spending declined from 64 percent of total spending in 1969 to 31 percent in 2018. Mandatory spending did nearly the opposite, increasing from 29 percent to 61 percent. Interest payments fluctuated a little, but averaged about 7 percent over the period.

Discretionary spending not only declined relative to mandatory spending, but grew slowly since 1969, a 1.7 percent annual rate. This is much slower than the 6.2 percent rate of increase of GDP. Discretionary spending is the spending that is most likely to be affected by the Budget and Impoundment Act of 1974. Hence,

discretionary spending is not the problem; it cannot account for the accelerating deficit/debt problem. While it may be desirable to reduce discretionary spending for other reasons, doing so will have no meaningful effect on the deficit/debt problem.

Indeed, nothing meaningful can be done to “solve” the deficit/debt problem without dealing with “the elephant in the room,” mandatory spending. In 2018 mandatory spending accounted for 60 percent of total government spending. Furthermore, this percentage is expected to grow even faster for the foreseeable future.

Mandatory spending is not part of the budgeting process. The Treasury borrows whatever amount is required to meet the mandatory spending requirements, even if the government is shutdown. Social Security and spending on healthcare: Medicare, Medicaid, the Children’s Health Insurance Program, and subsidized health insurance purchased under the Affordable Care Act (hereafter, collectively SSMM) currently account for the lion’s share of mandatory spending, 78 percent. Civilian and military retirement and veterans programs make up the rest. Figure 5 shows SSMM in billions of dollars and as a percent of all mandatory spending from 1969 to 2018. SSMM has increased rapidly from $24.3 billion in 1969 to $1.8 trillion in 2018—9.2 percent per year; 3 percentage points faster than GDP. [The SSMM spending presented here is net of the taxes that are paid into to these programs. For example, expenditures on Social Security are net of Social Security taxes]. In contrast, the rest of mandatory spending increased at an annual rate of just 2 percent. Hence, the accelerating deficit/debt problem since 1970 is entirely due to SSMM spending.

Unfortunately, these numbers significantly understate the magnitude of the accelerating deficit/debt problem. The mandatory spending programs also represent promises the government has made to provide income and/or services to future recipients. But the government doesn’t have a pool of savings from prior years that it can draw on to pay these future promises. Hence, all of the future payments that must be made are in reality unfunded liabilities. The present value of these unfunded liabilities is staggeringly large. [Present value can be thought of in two equivalent ways: (1) What the government would have to pay for these services if it were to pay them off today. (2) The amount of unencumbered assets the government would have to hold today to pay for all of these promises without increasing taxes or issuing more debt.] The Congressional Budget Office (CBO) estimates that with no changes in taxes or programs the public debt will increase from $14.7 trillion in 2018 to $27.3 trillion in 2029. Hence the CBO estimates that the government would have to have savings of $12.6 trillion today in order to pay meet its commitments through 2029. Because the CBO estimates that the deficits will increase continuously and by 2038 will be nearly 13 percent of GDP, the CBO estimates that the government would need savings of $55.7 trillion to meet its obligations through 2038. Economist Lawrence Kotlikoff’s estimate assumes an infinite horizon and, hence, it is much larger—in excess of $210 trillion.

Regardless of how you measure it, the deficit/debt problem is enormous and accelerating. It won’t go away without taking action. If the government wants to keep the promises it has made without massive increases in the debt, taxes must be increased and the increase must be very large. In lieu of raising taxes, the problem can be solved only if the government reneges on many of its promises. Again, the program cuts must be very large. Whether the government deals with the deficit/debt problem by increasing taxes, breaking promises, or some of each, the actions must be large. Minor tweaking of taxes and mandatory spending won’t do the job. Moreover, it is essential to act quickly. The experience of the last 50 years and the CBO’s analysis clearly shows that the longer the government waits to deal with the problem, the more taxes will have to be increased and/or programs be cut. Given the little effort Congress has put into solving the problem, I don’t expect to see any significant steps taken until the deficit/debt problem is much worse, perhaps critical. As is always the case in economics, the financial markets will tell us when the deficit/debt problem is critical, i.e., when it is obvious that policymakers have waited far too long.

EDITOR'S NOTE

This is a Hedgeye Guest Contributor piece written by Dr. Daniel Thornton. During his 33-year career at the St. Louis Fed, Thornton served as vice president and economic advisor. He currently runs D.L. Thornton Economics, an economic research consultancy. This piece does not necessarily reflect the opinion of Hedgeye.