This special guest commentary was written by our friend Stefan Wieler of Goldmoney.

Low volatility is the topic of the day in financial markets. Volatility in U.S. equity markets is flirting with all-time lows despite considerable economic, political, and monetary uncertainty. In this report, we describe gold volatility in relation to other markets in part one, and then discuss the nature and risks of low volatility across assets in part two.

1. GOLD VOLATILITY IN RELATION TO OTHER MARKETS

What is volatility? In finance, volatility describes the degree of variation in the price of an asset. It is typically expressed by the annualized standard deviation (σ) of (log) returns. The standard deviation of a data set is the square root of its variance (σ2). In mathematical terms:

Volatility comes in two basic flavours: historical volatility and implied volatility. Historical volatility is simply the measured (realized) price volatility of a security over a specific time horizon. Implied volatility is the expected volatility that is priced into the options traded on that security.

Options can be valued in many ways. One common approach is to use the Black-Scholes model, a framework in which the value of an option is determined by five parameters:

- The current price of the underlying security

- The options strike price

- Time until expiration

- Risk-free interest rates, and

- The implied volatility

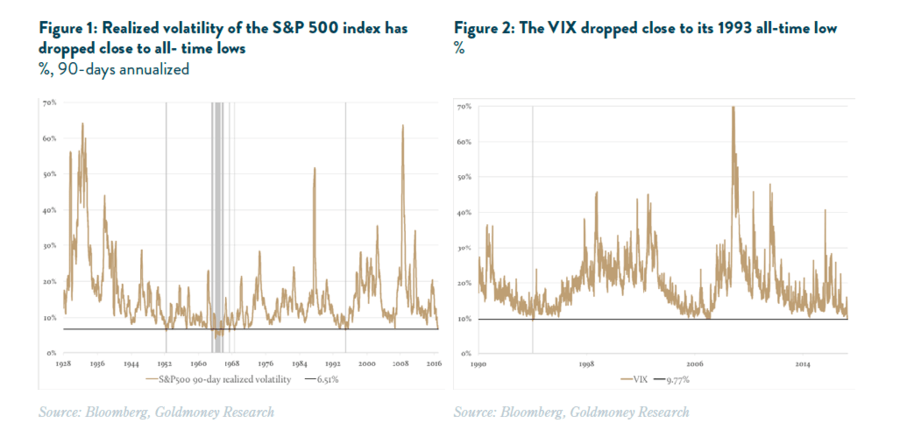

The latter reflects the market’s expectations of what the volatility of an underlying security will be over an option’s lifetime. As the four other parameters can be observed, one can back out the implied volatility of the security from observed option prices. This implied volatility itself can be traded. The famous VIX index (Chicago Board Options Exchange Volatility Index) reflects the 30-day implied volatility in the S&P 500 Index market using a wide range of options on the S&P 500 Index futures.

The VIX is widely regarded as a risk index; a rising VIX reflects market expectation for higher price volatility. Realized volatility in the equity markets had dropped to extremely low levels. For example, the 90-day realized volatility of the S&P 500 index dropped as low as 6.5% at the end of April, a 22-year low. As from three single days in 1995 with lower volatility, one must go back to 1968 to find an environment with lower realized equity volatility (see Figure 1). The VIX shows a similar picture, dropping to 9.77% on May 8, 2017. Aside from a brief three-day period in December 1993, during which the index dropped to 9.31%, the VIX had never been lower (see Figure 2).

Low volatility is not only an equity phenomenon. Volatility in the fixed income space is also very low. The TYVIX (CBOE/CBOT 10-year U.S. Treasury Note Volatility Index), a cousin of the VIX index in the fixed income space, dropped to 4.36% – just shy of the all-time low of 3.62% – more than 2% below the long-term average, and over 10% below the all-time high in 2008.

Commodities have also been languishing in ultra-low volatility for a while now. The 90-day realized volatility of the GSCI commodity index had dropped to an all-time low by mid-2014. Even though the sharp sell-off in oil that started in mid-2014 led to a temporary spike in realized volatility, volatility in the commodity space has been trending sharply lower again over the past 12 months.

Having now reached the gold market, gold price volatility has dropped to very low levels. For example, 90-day realized volatility of XAU/USD prices dropped to the lowest levels in 12 years. Aside from a period in the 1990s, gold volatility has rarely been that low. Over the past 10 years, gold volatility has only been below the recent lows for 0.23% of all trading days (see Table 1).

It’s important to note that this is not due to low volatility in the denominator (USD), but gold itself. Looking at gold priced in other currencies, volatilities have rarely been that low over the past 40-plus years (see Table 1) and are currently well below the long-term average (see Figure 3). For the currencies in which gold price volatility isn’t near all-time lows, the reason lies in the denominator as those currencies go through some turmoil (e.g. Brazilian real, Mexican peso etc.).

Because there is an options market for gold, one can also calculate implied volatility in gold prices. Implied volatility for gold in USD is also extremely low and near dated volatility (1-month) dropped to less than 10 for the first time, at least since the beginning of recorded data (see Figure 4). Implied gold volatility also highlights an important aspect of the current low-volatility phenomenon. Even though implied volatility is low, the volatility curve remains quite steep (see Figure 5). We will discuss how this helps to explain the low volatility environment overall later in our report.

2. THE NATURE AND RISKS OF LOW VOLATILITY ACROSS ASSETS

It seems bizarre that volatility in general – and gold volatility in particular – is so low despite heightened economic, political, and monetary uncertainty, and we believe it isn’t a coincidence that realized and implied volatility are depressed across most asset classes and currencies.

