The commentary below was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst.

Volatile markets have finally made policy makers start to fret about excessive leverage and sky-high asset prices, two results of years of equally excessive monetary policy. Former Federal Reserve Chair Janet Yellen, for example, worries from the speaking circuit about excessive leveraged lending and the level of corporate debt across Wall Street.

"Corporate indebtedness is now quite high and I think it's a danger that if there's something else that causes a downturn, that high levels of corporate leverage could prolong the downturn and lead to lots of bankruptcies in the non-financial corporate sector," Yellen told New York Times columnist Paul Krugman.

As with past appearances, Yellen never directly admits that some of her own policy decisions contributed to the problematic accumulation of barely investment grade corporate debt now teetering on the brink of downgrade. But she did make this remarkable concession:

"Recent research has identified possible linkages between monetary policy & leverage among financial intermediaries. It is conceivable that accommodative monetary policy could provide tinder for a buildup of leverage & excessive risk-taking in the financial system."

Bravo Janet.

Meanwhile, the US markets continue to suffer from the mounting concerns about future economic growth and, therefore, rising credit costs. Recall that the definition of a systemic event is when markets are surprised. Most categories of new debt issuance are down double digits compared with a year ago, as shown in the table below. While Treasury debt issuance is up 15% year-over-year (YOY), corporate debt issuance is down 18% and municipal issuance is down almost as much.

Notice that issuance of agency securities is also down, a result of falling lending volumes in the residential and commercial mortgage sectors. Some of the paper that might have been packaged and sold into the agency market in past years is now being retained in portfolios or sold into private deals. Note too that the issuance of asset backed securities is also down double digits for the year. When volumes in key debt markets are falling, it is a pretty good guess that asset prices will soon follow.

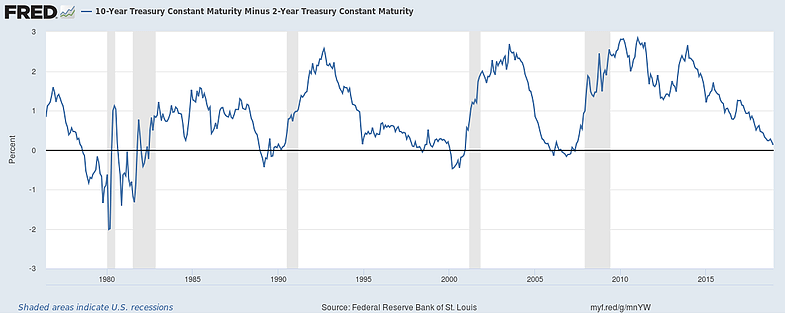

And even as markets recoil from risks real and imagined, the benchmark 10-year Treasury bond continues to rally, forcing the yield curve to invert. There are endless swarms of experts pontificating on the meaning or not of a flat yield curve, but the obvious observation is that buying pressure on the 10-year bond remains brisk. Indeed, do observe that 2s and 10s have been rallying since early November.

Last time the the yield curve inverted was 2005, then as now a period with loan volumes falling and asset prices about to follow. Two years later, asset prices collapsed and banks were subject to liquidity runs regardless of the level of capital. When asset prices fall to cents on the dollar, "we were all broke for a while" as one colleague at Tudor observed a decade ago.

But don't bother policy makers with facts.

Witness Federal Reserve Governor Lael Brainard, who thinks that banks ought to raise more equity capital now that profits are booming and the economy is relatively stable. Sounds great, yes? But sadly Governor Brainard repeats the same nonsense about increased capital that is found too often in the world of academia. Many policy makers see punitive levels of capital as a panacea for addressing market risk. Also, many economists believe that banks should not be profitable at all and instead should simply be managed as public utilities, thus profitability is seen as a secondary concern.

The only trouble with higher capital is that it makes banks less stable. Raising capital above the level needed to 1) absorb actual credit losses and 2) grow deposits reduces bank profits, thereby weakening the banks ability to fund credit losses. Provisions for credit losses come from income, not capital. Banks with weaker revenue and profits trade at lower equity multiples, increasing the cost of debt and equity capital. Eventually poor profitability leads to situations like Deutsche Bank (DB).

Even as markets show signs of entering a new deflationary cycle, current and former Fed officials roam the financial landscape, talking about increased regulation and capital to solve problems of market risk that the Fed itself created with its extraordinary policies. But static piles of capital sitting safely invested in Treasury bills do not help a bank absorb losses. Big spreads and profits are what make banks like JPMorgan (JPM), U.S. Bancorp (USB) and BB&T (BBT) so stable and so highly valued by investors.

Chair Yellen, for example, keeps talking during her numerous public appearances about "holes" in the financial regulatory system, but the biggest holes are intellectual, in the minds of federal regulators who don't seem to appreciate that capital is only important to dead banks and their creditors. In fact, banks like community lenders that manage credit well should be allowed to maintain less capital than their peers.

Chair Yellen and Governor Brainard may eventually admit that extraordinary monetary policy increases market volatility, but the corollary to that obvious statement is more ominous. No amount of bank capital can protect financial institutions during periods of investor fear and market panic. If the US central bank is going to use the manipulation of asset prices to conduct monetary policy, then they should expect to see periods of extreme market volatility as a result. And no amount of book equity capital can save you when the bid goes to zero.

EDITOR'S NOTE

Christopher Whalen is Chairman of Whalen Global Advisors LLC. He has worked in politics, at the Federal Reserve Bank of New York and as an investment banker for more than 30 years. He is the author of three books Inflated (2010), Financial Stability (2014) and Ford Men (2017).

In 2017, he resumed publication of The Institutional Risk Analyst and contributes to many other publications and media outlets. He recently launched the first volume of The IRA Bank Book, a review of the operating and credit performance of the US banking industry written for institutional investors.