The guest commentary below was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst.

This week The IRA will be at the MBA Secondary Market Conference & Expo, as always held at the Marriott Marquis in Times Square. The 8th floor reception and bar is where folks generally hang out. Attendees should not miss the panel on mortgage servicing rights at 3:00 PM Monday. We’ll give our impressions of this important conference in the next edition of The Institutional Risk Analyst.

Three takeaways from our meetings last week in Paris: First, we heard Banque de France Governor Villeroy de Galhau confirm that the European Central Bank intends to continue reinvesting its portfolio of securities indefinitely. This means continued low interest rates in Europe and, significantly, increasing monetary policy divergence between the EU and the US.

Second and following from the first point, the banking system in Europe remains extremely fragile, this despite happy talk from various bankers we met during the trip. The fact of sustained quantitative easing by the ECB, however, is a tacit admission that the state must continue to tax savings in order to transfer value to debtors such as banks. Overall, the ECB clearly does not believe that economic growth has reached sufficiently robust levels such that extraordinary policy steps should end.

Italian banks, for example, admit to bad loans equal to 14.5 percent of total loans. Double that number to capture the economic reality under so-called international accounting rules. Italian banks have packaged and securitized non-performing loans (NPLs) to sell them to investors, supported by Italian government guarantees on senior tranches. These NPL deals are said to be popular with foreign hedge funds, yet this explicit state bailout of the banks illustrates the core fiscal problem facing Italy.

And third, the fact of agreement between the opposition parties in Italy means that the days of the Eurozone as we know it today may be numbered. The accord between the Five Star Movement (M5S) and the far-right League Party (Lega) of Silvio Berlusconi marks a deterioration in the commitment to fiscal discipline in Europe. Specifically, the M5S/Lega coalition wants EU assent to increased spending and cutting taxes – an explicit embrace of the Trumpian economic model operating in the US.

The M5S/Lega coalition is essentially asking (or rather blackmailing) the EU into waiving the community’s fiscal rules as a concession to keep Italy in the Union. The M5S/Lega coalition manifesto, entitled appropriately “Government for Change,” suggests plans have been made for Italy to leave the single currency, calls for sanctions against Russia to be scrapped and reveals plans to ask the European Central Bank to forgive all of the Italian debt the ECB purchased as part of QE.

John Dizard, writing in the Financial Times on Friday, notes the new spending in Italy will be funded via “mini-BoTs,” referring to Italian T-bills. The M5S/Lega coalition apparently wishes to issue small (euro) denomination, non-interest-bearing Treasury bills. The paper would be in the form of bearer securities that would be secured by Italian state tax revenues.

Dizard notes that the logical conclusion of the Italian scheme, which allows the printing of a de facto fiat currency in the form of bearer bonds, will result in either Germany or Italy leaving the EU.

The Italian evolution suggests that Ben Bernanke, Mario Draghi and their counterparts in Japan, by embracing mass purchases of securities via Quantitative Easing, have opened Pandora’s Box when it comes to sovereign debt forgiveness. We especially like the fact that mini-BOTs will be in physical form, printed like lottery tickets. The spread on Italy is now trading 1.65 percent over German Bunds vs 1.5 percent last week and is likely to widen further.

Among the biggest challenges facing Italy’s new government and all EU heads of state is the growing economic policy divergence between the US and Europe. Again, to repeat point two above, the Europeans have no intention of raising interest rates anytime soon and, to this end, will continue to reinvest returns of principal from the ECB’s securities portfolio.

Given the Fed’s focus on raising interest rates in 2018, it seems reasonable to assume that the euro is headed lower vs the dollar. The assumption on the Federal Open Market Committee, of course, is that US inflation is near 2 percent, giving us a real interest rate measured against LIBOR at 3 percent, for example, of one hundred basis points.

