The guest commentary below was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst.

Consider the irony of the American housing sector. In the District of Columbia, various pundits, market retreads and spin-meisters (many employed by hedge funds) obsessively focus on "reforming" the government sponsored enterprises known as Fannie Mae and Freddie Mac, together the “GSEs.” The third and largest GSE, the Federal Home Loan Banks, along with the fourth, the Government National Mortgage Association or Ginnie Mae, are also included in the prospective policy mix. None of these agencies are in distress or in need of financial assistance, but no matter.

Meanwhile, the US mortgage sector is undergoing a massive and truly terrible period of restructuring that conjures up biblical images of the apocalypse. Literally dozens of private mortgage firms are for sale or simply shutting down. As we have long anticipated, Ditech Holdings was forced to again file for bankruptcy protection last week. The company and its creditors are seeking bids to buy some or all of the business, but it remains to be seen whether there is any value in the remaining assets.

The big question: who will buy the Ditech reverse mortgage business, Reverse Mortgage Solutions. RMS is consuming cash to such an extent that the company’s DIP lenders had to allocate a big portion of resources -- $1 billion in working capital – to RMS as part of the bankruptcy filing. As we’ve noted in the past, Ginnie Mae as the guarantor of the bonds that hold the reverse mortgage loans, is on the hook in the event that the business is abandoned in bankruptcy. But hold that thought.

All this talk of doom and destruction in mortgage finance may come as a surprise to some readers of The Institutional Risk Analyst. After all, aren’t home prices near record levels? Loan trading in the secondary market is brisk and mortgage servicing rights or MSRs are likewise trading at all time high multiples of cash flow, around 6x annual servicing income or 6-7% yields. What’s the problem? In a word, government. And in several words, the Federal Open Market Committee.

As we noted last week, sales of mortgage loans into residential mortgage backed securities or RMBS plummeted in the fourth quarter, reflecting the difficulty faced by mortgage banks in pricing loans during the market volatility seen in November and December. And as we noted in our previous missive, new issuance of mortgage RMBS has fallen by nearly 40% since the end of September last year.

In fact, the happy campers on the FOMC came awfully close to running the good ship lollipop aground in December 2018. New securities issuance activity across many sectors basically went to zero and mortgage lending volumes fell to levels not seen in decades.

After almost touching 5% in mid-November, the 30-year fixed rate mortgage has since fallen to 4.4%, this as the yield on the 10-year Treasury note has rallied to 2.6% from a high of 3.25%. If you see Fed Chairman Jerome Powell in the hallway, please tell him that this sort of roller-coaster in terms of gyrating benchmark interest rates is not particularly helpful.

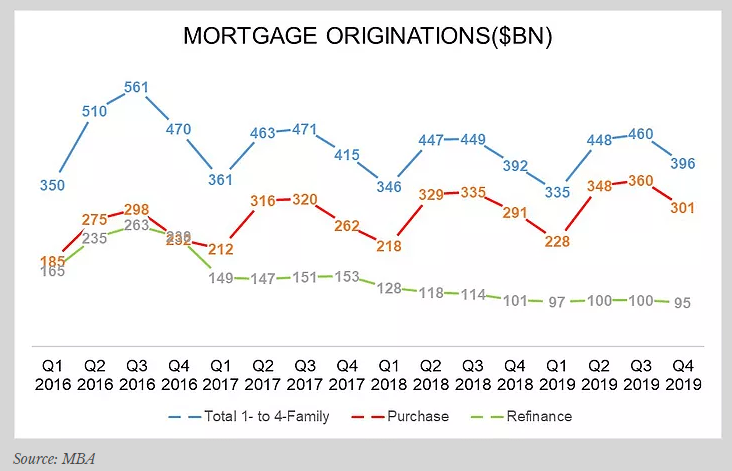

The estimates from the Mortgage Bankers Association released last week still show Q4 2018 coming it at just shy of $400 billion in total purchase and refinance originations, but based upon what we are hearing from the origination channel we’d be surprised if the actuals are not lower. See chart below showing the actuals and projections.

Now of course the mortgage origination estimates from the MBA assume that interest rates are rising. Yes, rising. The most recent projections show the 30-year mortgage at 4.8% and the 10-year Treasury note at 3%. But what if the bullish assumptions about the US economy are wrong? What if we are in fact headed into a recession or at least a period of economic stagnation?

Keep in mind that the near-5% print for the 30-year fixed rate mortgage back in November 2018 was close to the 10-year high for that key benchmark. The RESI market prices off the 10-year Treasury because it is close to the double digit average life in many pools, as shown in the chart from FRED below.

Should the FOMC actually end the runoff of the system open market account (SOMA) portfolio later this year, then assumptions about rising interest rates may need to be recalibrated.

“Federal Reserve governor Lael Brainard said she expected the central bank could end the runoff of its asset portfolio later this year,” reports Nick Timiraos at The Wall Street Journal. “Ms. Brainard said she is comfortable ending the balance sheet runoff this year because she favors an operational system with a much larger level of reserves than before the financial crisis.”

Brainard’s comment confirms our suspicion that the economist-led FOMC and, more specifically, the Fed Board of Governors, has decided to permanently nationalize the short-term money markets in the US. In effect, the Fed is discarding any hope of restoring private function and particularly unsecured lending in the US.

The decision to again grow the portfolio is being made without the advice and consent of Congress and carries with it profound implications for mortgage lenders, the REPO market and investors. But the reason for the decision obviously is the accelerating fiscal deficits of the United States.

