This guest commentary was written by Mike O'Rourke of JonesTrading. Click here to get Hedgeye's Market Brief, a free weekly newsletter featuring the top 5 trending insights on Hedgeye.com.

As of the close of trading yesterday, Apple Inc. had posted returns of 39.66% year to date and the shares were approximately 3% from their all-time high that was registered last month. The run-up throughout the year occurred in anticipation of the new iPhone launches.

The iPhone 8 started selling in late September and debuted to negative reviews. Shares dipped briefly before rallying nearly 8% in the past month. Last week, AT&T warned that the company experienced 900,000 fewer smartphone upgrades than it did in Q3 2016, an ominous sign. Earlier this week, there were reports that the iPhone 7 was outselling the iPhone 8. It was also reported that “Consumer Reports thinks the 18-month-old Galaxy S7 is a better phone than either new iPhone 8 model.” Amidst these latest developments, this week Apple shares continued to push to their highest levels in a month. Market hopes shifted towards the iPhone X due out early next month.

Last night, Taiwan’s Economic Daily News reported that Apple reduced iPhone 8 and 8 Plus orders by 50% for the next two months. That was the report that finally resonated with Apple shareholders sending the shares 2.4% lower today. We have said it numerous times, this is a tape where “price sets the narrative” and as long as Apple’s share prices did not respond to the news, investors had no interest in doing so either.

Stock market complacency is a daily topic and this type of behavior is another example of it. If the market is only reacting to price action, then this is the most virtuous part of the virtuous-vicious cycle. The largest daily change over the past 5 trading days is 18 basis points. Four of the 5 largest S&P 500 companies traded down today. It was merely a blip in the market as funds simply rotated elsewhere. We have reached such an extreme point where there are no dips left to buy.

In 2017, S&P 500 pullbacks from 52 week highs have nearly evaporated (chart below). On an annual basis, the pullback from a 52 week high has averaged -1.34% (chart above). That is the second shallowest annual average on record, second only to the -1.67% average in 1995. The long term average S&P 500 pullback form a 52 week high is -8.42%.

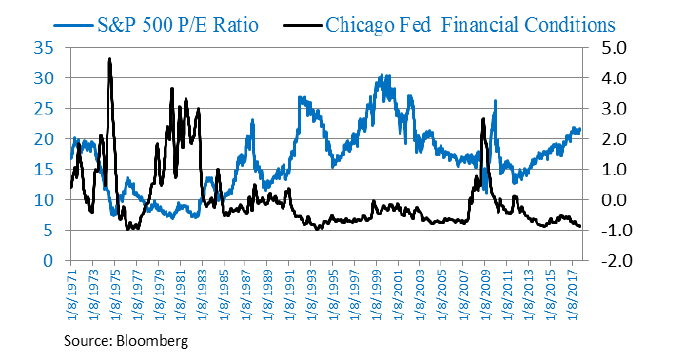

When one looks at the market's low volatility, expensive asset valuation levels and extremely easy financial conditions, it is trifecta of unfavorable investment variables (chart below). The market's inability to even register the slightest correction continues to draw investors in at high prices. Being the cusp of a credit crisis or in an even more extreme asset bubble are likely the only other macro environments where market variables line up less favorably for long term investors than they do today.

EDITOR'S NOTE

This is a Hedgeye Guest Contributor research note written by Mike O'Rourke, Chief Market Strategist of JonesTrading, where he advises institutional investors on market developments. He publishes "The Closing Print" on a daily basis in which his primary focus is identifying short term catalysts that drive daily trading activity while addressing how they fit into the “big picture.” This piece does not necessarily reflect the opinion of Hedgeye.