This guest commentary was written by Jeffrey Snider from Alhambra Investment Partners.

I thought he might wait awhile longer given how things have played out. I guess not. Bill Gross, the former “bond king” at PIMCO, was back to advertising his position that the great bond bull market of the past quarter century is finished. In a tweet from his new employer Janus (h/t ZeroHedge) it seems there is no level for long UST yields he can’t hate. This time, it’s the 10-year crossing the 2.50% threshold for the sixth time since Reflation #3 started in the second half of 2016.

There has sprung up a cottage industry standing at the ready to shout BOND ROUT!!! at each and every uptick in longer dated UST yields. The godfather of that business has been Bill Gross, consistently, which is not a good start as far as credibility might be concerned.

In May 2015, during the “transitory” rise in UST yields in between Phase 1 and Phase 2 of the “rising dollar”, Gross was again everywhere with the same message:

|

"The bull market “supercycle” for stocks and bonds is approaching an end, as the unconventional monetary policies that have bolstered asset prices since the financial crisis are running out, widely followed investor Bill Gross said on Monday. |

That came almost exactly two years after one of his most widely followed proclamations (May 2013), one that for a few months anyway appeared to have some small chance of actually coming true (Reflation #2).

|

"Bill Gross said the three-decade bull run in bonds ended last week when the 10-year Treasury yield hit 1.67%, in his latest attempt to call the top in a market whose buoyancy has been aided by central-bank policy and long questioned by skeptical investors. |

As early as February 2011, Mr. Gross had emptied PIMCO’s Total Return fund of all its US government debt holdings in seeing global economic recovery. At that time he had claimed the impending end of QE2 (June 2011) would be a “d-day” for the bond market (by which he meant hugely negative for bond prices, thus rising yields). The mechanics are correct, meaning actual growth would be bad for bonds, forgetting that recovery was left in the hands of people like Ben Bernanke (he of the “global savings glut” ridiculousness).

PIMCO’s bond king was by no means alone in his views. In fact, he was reflecting each and every time the consensus view, at least the one fashioned by Economists. In March 2012, the University of Pennsylvania wrote a mere six months before QE3 (which was undertaken because the bond market of persistently lower rates was correct that the economy wasn’t, in fact, recovering, even indicating the very reason it wasn’t) of the steady mainstream chorus striking notes against Treasuries:

|

"Many experts are warning that bonds — and bond funds — are riskier than they have been in recent decades. The risk can be reduced by owning bonds and funds with shorter maturities, since those holdings would suffer less from rising rates: Even if rates were to double or triple overnight, a $1,000 bond maturing the next day would still be worth $1,000, while a bond that wouldn’t mature for 10, 20 or 30 years would collapse in value. |

And we shouldn’t forget Nassim Taleb’s “no-brainer” trade from a couple years earlier. In talking about selling UST’s short, the chaos theory proponent for some reason opted for the utterly conventional, telling his audience at a February 2010 conference in Moscow “every single human should have that trade.”

What’s been going on all this time is incredibly simple, which is why it doesn’t make sense for anything other than human biases and ideology. Each one of these predictions accompanied a selloff in UST markets, in some cases a bonafide BOND ROUT!!! if still short of the epic proportions given to it by contemporary commentary.

We are conditioned to believe that economic growth is a given. It just happens, so when it doesn’t happen we are given the only option of believing it’s just temporarily delayed from returning to our lives. Because of that bias, what that means in terms of the UST market is that at some point interest rates will have nowhere to go but up. They crashed as a result of the economic collapse that took place in 2008-09, so once the economy gets back on track they will have no choice but to get back normal in anticipation of the economy’s rush toward it.

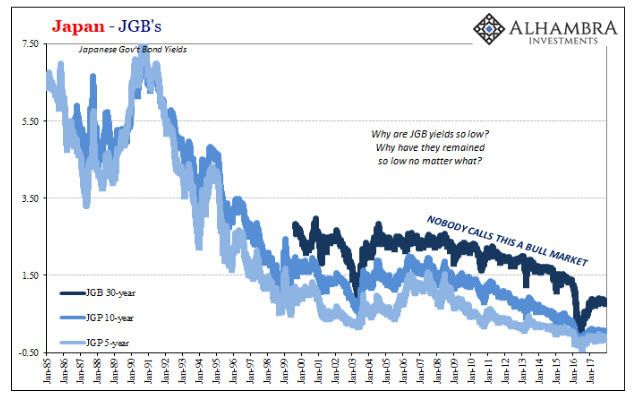

The only place (in our recalled modern experience) where that didn’t happen, the prominent counterexample if you will, was in Japan. Interest rates sunk in the early and middle nineties in the lingering, persisting aftermath of what were described as almost conventional asset bubbles (conventional in the 21st century sense where they have seemingly prevailed everywhere). Thus, three decades of constantly low interest rates assaults our baseline economic sensibilities – such that “we” purposefully ignore the Japanese specimen, preferring instead to chalk it up to strictly Japanese factors that could never be repeated here (or anywhere else in the world).

And yet, our own economic experience has been marked by these same fits and starts; one step forward and then always two steps back (if not three at times). It’s not like it’s been just a few months without vigorous expansion, either, the clock striking a decade in the middle of last year. It’s more than enough time to consider the what is supposed to be impossible is not only possible but even the baseline or most likely case – that economic growth is not a given, and that returning to normal financial levels and conditions nowhere near a certainty.

Japan’s been at it for three decades and counting, an end predicted to its high-priced bond market at each and every turn, too (though no one seems to want to characterize JGB’s as in a bull market for some reason).

Having surpassed the ten-year mark for own economic unhappiness, given that longstanding bias toward normalcy it almost seems as if it has to happen right now. The longer we go without higher rates anticipating better if not completely normal growth, the more these many “experts” believe it has to happen tomorrow.

So, each little bond selloff over the past few years has been treated as the definitive signal for the normalcy, the one you better not bet against for each of these oracles are sure is our guaranteed futured; even as the (many) years tick by without being paid up on that pledge.

Markets just don’t ever go in a straight line, nor are they perfectly efficient (even the UST market fell susceptible to IRHNTGBU fever three times in the last ten years, though each one with decreasing intensity of belief). That means in the short run, however you wish to define the short run, interest rates are going to rise relative to yesterday, last week, or even several months ago. It’s just the way things are.

What has happened in each of these cases listed above, as well as the innumerable others no one could ever fully catalog, is that regular market gyrations have been given emotional significance through nothing more than disbelief, a sort of voodoo economicsbefitting this 21st century update. That’s true even though after a decade the burden of proof long ago shifted to those who claim something has meaningfully changed so as to lift the veil of malaise that disappoints the world economy time and time again.

If your entire premise for believing that interest rates have nowhere to go but up is that they just have to at some point, that’s really no basis at all. There is nothing in the world that says economies only grow, and a great many historical examples that show that has never been a certainty. Japan is just the latest, or was the latest before the whole global economy blindly followed the Western central bankers who blindly followed the Bank of Japan into the (so far) inescapable abyss.

EDITOR'S NOTE

This is a Hedgeye Guest Contributor piece written by Jeffrey Snider of Alhambra Investment Partners. Prior to joining Alhamra Investment Partners as Head of Global Investment Research, Snider was at Atlantic Capital Management. This piece does not necessarily reflect the opinion of Hedgeye.