It is our view that central bank policy is at the core of this phenomenon, as central bank market intervention has reached unprecedented levels in the aftermath of the financial crisis. From the late 1980s, the Fed, under chairman Allan Greenspan, had the tendency to lower interest rates every time the economy (and thus markets) hit a bump. Traders and investors became increasingly convinced that for as long as Greenspan remained chairmen of the Fed, the Fed would come to the rescue if markets turn sour. They referred to it as the “Greenspan put”.

While the Greenspan Fed tried to navigate the economy and markets by moving interest rates up and down, central banks now use a much more brachial approach. As most central banks already slashed interest rates to zero years ago (or in some cases below zero), they can’t influence monetary conditions any further by fiddling with key interest rates; instead, they began to directly purchase assets in the hope that it would ease monetary conditions and stimulate their respective economies.

For traders and investors, this once again means that there is always abuyer of last resort if things turned against them. It would be natural to call this the“Yellen put”, but this would be a gross understatement as this time it is not just the Fed that gives traders and investors the reassurance that any sell-off would be promptly responded to with more stimulus. Essentially, all major central banks – from the ECB to the BOJ, BOE, SNB, and the PBC – have been buying vast amounts of assets, from government to corporate bonds, mortgages, and even equities.

The six major central banks alone have together now purchased nearly 20 trillion dollars in assets, which is equivalent to almost 40% of the combined GDP. The market’s conviction that central banks would intervene if markets fall too far has created an environment in which investors see a buying opportunity in every dip. If central banks keep buying assets, a good trading strategy is to buy assets before them and then sell those assets back to them later. There is no other reason to buy a 10-year government bond with negative yield to maturity.

In addition, because of the ultra-low interest rate environment, investors don’t really have anywhere to go. Even if investors come to realize that an asset is overpriced and should be sold, when all assets are overvalued, including – and we would argue especially – currencies themselves, what else is there to buy?

Investors have also been trained like Pavlov dogs to simply sell volatility. Selling volatility has been one of the most successful trading strategies in the past several years. Although it seems odd that investors keep selling volatility when the VIX has dropped to record low levels, implied volatility is still significantly above realized volatility and near-dated volatility is trading below longer-dated volatility; therefore, investors still ending up making money when they sell longer-dated volatility and rolldown the curve.

When investors sell volatility, the dealer (usually a bank) that sells them the volatility becomes long volatility if he remains unhedged. As explained, that has been a losing trade; therefore, dealers will try to hedge their exposure by buying the underlying assets when prices fall and selling them when they rise, as the hedging smooths out assets prices and thus leads to lower volatility. This creates a feedback loop through which investors selling implied volatility leads to lower realized volatility and thus, somewhat like a self-fulfilling prophecy, reinforces the volatility shorter’s conviction that this is the right trade.

Obviously, when volatility suddenly spikes for whatever reason, and traders try to unwind their short volatility position, this works in the other direction as well. Banks stop hedging their positions as being long volatility suddenly pays off, which is why an important player that used to cushion asset price moves will disappear overnight.

Selling volatility is also no longer limited to the domain of hedge funds and professional traders at prop desks, as it has increasingly found its way into the retail space. Sources working in the structured product space at some major banks informed us that products that are inherently short volatility are currently bestsellers in the retail space. These products are not necessarily being bought to gain short volatility exposure; instead, the retail investor is usually trying to get exposure to a trade idea in a more cost-effective way and (perhaps unknowingly) ends up buying products that are short options.

Because realized volatility has been in a prolonged downward trend, products that were structured to be short implied volatility have generally done well over the past years. As a result, these products are becoming ever more popular, though one cannot help but assume that a lot of these retail investors are unaware that these products may move in conjunction with volatility. They might not even know what volatility is.

Neither BREXIT nor the political turmoil that followed the U.S. elections, increased geopolitical tensions, or the Fed’s departure from NIRP had any lasting impact on volatility, both implied and realized. Last week’s media report regarding a memo from former FBI director James Comey that implied president Trump may have interfered with an ongoing FBI investigation seemed to have awoken the VIX from its slumber, but after initially shooting up to 16 on May 18 from less than 10 a week earlier, it dropped back to 12 the next day and was trading at 10.72 at the time of writing.

Shortly after Alan Greenspan became Fed Chairman, U.S. equity markets crashed by more than 10% in one day. It seems that the preceding Fed policy was designed to avoid spooking markets at all costs to avoid a repetition of the 1987 crash. As a result, volatility in the equity markets continuously fell for several years until the mid-1990s. When volatility began to rise again later in the decade on the back of the Asian crisis and turmoil in the wake of the failing LTCM fund, equity markets nevertheless kept on moving higher.

Eventually, the Greenspan put era ended with the burst of the dot com bubble in 2000, which wiped out close to 80% of the NASDAQ’s value and sent the U.S. economy into a recession. It’s naïve to assume that the outcome will be more benign this time around, given the vastly larger scale of central bank intervention.

Low volatility is simply the symptom of a market that is no longer able to react to price signals. Being long volatility can work over the short run to hedge a portfolio if the timing is right. You can view an example of successful timing provided by our guest contributor Omer Rozen (Market Update: Hedge Your Portfolio Now with VIX Futures on the Cheap, April 28, 2017).

On the other hand, the buy and hold volatility strategy as a hedge for potential future market turmoil has been a losing trade. However, we found that elevated volatility (higher levels of the VIX) tend to be followed by rising gold prices. Figure 6 shows the return of the gold price in USD at 12, 26, and 52 week intervals after the VIX hit certain levels, starting with the creation of the VIX in 1990. The higher implied volatility, the stronger gold rallies in the subsequent weeks.

EDITOR'S NOTE

This is a Hedgeye Guest Contributor research note written by Stefan Wieler for Goldmoney Insights. Wieler was previously a senior commodity strategist at Goldman Sachs. This piece does not necessarily reflect the opinion of Hedgeye.