The guest commentary below was written by Dr. Daniel Thornton of D.L. Thornton Economics.

My first three essays on the limits of monetary policy dealt with mainstream views about how monetary policy works to stabilize prices and promote economic growth and full employment. I had three main conclusions:

- Interest rates are relatively unimportant for spending and hence for increasing output and employment.

- Monetary policy actions have little effect on the interest rates that matter most for spending decisions.

- Monetary policy cannot have a persistent or permanent effect on economic growth.

This essay deals with unconventional policies that the FOMC undertook in the wake of the financial crisis and some that have been suggested by policymakers but not implemented. I will end the essay with a discussion of what I believe monetary policy can do and what Congress should do to prevent the FOMC from trying to do things it can’t really do.

The Great Financial Crisis: What The Fed Did

Following Lehman Bros. bankruptcy on September 15th, the FOMC attempted to stimulate growth by attempting to reduce long-term interest rates. It did this by adopting QE, forward guidance, and the maturity extension, aka Operation Twist. I have examined the theoretical foundations of these programs elsewhere, so I will only briefly summarize my conclusions.

Using the verbatim transcripts of the FOMC meetings, I have shown that “theoretical foundations” for QE were developed after the program began. Bernanke claimed that QE worked through what he called a portfolio balance effect. Bernanke’s portfolio balance effect (which is different from an effect of the same name discussed by Milton Friedman and others) requires the markets for the long-term securities that Fed purchased—mortgaged-back securities, long-term Treasuries, and agency debt (markets #1) to be segmented from (that is, independent of) other long-term securities markets (markets #2). However, in order for the Fed’s purchases to effect on other long-term rates, it also requires investors markets #1 to sell these securities and purchase long-term securities in markets #2 because those markets are now paying a higher interest rate. Of course, this means these markets cannot be segmented—catch 22.

There is an alternative way QE could work. Specifically, all “long-term securities markets” could be segmented from “short-term securities markets.” But this is ridiculous! Decades of finance research has shown a strong association between long-term and short-term rates. (as I note below, the tight association between long-term and short-term rates is essential for the effectiveness of the FOMC’s forward guidance policy). It is not surprising that during a CNBC interview Bernanke Jan. 2014 quipped “The problem with QE is it works in practice but it doesn’t work in theory.”

However, there is no credible evidence that it worked in practice either. I have shown that much of the research Bernanke cited as evidence of QE’s effectiveness is either extraordinarily weak (An Assessment of the Event-Study Evidence) or due to a combination of faulty data and bad statistical analysis (Is There a Portfolio Balance Effect?).

Bernanke and others suggested that even if QE didn’t work through the portfolio balance effect, it could reduced long-term Treasury yields by reducing the term or risk premium on long-term bonds (the term premium is the extra yield that long-term investors require to be compensated for holding long-term assets because they have more market risk (aka, interest rate risk) than short-term rates). I have shown that this cannot happen because the term premium is solely determined by two things, neither of which is affected by the quantity of the long-term security in the market.

Moreover, if investors have a strong preference for holding long-term securities, as one of the ways that QE is supposed to work requires, the premium that investors would require to hold long-term bond would be small. If the preference was strong enough, the term premium could be tiny. I show that the only way that QE could reduce the term premium on long-term Treasuries is if the most risk averse investors leave the security of the default-risk-free Treasury market while the least risk-averse investors remain. Bernanke and others have suggested that this could be how QE reduces the term premium. However, this seems implausible. Why would the most risk-averse investors leave the security of Treasuries?

In any event, there is no evidence that QE reduced term premiums. The FOMC’s forward guidance policy is the brainchild of Michael Woodford, who suggested that changes in the short-term policy rate would have a larger effect long-term interest rates if policymakers could creditably commit to keeping the policy rate at the new level longer than investors would normally expect. Woodford’s forward guidance idea requires that long-term rates are determined by market participant’s expectations for short-term rates. Hence, the market for long-term securities cannot be segmented from the market for short-term securities, as Bernanke’s portfolio balance effect requires. In fact, forward guidance requires there be perfect substitutability between short-term and longer-term rates.

The only thing that drives a wedge between longer-term and shorter-term rates is the term premium, which is due to the fact that longer-term rates have more interest rate risk than shorter-term rates. I noted in An Opportunity for Greater Transparency, 2010, the FOMC should have told the market exactly why it was trying to reduce long-term interest rates using QE and forward guidance because the policies are based on economic theories that are completely incompatible. Of course, the FOMC never took up my suggestion.

