The most over-owned, consensus long position in all of global macro is... the Euro! That's the latest data embedded in the CFTC's latest net futures and options positioning amongst institutional investors. Below are three key considerations on why we think the balance of risks related to the Euro "has decidedly swung in favor of long-term U.S. dollar bulls like us."

(See Z-score in table below, which compares current contract positioning against the mean net contract positioning over the past 1-year and 3-year period.)

1. Euro Positioning

At +71,335 contracts, the futures and options market (i.e. institutional investor consensus positioning) is as net long of euros as it has been at any time since the first week of May 2011. Recall that the EUR/USD spot rate plunged -19% from that overextended peak before bottoming in the Summer of 2012 on ECB President Mario Draghi's pledge to do "whatever it takes" to save the Eurozone.

2. Euro Complacency

Over the past month, the EUR has experienced the largest decline in at-the-money put implied volatility across all of the global macro factor exposures we track. Implied volatility is effectively investor expectations of future volatility as implied by positioning in futures and options contracts.

Put simply, investor expectations of future volatility has fallen precipitously, as formerly fearful investors abandoned bearish bets. Investors had been buying protection to hedge against risks related to a Le Pen victory in France's April/May elections. Marine Le Pen is, of course, President of the far-right National Front political party, who pledged to leave the European Union.

Following centrist Emmanuel Macron's win in May, downside protection has rolled off. That looks misguided. Our call on the Eurozone economy is that it will continue to slow and surprise investors to the downside throughout 2017. As such, we view investors expectations of low future volatility as budding complacency. When compared to historical or realized actual volatility implied volatility is trading at a discount, meaning investors expect volatility to decline still further. Note: This has left the Euro with the 2nd most extended aggregate implied volatility discount in the world.

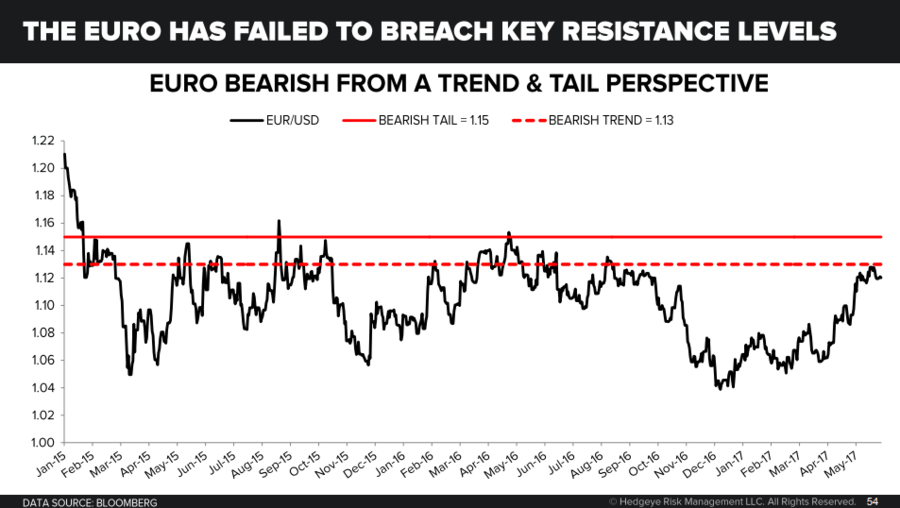

3. Euro vs. U.S. Dollar

Digging in still further, the Euro remains bearish from an intermediate-term TREND and long-term TAIL perspective on Hedgeye CEO Keith McCullough’s proprietary price, volume and volatility overlay. Unless the Euro/U.S. Dollar can breach 1.15, we think the Euro currency remains in a bearish trend.

As Hedgeye Senior Macro analyst Darius Dale writes in today's Early Look, "All told, the expected value calculus has decidedly swung in favor of long-term U.S. dollar bulls like us."