But what if the FOMC is wrong about inflation and, particularly, if the favorite inflation measure used by American economists is overstated? Is the broadly defined personal consumption expenditure (PCE) index, which the FOMC relies upon for assessing economic conditions and fiscal policy, inflation, and employment, really the best measure of price change? And is the FOMC currently making a rather gigantic mistake in raising interest rates further?

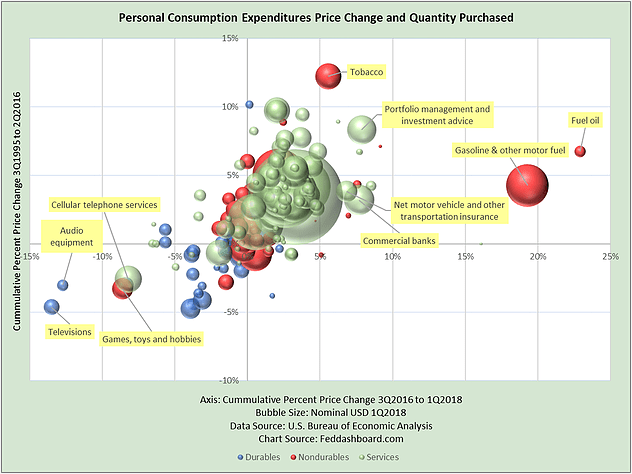

Our friend Brian Barnier at Fed Dashboard has done some interesting work on this question over the past several years, including his May 10, 2018 missive (“Concentrated price changes mean less control for the Fed”). The chart below from Fed Dashboard shows the components of PCE.

The chart illustrates how difficult it is to discern a central tendency in the bundle of data that goes into inflation indicators such as PCE. As Barnier writes:

|

"’Inflation is back’ has been a big headline. Is that true? Yes, if ‘inflation’ means the weighted-average price change of products No, if ‘inflation’ means price increases caused by monetary factors or widespread price increases.” |

The San Francisco Fed has also done some great work on this issue of "PCE diffusion." If you are indeed a data dependent monetary agency, the idea of using the center point average of the diverse factors in PCE as a bellwether for monetary inflation is a bit odd. Notice, for example, that increases in the cost of financial services such as banks, auto insurance and financial advice are among the biggest positive factors in the PCE index. Increases in interest paid on excess reserves (IOER) by the Fed also positively impacts PCE, Barnier tells The IRA.

Important for Europe, the Fed’s use of PCE is leading to rising interest rates, which in turn is driving up dollar borrowing costs in Europe, as shown in the FRED chart below of three month LIBOR vs three month Treasury bills. The FOMC’s view of inflation also is supporting a rally in the much battered dollar. But what if the Fed’s favorite indicator, namely PCE, is overstating the actual rate of price change?

Economists on both sides of the Atlantic like to neatly separate “real-world” indicators like interest rates and debt from supposed monetary factors such as PCE. But the divergence of monetary policy in the US and Europe suggests this is difficult in practice.

There seems to be a basic conflict in how inflation is perceived in Washington and Brussels. This conflict of visions promises to be increasingly problematic in the weeks and months ahead with a stronger dollar and higher US interest rates pressuring emerging nations. The big risk we see both for Europe is that the narrative being followed by the FOMC assumes that inflation is rising, at least as measured by PCE, when in fact deflation driven by excessive debt may still be the central tendency of aggregate price change. If PCE is overstating monetary price change, then the FOMC should not raise rates further.

So the good news is that Europe is showing some signs of life in terms of economic growth. A weaker euro may help in the near term. The bad news is that the EU’s banks remain largely crippled by non-performing loans accumulated during previous economic slumps. And the level of debt held by nations such as Italy is growing steadily. With the UK already headed for the door, the latest political developments in Italy may presage the end of the EU as it stands today. How the Germans and other euro nations deal with the new government in Italy will tell the tale.

EDITOR'S NOTE

This Hedgeye Guest Contributor piece was written by Christopher Whalen, author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington. This piece does not necessarily reflect the opinion of Hedgeye.