In any event, the FOMC’s experimentation with forward guidance was relatively short-lived. The Fed began using forward guidance in December 2008 when it reduced its target for the funds rate to zero saying “the Committee anticipates that weak economic conditions are likely to warrant exceptionally low levels of the federal funds rate for some time.” The wording was subsequently changed to give a specific calendar date, with the date being pushed back on several occasions. The wording was changed at the December 2012 meeting to make raising the funds rate target conditional on the unemployment rate reaching 6.5%.

In early 2013 (Is the Unemployment Rate Threshold a Good Idea?), I pointed out several reasons why tying the FOMC’s interest rate policy to the unemployment rate was a bad idea. Consequently, I was not surprised when the FOMC abandon forward guidance at its March 2014 meeting because the unemployment rate was approaching the critical level much faster than expected. Of course, the decision to abandon forward guidance may have been influenced by lack of evidence of the effectiveness of forward guidance policy (see Efficacy of Forward Guidance and Central Bank Forward Guidance). However, the lack of evidence that QE was effective did not cause the FOMC to abandon that policy. Maturity extension was also tried but quickly abandoned.

'There is no compelling evidence the Fed Controls INFLATION'

“If interest rates aren’t important for spending and the Fed has only a minor effect on the interest rates that matter for spending, and if monetary policy has at best a small effect on spending, output, or employment, and no permanent effect on output growth, what can the Fed do?"

This is a good question. I would love to say the Fed can control inflation! However, as I pointed on in my first essay (Interest Rates Don’t Matter), while there is widespread agreement that Volcker’s November 6, 1979, change in policy brought an end to the Great Inflation of the 1970s and early 1980s, there is no agreement exactly how this happened. As I noted in The Link Between Monetary Policy and Inflation, the problem is that economists and policymakers have two theories of inflation, neither of which works in practice. The Fed’s inability to affect inflation is illustrated by the fact that the FOMC has pursued a very aggressive monetary policy in part to raise the inflation rate to its 2% target level, but inflation has remained below 2% for nearly a decade.

There is no compelling evidence that the Fed can control inflation. We will have to wait until the next bulge inflation for more evidence one way or the other. However, I do believe that the Fed’s actions immediately following Lehman’s September 15, 2008, bankruptcy announcement brought an end to the recession and returned output to trend growth. I have written about this in detail (What the Fed Did and What It Should Have Done) so I will briefly summarize the arguments and the evidence.

The financial crisis is dated as beginning on August 9, 2007, when BNP Paribus suspended redemption of three of its investment funds. Initially, the Fed did little. However, by year’s end, the Fed had established several new lending programs and the federal funds rate target was reduced from 5.25% to 4.25%. Nevertheless, the recession began in December 2007 and there was further deterioration of financial markets. The FOMC responded by reduced its funds rate target aggressively—to 2% on April 30. Fed increased its lending to banks and helped rescue Bear Sterns.

“This must have helped.” It didn’t.

The further deterioration in financial markets (see the Financial Crisis Timeline) culminated with the bankruptcy of Lehman Bros on September 15. After that, both the recession and the financial crisis intensified. “Why didn’t the reductions in the funds rate and the Fed’s lending help?” The answer to the first part of the question is provided by my first three essays. The answer to the second part of the question is the Fed’s lending didn’t help because it was sterilized. That is, the Fed offset the effect of all of its pre-September 15, 2008, lending on the total supply of funds available in the credit market by selling an equal amount of government securities— this is what sterilization means. Consequently, the Fed’s lending did not increase the amount of credit available to the market.

“This seems like a bad idea. The problem was a scarcity of credit because banks and others were afraid to lend because it was too risky?”

Correct on both counts. As I document in Requiem for QE pp. 3-6, the Fed did this because the FOMC was implementing policy by controlling the funds rate. (I say the Fed rather than the FOMC because as I document in Requiem for QE p.3, the decision to sterilize the lending was made by Bernanke and not the FOMC.) Had the lending not been sterilized, the Fed would not have been able to control the funds rate.

“So what did the Fed do differently after September 15, 2008?”

