“A flush beats a full house”

-Plumbing humor

Plumbum is Latin for lead.

In innovating the first attempts at modern conventional plumbing, the Romans used lead to make pipes and conduits for distributing and delivering water.

Etymologically, the Latin origin persisted through old French into English and continues on its modern derivative forms of “plumbing” and “plumber” today.

So what, right?

- Black Panther, bro! …. Everyone loves Origin stories. And the sales numbers usually come with at least 9 zero’s at the end.

- From a macro perspective, base effects represent the central plumbing of any second derivative-centric model.

Back to the Global Macro Grind ….

I want to make a couple simple points this morning.

Simple, we’d lightly remind you, is not a synonym for insignificant.

After all, yesterday we suggested, simply, that if Powell either explicitly or unwittingly sponsored an expectation for 4+ rate hikes, it risked re-overturning the equity apple cart.

Well, as it turns out, he tacitly sponsored just such a view, sending both yields and the dollar higher.

And because inverse correlations to the dollar remain strong and pervasive and because too high/too fast in rates remains an acute concern to equities, stocks had their worst day since the thralls of the vol contagion selloff on February 8th. And because higher rates and a strong dollar generally put pressure on things priced in those dollars, oil and commodities had a bad day. And … we’re almost done with the global macro cross-walk here … because higher rates, a stronger dollar and commodity deflation are virtually never a positive factor cocktail for emerging markets broadly, EM was similarly under pressure.

Plumbum is Latin for lead. Pablum is the Latin root for “to feed” and, in its modern English form, refers to the expression of worthless, empty ideas. Pablum and cleverly guised double-talk remain the sangre vital of effective, modern Central Banker communique.

Powell is English for Fed Chair … he’ll get some more pablum perfection reps today in the Senate hearing.

Anyway, this morning I wanted to redux an institutional note we put out in mid-January.

To quickly review and set the stage:

We’ve spared no digital ink in detailing the dynamics surrounding domestic growth accelerating over the past year and a half.

Organic and globally harmonized acceleration combined with trough industrial/profit recession comps conspired to drive perhaps the finest protracted stretch of growth and risk adjusted returns of the cycle.

But macro, of course, remains an exercise in successfully front-running Better/Worse and, from a slope-of-the-growth-line perspective, organic improvement and base effects aren’t mutually exclusive.

Large-scale accelerations and all-time highs eventually become the comp and as good as those highs looked against recessionary compares can be as challenging as they become after those trough comps are fully rearview.

From here, after fully traversing those trough comps over the last 6 quarters, the fundamental gravity embedded in the base effects is set to get significantly stronger.

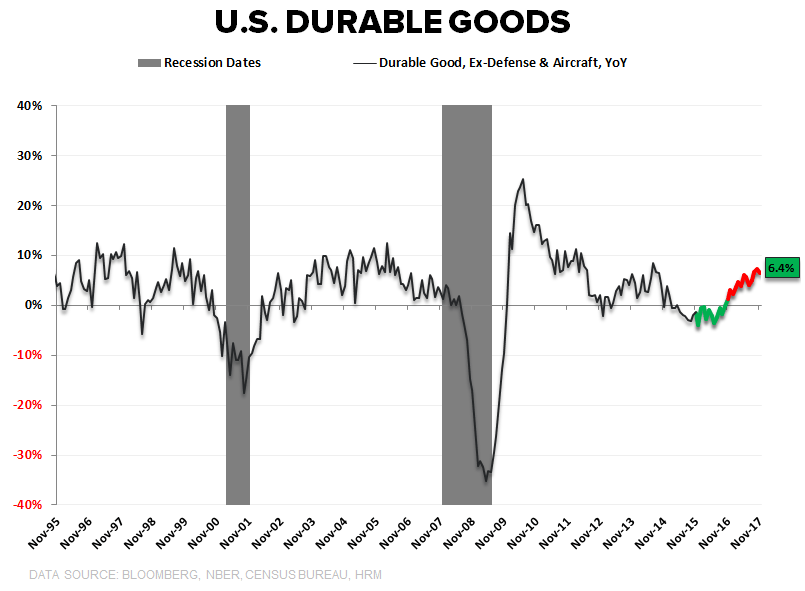

To illustrate, below we visually highlight the forward comp dynamics across a short selection of high frequency domestic fundamentals.

Green Line in the Chart = TTM/2017 Comps

Red Line in the Chart = the NTM/2018 comp setup.

I wanted to re-highlight the base effect dynamics for a couple reasons:

- It’s not our call that growth is at risk of imminent collapse. We’re simply and proactively highlighting the impending 2nd derivative reality - a reality that may be increasingly relevant to asset prices if domestic growth accelerating does, indeed, peak in 1H18.

- We got a sample of this dynamic in yesterday’s Durable and Capital Goods data for January.

The Data:

- Headline Durable Goods = -3.7% M/M and decelerating -440bps to +6.8% Y/Y

- Durables Ex-Defense and Aircraft (i.e. the closest proxy for stuff actual households purchase) = -1.0% M/M and decelerating -200bps to +6.1% Y/Y

- Capital Goods Orders = -0.2% M/M and decelerating -170bps to 6.3% Y/Y

The Detail:

Six percent year-over-year growth is obviously still strong, the New Orders/Capex Plans series in the ISM and Fed Regional Survey’s suggest near-term activity should remain solid and tax reform/infrastructure related capex should remain an upside wild-card. Moreover, extreme weather conditions in the early part of the month may have served as a moderate negative distortion. Further, there is some evidence of a pull forward in demand for short-cycle capital goods ahead of tax reform and a lower tax shield. The rise in Tractor and Rail Car deliveries in late 4Q, for example, are suggestive of such a pull-forward phenomenon – a dynamic that would have, on the margin, helped juice 4Q17 Orders data and drag on the 1Q18 figures.

The Distillation:

One month does not a trend make and mid-high single-digit growth is still good, but it’s less good when filtered through the Better/Worse lens and comps get progressively tougher from here across the Industrial economy.

As we highlighted in the note referenced above, there’s nothing conceptually groundbreaking in visually cataloguing reported reality, but degree of difficulty doesn’t necessarily count and simply identifying gravity doesn’t indemnify one from its effects if you’re not also proactively prepared for it.

After all, the post-crisis market reality remains one where everything is obvious and nothing is what it seems ....

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND views in brackets) are now:

UST 10yr Yield 2.79-2.94% (bullish)

SPX 2 (bullish)

RUT 1 (bearish)

NASDAQ 7024-7422 (bullish)

Biotech (IBB) 106-112 (bullish)

Energy (XLE) 66.51-70.09 (bearish)

RMZ 1014-1061 (bearish)

Nikkei 21170-22484 (bearish)

DAX 124 (bearish)

VIX 14.80-22.94 (bullish)

USD 88.53-90.66 (bearish)

EUR/USD 1.22-1.25 (bullish)

YEN 105.80-108.43 (bullish)

GBP/USD 1.38-1.41 (bullish)

Oil (WTI) 59.70-64.45 (bullish)

Nat Gas 2.50-2.80 (bearish)

Gold 1 (bullish)

Copper 3.12-3.27 (neutral)

AAPL 166.80-180.43 (bullish)

AMZN 1 (bullish)

FB 173-186 (bullish)

GOOGL 1059-1150 (bullish)

NFLX 265-300 (bullish)

TSLA 318-363 (neutral)

Christian B. Drake

U.S. Macro Analyst