The carnage in Emerging Markets caught a lot of investors off guard. Meanwhile, U.S. equities continue to head higher.

Hedgeye CEO Keith McCullough hosted a free edition of The Macro Show this week to discuss our outlook for global growth and the investing implications.

Below are key takeaways transcribed from the webcast. Also below is the video replay to watch the entire 33-minute webcast.

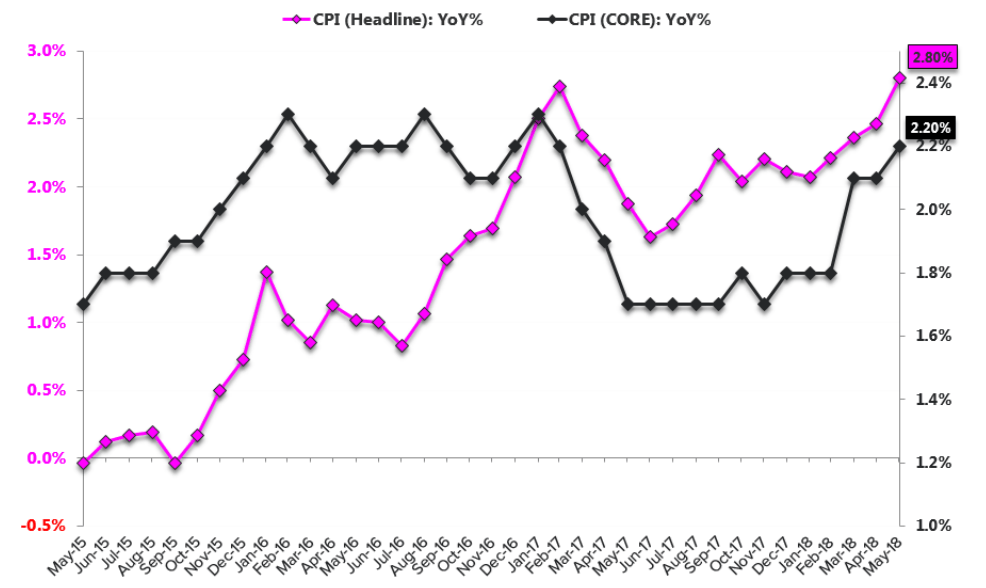

Keith McCullough: The question this morning is: Have interest rates peaked? The Producer Price Index, released this morning, hit a new high. It’s got a 3-handle on it or 3.1%. The CPI hit 2.8%, a 75-month high. They’re both at the highs. In the coming months – there are probably two months left of inflation peaking, that’s our call – bond yields are going to have to reflect on whether inflation accelerating is already priced-in.

Everybody in the mainstream media is staring at inflation accelerating this morning and saying, ‘I guess the Fed is going to have to revise their forecasts.’

Guess what?

The Fed operates on a lag to economic data that is reported on a lag and the fine folks at Hedgeye front-run them by 6-12 months.

This is the point. This inflation data is yesterday’s news.

This is why 10-year bond yields went from 2-3%. This is why the 10-year Treasury is probably signaling a lower high here. According to my quantitative risk ranges, we don’t have a lot of upside beyond 3.02% on the 10-year yield and the high this year was about 3.12%.

So again, has Mr. Market priced-in higher inflation for the last 9-months? Guess what? The market front runs Mr. Consensus all of the time. So be careful. All of Wall Street is short of bonds. Just look at the CFTC futures and options positioning report. Wall Street is net short of ~250,000 10-year Treasury contracts. That’s massive. So everybody is leaning one way and getting long of inflation.

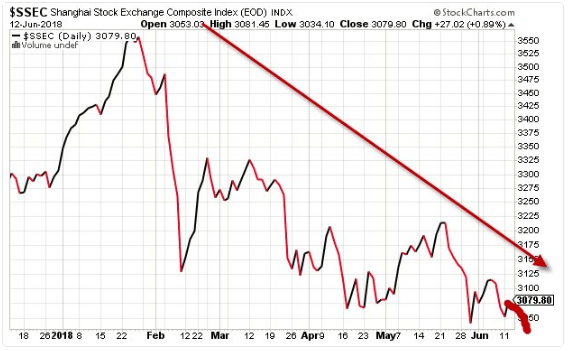

Keith McCullough: Emerging Markets are another big problem.

What if you’re long of China in your asset allocation pie chart? That’s not good. China was down a full percent and hit a new low this morning. The Shanghai Comp is down -15% from its year-to-date highs.

Looking at Emerging Market Asia, we’re not just talking about Turkey, which is of course crashing again this morning. The stock market there is down -22% from where it was in January. Back then, people on Old Wall TV were telling you to buy Emerging Markets. Just terrible.