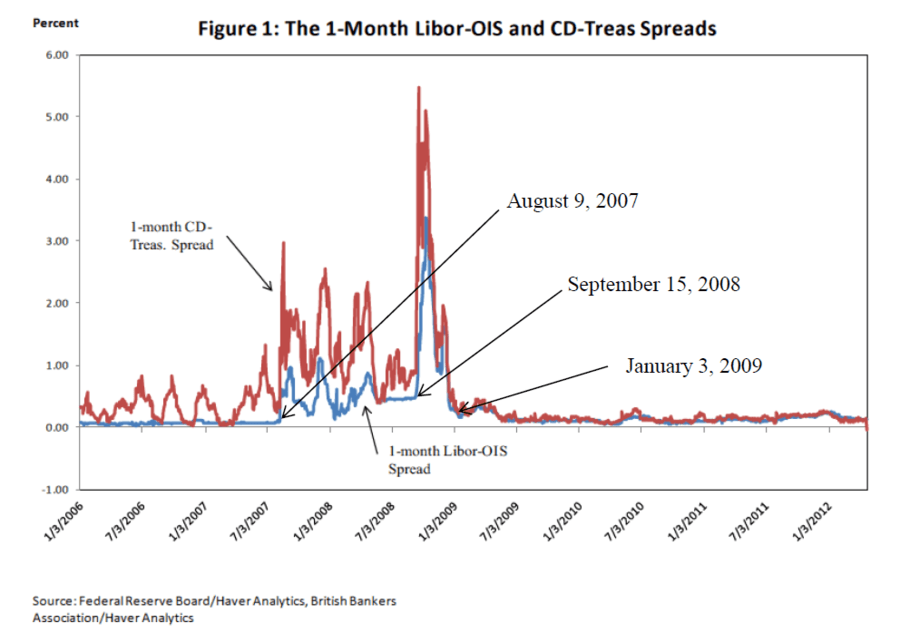

It stopped sterilizing its lending. Hence, there was a large increase the amount of credit available to banks and other financial institutions: The supply of credit increased by nearly $1 trillion by January 2009. The effect of this change in policy was dramatic. Spreads between higher risk and lower risk securities, that had increased significantly after August 9, 2007, and exploded immediately after Lehman’s announcement had declined very significantly by early January 2009. Some spreads were below their pre-Lehman levels.

For example, the figure below shows the spread between the 1-month rate on negotiable certificates of deposit (the main source of funds for bank lending before Lehman) and the 1-month Treasury bill rate (red) and the spread between the 1-month Libor rate and overnight indexed swap (OIS) rate (see What the Libor-OIS Spread Says for an explanation of the IOS rate) daily from January 3, 2006 to January 30, 2012. The figure shows that the CDTreas. spread had been trending higher before August 9, 2007, while the Libor-OIS spread remained flat.

However, both spreads increased significantly after August 9, 2007, and remained high in spite of the 3.25% reducing in the federal funds rate and the Fed’s sterilized lending. Both rates increased dramatically immediately upon Lehman’s announcement. The Fed increased its lending, but this time it was not sterilized. The increase in the total supply of credit accompanied the Fed’s unsterilized lending provided the market with the credit at this critical time.

The effect of this change was dramatic. By January 3, 2009, both spreads were below their pre-financial-crisis levels. That the policy of unsterilized lending was effective is also evidenced by the fact that the recession ended June 2009, just 9 months after Lehman’s bankruptcy—the largest bankruptcy filing in U.S. history. In contrast, the recession began in December 2007 and got progressively worse over the next 9 months in spite of the Fed’s sterilized lending and 3.25% reduction in the federal funds rate. In contrast, the Fed engaged in unsterilized lending and credit spreads declined dramatically in a period of three and a half months and the recession ended just 9 months later. This is remarkable; however, it seems that I’m the only person who has remarked about it. This is truly amazing.

The worrisome thing from the perspective of future monetary policy is policymakers did not have an epiphany; they didn’t suddenly realize they had to massively increase the supply of credit to the market. No, as I have shown (Requiem for QE), the Fed stopped sterilizing its lending because it was no longer able to sterilize. Indeed, policymakers did not even realize how significant this unintended change is policy was or how financial market conditions and the economy improved. This is evidenced by Janet Yellen’s March 18, 2009, statement at the March meeting of the FOMC:

|

"I think we’re in the midst of a very severe recession—it’s unlikely to end anytime soon. The optimal policy simulations would take the fed funds rate to −6 percent if it could, and because it can’t, I think we have to do everything we possibly can to use our other tools to compensate." |

Of course, this is exactly what the FOMC did—QE, forward guidance, operation twist, and a zero federal funds rate target for over 6 years after the recession ended. These policies had essentially no effect for the reasons discussed in my first three essays. Unfortunately, the FOMC continues its low-interest-rate policy and targeting the federal funds rate in the misguided belief that these actions will eventually increase output growth.

The danger is the FOMC may try to do other things—maintain a large balance sheet indefinitely, adopt a negative nominal interest rate policy, targeting stock prices, or god knows what else. This is why it is critical that Congress constrain the FOMC’s monetary policy actions by adopting my economic-reality-based monetary policy (Fixing a Bad System).

EDITOR'S NOTE

This is a Hedgeye Guest Contributor piece written by Dr. Daniel Thornton. During his 33-year career at the St. Louis Fed, Thornton served as vice president and economic advisor. He currently runs D.L. Thornton Economics, an economic research consultancy. This piece does not necessarily reflect the opinion of Hedgeye.