“All you need in this life is ignorance and confidence, and then success is sure.”

-Mark Twain

If you read the “news” this morning, the IMF is cutting its US growth forecast, the ECB is going to end QE, and 1 in 3 pets in America are obese. What, of any of that “news”, do you believe?

Well… “the Banfield Pet Hospital 2017 State of Pet Health report found that 1 in 3 pets who visited Banfield pet facilities in 2016 was overweight or obese. Banfield operates over 800 pet clinics in the US, Mexico and the U.K. and the annual report details health habits of the 2.5 million dogs and 500,000 cats who visited facilities across the country in 2016.” –Daily Mollusk

And our predictive tracking algos have the IMF dead wrong at +2.1% US GDP growth (we have it accelerating to +2.69% and +2.99% year-over-year growth in Q417 and Q118). Whoever thinks the ECB is going to “end QE” is just ignorant of Reflation’s Rollover.

Back to the Global Macro Grind…

Yeah, tell me what you really think KM. What I think is that a lot of people who haven’t been Long Real Growth vs. Short Reflation are having performance problems right now and they need to think long and hard about how they’ll be positioned for the 2nd half of 2017.

Who has confidence in our growth outlook? At least 2/3 of the people we met with in New York for the last 2 days weren’t outright disagreeing with our view, if only because the best strategist on Wall Street (Mr. Market) has the same view.

My meetings are obviously a super small sample which could make me as ignorant as the IMF (who cut its growth forecasts at the literal bottom in US bond Yields last year and has missed this entire GDP acceleration). So how about the “confidence” of the masses?

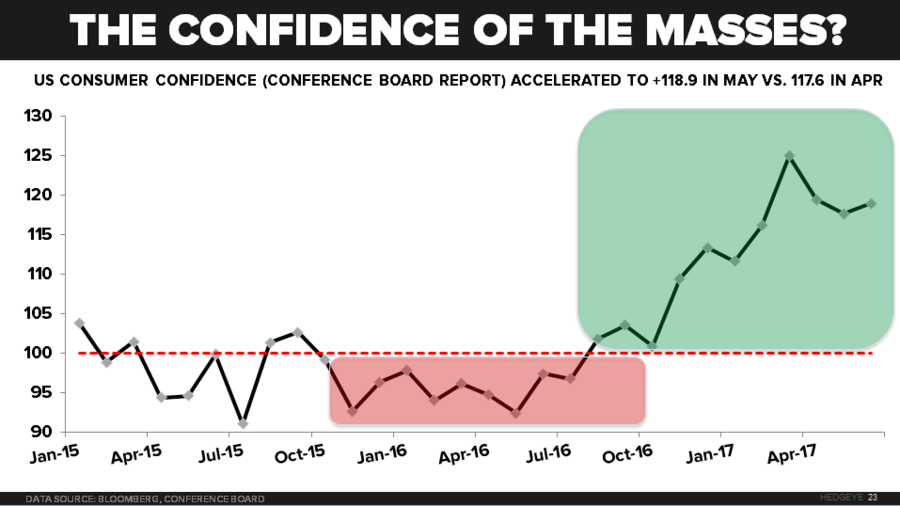

- US Consumer Confidence (Conference Board Report) accelerated to +118.9 in MAY vs. 117.6 in APR

- While that reading is inside of the +124.9 reading in MAR, it’s still higher than any reading under Obama’s Admin

- More importantly, Consumer Confidence was all the way down at 97.4 in JUN of last year

I get it. That’s “soft” data, and 33 month highs in both US Durable Goods and Capex growth is too hard for the bears to digest. That said, that’s what makes a market. Being confident matters a lot less than being ignorant in contextualizing economic data.

As importantly, we don’t want to be ignorant when it comes to making buy and sell decisions:

- On Monday morning, US Equity Beta (SP500) signaled immediate-term overbought (see Real-Time Alerts for timestamps)

- On Monday morning, the VIX signaled immediate-term TRADE oversold (risk range = 9.77-11.42)

- Into yesterday’s close US Equity Beat (SP500) almost signaled immediate-term oversold (risk range = 2)

- EUR/USD is signaling immediate-term TRADE overbought this morning (risk range = $1.10-1.13)

- UST 10yr Yield is signaling immediate-term TRADE overbought this morning (risk range = 2.12-2.26%)

- German 10yr Bund Yield is signaling immediate-term TRADE overbought this a.m. (risk range = 0.23-0.41%)

Instead of telling you how the market makes me “feel” (heck, some of my competitors give you a GDP forecast that “feels like 2%”, but I won’t go there), I feel absolutely nothing when the math in my model delivers me my daily risk range.

We don’t feel anything at all as 30 economic data points per month roll through our predictive tracker for GDP either…

For me, the rates of change in numbers (across duration) are a lot easier to understand than how many pundits theorize about markets. One of the best examples of this right now is the theory that “it’s different this time in Europe.”

We’ll review our #EuropeSlowing call on our Q3 Macro Themes Call on Friday (ping ) if you’d like to participate (we love taking your Q&A!), but isn’t it interesting that Mr. Market might have already made his call?

- European Stocks (EuroStoxx50) are down -0.6% this morning and -1.8% in the last month

- French Stocks (CAC40) are down -0.5% this morning and -1.9% in the last month

- Spanish Stocks (IBEX) are down -0.5% this morning and -2.4% in the last month

For context, inclusive of yesterday’s -0.8% correction, the SP500 is up +0.2% in the last month and the Russell 2000 is +1.5% (Biotech, IBB, is up +7.9% in the last month vs. Energy Stocks, XLE, down -3.7%).

Oh KM, you cherry picker you…

Yep, I left the -2.0% month-over-month decline in the Nasdaq until last just because I think it’s the most interesting debate right now. To buy or not to buy, the FANDAGO?

Truth: -1.8% of the decline came yesterday, so you’re probably trying to figure out if:

A) You want to be long the FANDAGO into month and quarter end and/or

B) You want to be overweight that Real Growth #Accelerating exposure in Q317

Since we’ve told you to buy every damn dip in things like Tech and Biotech (even when it had negative price momentum) back in November of 2016, I’m staying with it, hopefully being patient enough to signal buy at the low-end of my risk ranges.

Since I currently have 0% exposure to any FANDANGO in Real-Time Alerts, here are the risk ranges I’m waiting on:

- FB 149-156

- AMZN

- NFLX 148-159

- Dow Bro 21,276-21,533

- AAPL 142.06-147.90

- NVDA 145-162

- GOOGL 944-990

- ORCL 48.84-53.17

And because I feel absolutely nothing about these tickers (they are simply price/volume/volatility signals with no political or “valuation” bias), both Dow Bro and NVDA are the closest to signaling buy (at the low-end of the range).

As an independent research provider who aspires to get both the research and the “signals” right, there’s some serious ignorance in me signaling BUY on something like NVDA (which we don’t cover yet on the research team).

But, I’m just a knucklehead-and-retired-hockey-player, don’t forget. That said, I have a lot of confidence in my risk management signaling process and ignorance has often been my life’s bliss.

Our immediate-term Global Macro Risk Ranges (intermediate-term TREND views in brackets) are now:

UST 10yr Yield 2.12-2.26% (bearish)

SPX 2 (bullish)

RUT 1 (bullish)

NASDAQ 6121-6294 (bullish)

XOP 29.85-32.13 (bearish)

Nikkei 195 (bullish)

DAX 121 (bullish)

VIX 9.77-11.42 (bearish)

EUR/USD 1.10-1.13 (bearish)

Oil (WTI) 42.01-45.22 (bearish)

Gold 1 (bullish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer