This special guest commentary was written by our friend Richard Peterson M.D., MarketPsych.

|

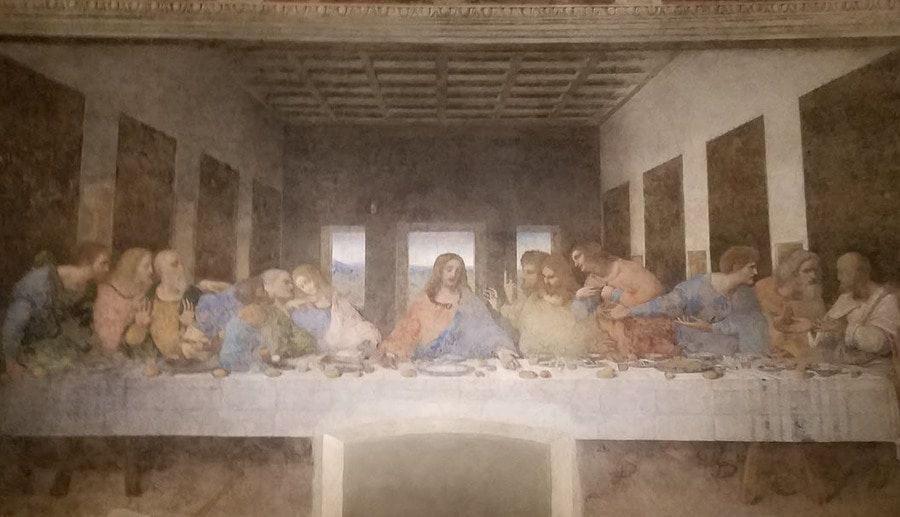

"One of you shall betray me." |

A wave of emotion passed through the disciples - shock, confusion, sadness, fear.

This moment is captured in Leonardo da Vinci's masterpiece, "The Last Supper." Da Vinci portrays the disciples' reactions as ripples radiating outwards. These waves are seen in the two clusters of three disciples on each side of Jesus in the image below.

Prior to the Last Supper, paintings were often portraits of emotionless dignitaries, bland landscapes, religious iconography, or historical battle scenes. Classical sculptures displayed subdued or passive emotion. Da Vinci put dynamic feeling and emotion - life and humanity - into this work.

As in the painting, at times waves of emotion wash over society. It is such waves of emotion that we model and study at MarketPsych. We often forget while absorbed in the details of earnings, prices, IPOs, the next new thing - financial markets are a human construction. In order to better understand them, we must understand our shared humanity with all its quirks.

Today's newsletter examines how waves of social sentiment course through equity markets. We demonstrate how such waves appear to precede market price swings and describe how they are used by an award-winning and exceptionally large equity fund manager (NN IP). Today's newsletter also touches on the path-breaking work of Prof Richard Thaler, winner of this year's Nobel in Economics - and specifically the "house money effect" - which we use to better understand market turning points.

IFTA 2017

|

Human subtlety...will never devise an invention more beautiful, more simple or more direct than does nature, because in her inventions nothing is lacking, and nothing is superfluous. |

I was fortunate to attend the IFTA (International Technical Analysis Association) conference in Milan last weekend. Bob Prechter spoke about the influence of social mood at major turning point in markets. At market bottoms media reports rationalize the end of opportunity (he provided several examples from gold, oil, and equities). At tops, the media proclaims the rally will go on forever. As our own Dr. Frank Murtha noted in a tweet this week: "Flocks of swallows returning to Capistrano is the harbinger of spring. Flocks of daytrading commericals is the harbinger of big, big trouble".

It is not only practitioners who appreciate the influence of complex human emotions on markets. The work of pioneering academics who elucidate the psychological patterns in market prices is finally being accepted. Robert Shiller split the Nobel prize in 2013 for his work on bubbles, and last week Richard Thaler was awarded the Nobel for his work in behavioral economics.

Thaler Nobel

|

I have been impressed with the urgency of doing. Knowing is not enough; we must apply. Being willing is not enough; we must do. |

Prof Richard Thaler performed ground-breaking research on individual biases such as the endowment effect and the house money effect. Thaler also examined markets, and in research with Werner DeBondt they identified one of the first "behavioral" patterns in markets called the "long-term reversals" anomaly in their 1985 paper "Does the Stock Market Overreact?" For example, after 3 to 5 years of out-performance, stocks tend to experience a subsequent 3 to 5 year period of underperformance. The reverse is also true (underperformers then outperform).

Thaler is a co-founder of Fuller and Thaler Asset Management (a mutual fund group) that takes advantage of behavioral biases in market price patterns. He also worked to help individuals make better financial decisions by designing the "SMART" plan in collaboration with Shlomo Benartzi. The SMART plan is a scheme to improve retirement savings rates by changing choice architecture. Their work is estimated by MarketWatch as adding $29.6 billion to American's retirement savings accounts. Thaler's books "Nudge" and "Misbehavior" are enjoyable reading and provide an overview of his work.

The market price anomalies identified by Thaler aren't definitively linked to social mood (although "overreaction" in the title of his paper is certainly suggestive). In looking for evidence of collective investor under and overreaction in prices, there is a fairly interesting media sentiment pattern that suggests it is occurring. Thaler's work sheds light on one aspect of this price pattern.

Sentiment Cycles in Markets

|

First, never underestimate the power of inertia. Second, that power can be harnessed. |

A popular image depicts a sine wave of market emotions. Prices start low with prevalent doubt, rise on optimism, climax on euphoria, fall on concern, decline on panic, and the cycle starts again. It's a simplification, but most investors can relate to it (hence its popularity). Yet it's difficult to use such a model for timing buys and sells. Important information is lost in the simplification. However, by integrating an understanding market complexity, some asset managers successfully use social sentiment in their investment process.

NN Investment Partners, which manages over $230 billion, scales in or out of equity exposure depending on social risk perceptions. Of the factors they consider, social sentiment holds the greatest weight. And it works - their funds won Lipper and Morningstar performance awards each of the past three years. I took a (unfortunately grainy) photo of NN's CIO Valentijn van Nieuwenhuijzen presenting on their investment process last weekend in Milan, below.

In several past newsletters we've described the sentiment cycle in the S&P 500. We included quotes from NN about their exploitation of the cycle.

The Sentiment Cycle in Pictures

|

Rip Van Winkle would be the ideal stock market investor: Rip could invest in the market before his nap and when he woke up 20 years later, he'd be happy. He would have been asleep through all the ups and downs in between. But few investors resemble Mr. Van Winkle. The more often an investor counts his money - or looks at the value of his mutual funds in the newspaper - the lower his risk tolerance. |

It is difficult to use sentiment in investing precisely because - as humans - we become caught up in the waves. Too often we are unconsciously influenced by the stories and beliefs of the herd, adopting them as our own.

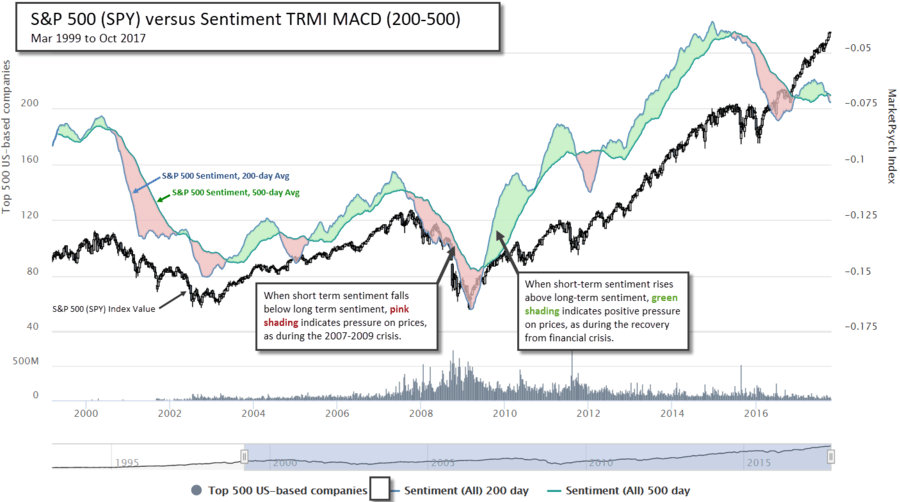

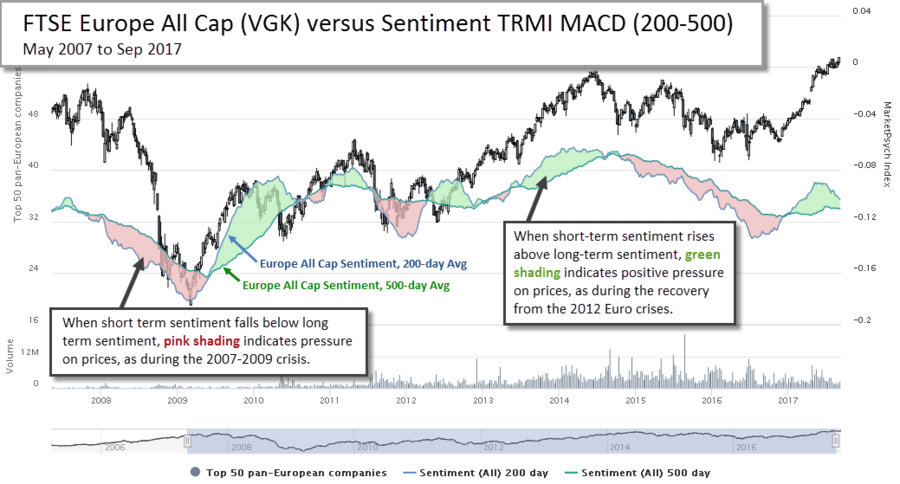

We can see a rough representation of the sentiment cycle using media sentiment averages. These seem to precede S&P 500 price movements since 1998. Below we can see that when the shorter term moving average of sentiment (200 days) is greater than the longer term moving average (500 days), the market tends to rise. Those periods of more positive recent media are colored with green shading below. When the 200 day average is more negative, the market tends to follow to the downside (pink shading).

The chart shows that a long-term moving average of media sentiment has historically been broadly useful in predicting the ups and downs of public equity markets. In particular, it seems to do well in timing tops. On average, a Long-Short investor would outperform a Buy-and-Hold investor by 3x using the moving averages of sentiment to time long and short bets. The media sentiment tone is perhaps reflecting or perhaps driving (or perhaps both) overall investment risk taking.

There are several potential explanations for this cycle. We've described previously how the confirmation bias may prevent investors from selling despite the warning signs at the top of a bull market. But that is not the whole story. Another bias - Richard Thaler and Eric Johnson's house money effect - also provides insight into the cognitive biases that may contribute to the cycle.

The House Money Effect

|

[W]e find that under some circumstances a prior gain can increase subjects' willingness to accept gambles. This finding is labeled the house money effect. |

When people experience a sudden windfall - earning or receiving more wealth than they had expected - Richard Thaler and Eric Johnson found that they subsequently increase their risk taking. He called this bias the house money effect because it is similar to gambler behavior at casinos. Having won money, most gamblers will increase their risk taking. It is said that they feel they are "playing with the house's money."

Increasing risky behavior after a gain seems to contradict the "cutting winners short" bias, which is derived from Kahneman and Tversky's prospect theory. Investors cannot both take more risk and cut risk in the "domain of gains", so one of these must be wrong.

The reason for this seeming contradiction is the mobility of the reference point in prospect theory. When people receive a windfall, especially if through their investments, they quickly learn to do more of the rewarded behavior. They feel compelled to take more risk in order to catch up with where they "should be" (the reference point). The reference point is moved higher as the media reports on "Bitcoin millionaires" and startup moguls who make it look easy. As long as investors are experiencing fear of missing out (FOMO), then they are in the realm of losses and will continue to take excessive risk via the house money effect.

However, after a long bull market, sometimes the market corrects, and investors lose a sizable portion of their highly-leveraged net worth. At these moments, their reference point shifts lower, and they begin to imagine they may lose their gains. They suddenly shift into the domain of gains ("at least I still have some profits") and are more susceptible to cutting winners short - taking their profits. As they do so, prices are driven lower. A self-reinforcing cycle of losses may be triggered as self-preservation becomes the goal.

Note that the sentiment MACDs depicted in this newsletter are better at timing market tops. As the media tone shifts to the negative, the gradual resetting of the reference point lower may be the cause of this superior performance.

Fundamental human behavior is consistent across cultures. Consistent with that observation, this pattern is in evidence globally.

Global Sentiment Cycles

|

It had long since come to my attention that people of accomplishment rarely sat back and let things happen to them. They went out and happened to things. |