By manipulating all manner of asset valuations, the FOMC has created two very specific risks for holders of mortgages and MSRs that are not well understood in the equity or debt markets. First, by gunning prices for homes, mortgage loans and MSRs to ridiculous levels, the FOMC has essentially created a short-put position for holders of mortgage credit and servicing exposures.

Once the FOMC resumes net purchases of government securities, long-term interest rates will fall under the dual pressure of investor demand and the artificial asset shortage that is the essence of “quantitative easing.” Like shooting heroin, once a central bank gets onto the QE habit, it is impossible to stop without deflating the financial markets. And since the Dow Jones Industrial Average and S&P 500 are the benchmarks for the political class, no deflation will be tolerated.

Second, using the forward TBA market to hedge this “SOMA Risk” may not be entirely effective because of the absurd “fair value” accounting rules brought to us by the happy squirrels at the Financial Accounting Standards Board (FASB) and the Securities and Exchange Commission. Tell us again why we need to value cash flow generating "intangibles" like MSRs every quarter please?

These same folks at FASB are responsible for the new idiocy known as Current Expected Credit Loss or “CECL,” whereby owners of 1-4 family loans have to guess the probability of default over the full life of a 30-year mortgage. Obviously such a task is impossible, but don’t tell that to the FASB and the SEC.

As benchmark interest rates fall, the modeled prepayment speeds for mortgage exposures will accelerate, this on the assumption that mortgage refinancing activity will increase -- maybe. Holders of MSRs, specifically, will be forced to take “fair value” non-cash losses on their mortgage exposures, even if they are running aggressive hedge positions.

Should the 10-year note continue to rally and perhaps get back down to a low 2% or even a 1% handle, for example, those 6x annual cash flow multiples that we see in the MSR market today will evaporate overnight. And the next shoe to drop, of course, will be credit risk, a currently unrecognized danger that is not really priced into asset valuations or the calculations of the FOMC.

Ralph Delguidice noted recently (“Bigger Balance Sheet Bullish? Really?”) that an increase in the SOMA portfolio may not actually be “stimulative” to the economy. In fact, the embedded credit risk in all of the 1-4 family mortgages that were originated during QE 1-3 may start to emerge in the next 18-24 months, pushing up the cost of servicing for holders of MSRs. If you own the servicing asset, then you are responsible for the capital cost of resolving a distressed mortgage.

“A report released… by the Federal Reserve Bank of New York revealed that the rate of delinquencies was steady at 4.65% in the last quarter, but Moody’s says this is a cycle low that will change in the coming quarters as loosening underwriting standards and rising interest rates impact loan performance,” reports HousingWire. The default and past due rates for the $2.5 trillion in prime bank-owned 1-4 family mortgages are shown below.

Assuming that Governor Brainard’s pontification about the imminent resumption of QE is correct, operators and investors in the world of mortgage finance need to take notice. With MSR valuations under the twin pressure of again falling long-term interest rates and rising capital costs of default servicing, investors could see the double digit gains in the best performing asset class in the fixed income market suddenly reversed, with catastrophic consequences for the mortgage market and certain publicly traded mortgage REITs.

Given the impending resumption of QE, investors who are long servicing need to take pause. MSRs carry both interest risk and, as many have forgotten, default risk garnished with reputational hazard. As John Dizard wrote in The Financial Times on December 16, 2018:

“If the homeowner defaults, it is up to the servicing company, i.e. the MSR holder or a sub-servicer they contract with, to persuade the homeowner to pay up, to restructure the mortgage if the original terms are too burdensome, or, if necessary, to carry out a foreclosure. You can see where MSRs can become an unromantic asset.”

So what is an independent mortgage banker to do? Lenders who are owners of MSRs need to seriously consider the following trade: 1) sell the mortgage servicing asset at the record multiples now available in the market to some willing, leveraged financial investor and 2) purchase a federally insured depository from which to safely operate a lending and mortgage sub-servicing business.

Go long a bank charter and short the capital risk in the MSR to a friendly mortgage REIT. Trade the haphazard and at times arbitrary regulation by the 50 states for the kind supervision of the Fed and FDIC. And the best part is that when defaults rise and prepayment rates accelerate, you'll be able to buy the servicing asset back at a lower valuation if you want. But we'd argue that the risk adjusted equity returns of sub-servicer + depository are superior to owning the actual MSR asset.

If our suspicions are correct that long-term interest rates are headed for another down leg, then holders of MSRs may be facing a considerable “emerging risk” to paraphrase our contributor Ralph Delguidice. They don’t teach you about such risks in the textbooks, but suffice to say that in the age of QE we might as well just throw the old corporate finance books into the trash. If you have been thinking about going short residential mortgage default risk and long a federally insured depository, then do give us a call.

Mo' Reading

Moody's: Mortgage delinquencies are on the rise

https://www.housingwire.com/articles/48175-moodys-mortgage-delinquencies-are-on-the-rise

Fed’s Brainard Says Balance-Sheet Runoff Should Probably End This Year

https://www.wsj.com/articles/feds-brainard-says-balance-sheet-runoff-should-probably-end-this-year-11550159755

EDITOR'S NOTE

Christopher Whalen is Chairman of Whalen Global Advisors LLC. He has worked in politics, at the Federal Reserve Bank of New York and as an investment banker for more than 30 years. He is the author of three books Inflated (2010), Financial Stability (2014) and Ford Men (2017).

In 2017, he resumed publication of The Institutional Risk Analyst and contributes to many other publications and media outlets. He recently launched the first volume of The IRA Bank Book, a review of the operating and credit performance of the US banking industry written for institutional investors.