We said get out of Emerging Markets in January.

The Philippines, another Emerging Market Asian country, was down -2.1% yesterday and -14% from its recent highs.

Poland, that’s another part of the EM pie chart, because it’s Emerging Markets Europe. Polish stocks are down -4% in the last month, -13% from their 2018 highs and leading the losers in Europe.

You’re seeing Europe trade in these risk-on, risk-off type moves. Look at European bond yields. They’re all going down. German, French, Swiss, and Japanese bond yields are all bearish trend. That’s because the bond market does not believe you’re going to get inflation going up in Europe and Japan going forward.

That’s another part of our call on rates potentially peaking. Even if you did Macro across asset classes but looked at the U.S. alone, you’d still be caught because you’re looking at everyone fearful of inflation that’s already been reported at 75-month highs.

Those inflation accelerating exposures have been working going all the way back to September. And then on the other side you’d be ignoring everything that’s going on in Europe, Latin American and Asian interest rates.

Our process looks at market globally. We’re looking at all of the environmental factors, fractally, and having the humility to know that Mr. Market knows a lot more than anybody on Old Wall TV.

Keith McCullough: Looking at the U.S., the S&P 500 does not look like the Russell 2000 and the Nasdaq, which both made all-time high closing highs the other day, because the S&P 500 isn’t the Russell or the Nasdaq. The S&P 500 has international baggage, Emerging Market baggage, China slowing baggage, and European and Polish baggage.

Guess what?

40% of S&P 500 earnings are international and impacted by a strong dollar. Did I mention that we went bullish on the dollar in April?

The current S&P 500 risk range is 2732 to 2809. The top-end of the range is signaling a lower high. So what do you do? At the top end of the range you sell some of your favorite longs and at the low end you buy your favorite longs.

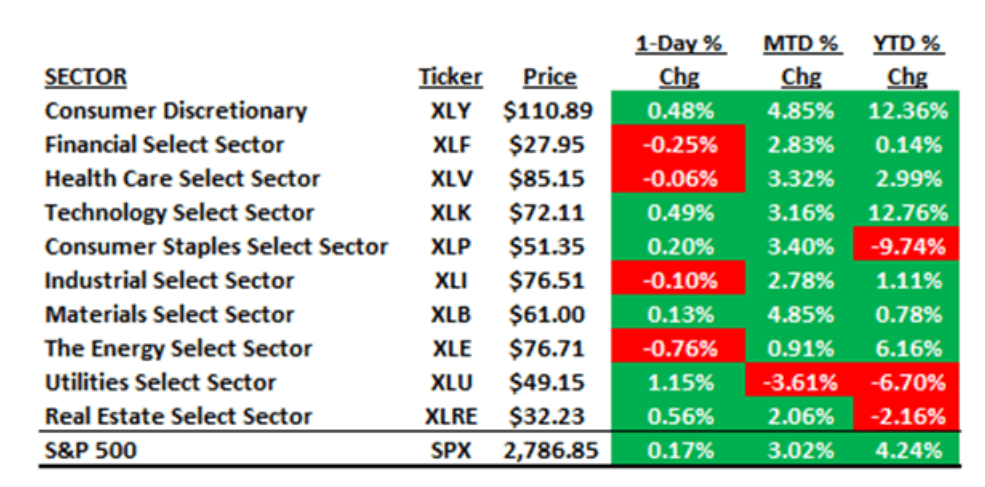

Our favorite longs right now are Energy (XLE), Consumer Discretionary (XLY) and Technology (XLK). The returns of those sectors are awesome. Those sectors are up 6.2%, 12.4% and 12.8% respectively for the year.

We’ve been bullish on Energy because inflation has been heading higher. We’ve been bullish on Consumer Discretionary and Tech because these are the sectors most tethered to the U.S. consumer and an acceleration in the U.S. economy.

Meanwhile, our three favorite shorts have been Utilities (XLU), Consumer Staples (XLP) and Industrials (XLI), which are down -6.7%, -9.7% and up just +1.1% respectively.

Why have we been bearish on Utilities and Consumer Staples?

As we’ve discussed, Utilities and Consumer Staples are bond proxies and with inflation heading higher we’ve been on the right side of that. Why are we bearish on Industrials? Because we’re bearish on China, Europe and Emerging Markets. Those are global industrials. We’re bearish on global growth relative to U.S. growth.

The pundits on TV have had this market all wrong. I really like this quote from Ray Dalio in his book Principles, “Don’t confuse what you wish were true with what is really true.”

There are a lot of different ways to play what’s actually happening in the world versus what people politically and ideally would like to see happen.