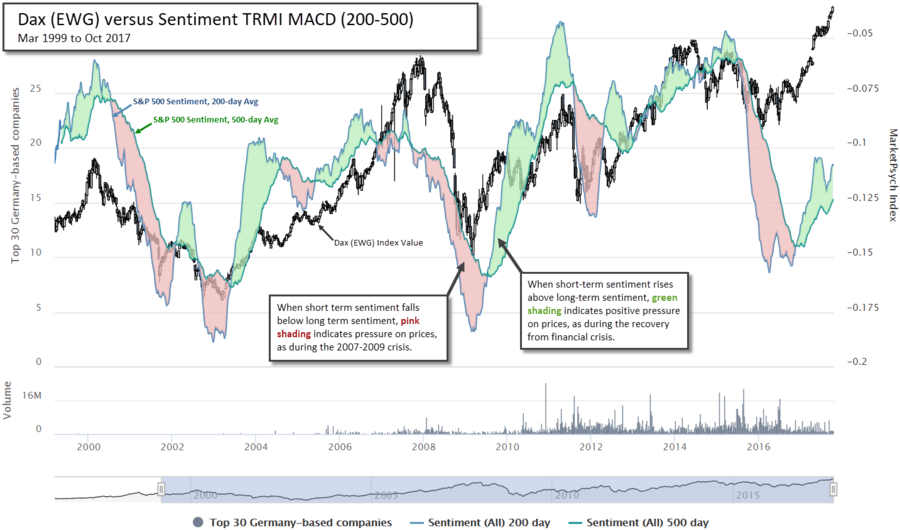

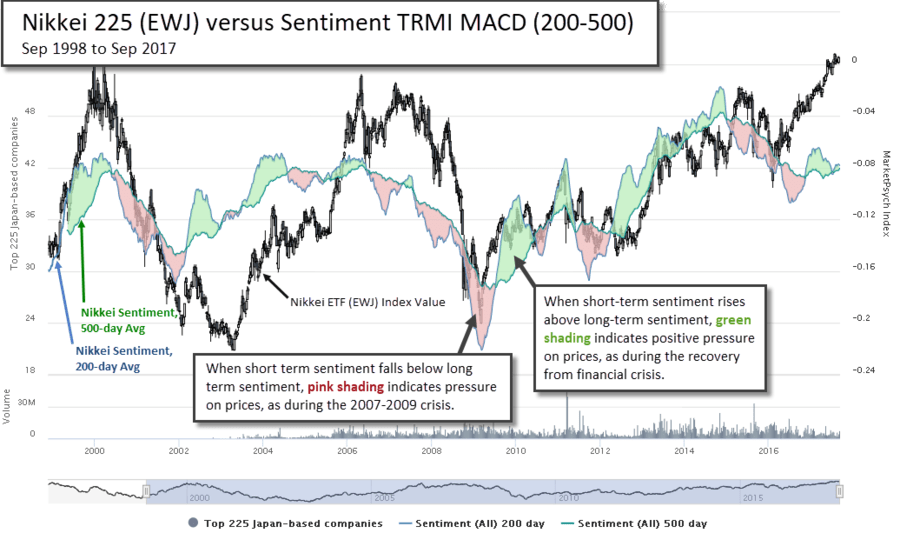

The cycle that we see in the S&P 500 is present, and profitable, in developed markets globally. Images of the remarkable predictive nature of this pattern are visible for the largest below through early September 2017: the Dax, the Nikkei, the HangSeng, and the EuroStoxx.

Most developing markets respond to media sentiment more quickly than developed markets, and the 200 vs 500 day MACD appears too slow in the Bovespa and the China Composite (and probably others - we haven't checked). Perhaps these markets are driven more by short term speculators than long-term investors or slow-moving institutions, and so the volatility is more violent. Consistent with that observation, the 30-90 MACD of sentiment seems to work best in China and Brazil.

By the nature of their construction, MACDs force around 50% long and short positions over any given time period. Note that our look back period is ideal for this type of study, with many stock markets making only modest gains since 1998. If we have a prolonged bull market, as we did from 1982 - 1999, then a buy-and-hold strategy would win out over a sentiment MACD.

Housekeeping and Closing

|

"As a well-spent day brings happy sleep, so a life well spent brings happy death." |

When times are good, our reference point (expectations) rise, and we become susceptible to the house money effect. It is difficult to conceive of worsening conditions at such times. And we ought to be most on alert precisely when everyone else is complacent.

Many cultures and religious traditions find that an appreciation of death improves our perspective on life. I took the below picture in Milan at the sanctuary San Bernardino alle Ossa. Something to contemplate when the climate is bullish.

Those are bones of the dead from the 15th and 16th centuries. When we consider our impermanence, our daily decisions take on more significance.

Our Thomson Reuters MarketPsych Indices are deployed globally to monitor real-time market psychology and macroeconomic trends. If you're an academic interested in data for research, please reach out for access. If you represent an institution, please contact us. The commercial Thomson Reuters MarketPsych Indices dataset covers 45 currencies (including Bitcoin), 61 countries' fixed income products and stock indexes, 12,000+ companies and stocks, 36 commodities, and 187 countries.

Happy Investing!

Richard Peterson and the MarketPsych Team

EDITOR'S NOTE

This is a Hedgeye Guest Contributor piece written by Dr. Richard Peterson. Peterson is CEO of the MarketPsych group of companies where he leads MarketPsych's data and asset management division. He has trained thousands of professionals globally to leverage behavioral insights. He is a board-certified psychiatrist and author of Trading on Sentiment.This piece does not necessarily reflect the opinion of Hedgeye.