This guest commentary was written by Mike O'Rourke of JonesTrading.

The Federal Reserve’s “temporary,” highly accommodative policy that commenced just under a decade ago has now outlasted the two Federal Chairs who were its key architects. For context, during the Greenspan era, the Fed Funds rate averaged 4.8% as compared to 1.5% under Chair Bernanke and 0.5% under Chair Yellen. During Greenspan’s final decade as Chair, the Fed’s balance sheet averaged $760 Billion compared to $2.25 Trillion under Bernanke and $4.4 Trillion under Chair Yellen. The best of luck to incoming Fed Chair Jay Powell who is rising to the helm right when the normalization process becomes challenging. Inflation and Unemployment have been at or near their respective targets for a year or more. Global monetary policy has kept US Treasury yields artificially low as the US enters a period where it needs to accelerate issuances.

Former Chair Greenspan could not have been more accurate in describing the environment on Bloomberg Television today when he said,

|

“There are two bubbles: We have a stock market bubble, and we have a bond market bubble. At the end of the day, the bond market bubble will eventually be the critical issue, but for the short term it’s not too bad. But we’re working, obviously, toward a major increase in long-term interest rates, and that has a very important impact, as you know, on the whole structure of the economy.” |

The first chart below illustrates the level of the 10Yr Treasury yields on key dates since the Bernanke era commenced in 2006. For the past 5 years, the market mantra has been that stocks are inexpensive compared to bonds. That relative value comparison to instruments that have spent most of the past decade manipulated by and pushed to bubble extremes by central banks has created the third most expensive equity market of the past century.

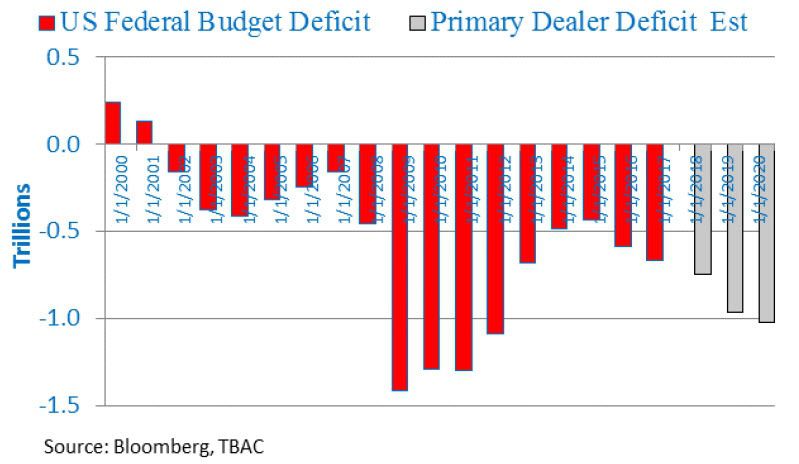

The budget deficit is expected to be $750 Billion this year and approximately $1 Trillion next year (chart below). As a result, it was expected that when Treasury announced its refunding plans today, it would increase the size of its offerings. Interestingly, Treasury increased the size of 2 and 3 year offerings more than expected. One would think that with the 2Yr yield at 2.14% and the 3Yr yield at 2.28%, the smart funding move would be to sell 10Yr at 2.7% and 30Yrs at 2.93%. Treasury either knows the market can absorb enough of either or it is truly scared of financing at those higher rates. Treasury is expected to increase issuance by approximately $1 Trillion per year for the next 3 years (chart below). Unlike the QE environment, Treasury will not have the luxury of having the Fed absorb most of the net issuance.

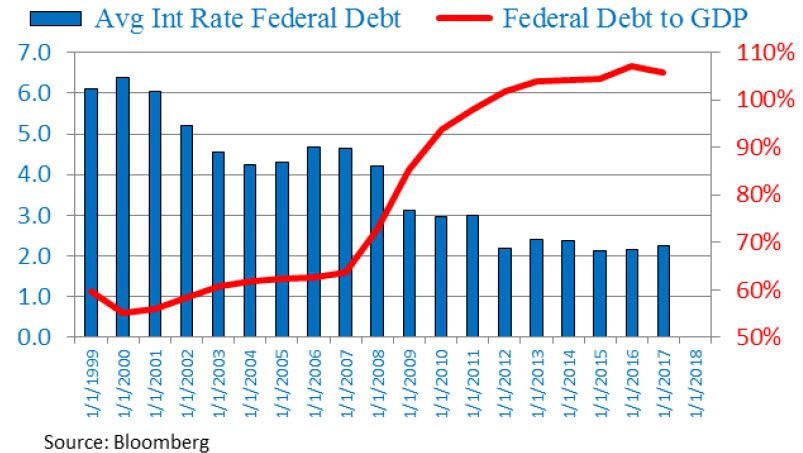

Going into the crisis in 2008, Federal Debt to GDP was 65% and interest rates were peaking and set to decline. Today, Federal Debt is 106% of GDP and interest rates have troughed and are rising. The Dollar weakness may be the first manifestation of the deterioration of the nation’s balance sheet. Regardless, it should be clear that the rising rates trade is a structural change in the environment. The central bank orchestrated bond market bubble is set to burst. Stocks may remain inexpensive relative to bonds, but bonds are getting less expensive with each passing day and are likely to continue doing so.

EDITOR'S NOTE

This is a Hedgeye Guest Contributor research note written by Mike O'Rourke, Chief Market Strategist of JonesTrading, where he advises institutional investors on market developments. He publishes "The Closing Print" on a daily basis in which his primary focus is identifying short term catalysts that drive daily trading activity while addressing how they fit into the “big picture.” This piece does not necessarily reflect the opinion of Hedgeye.