This special guest commentary was written by Peter Atwater of Financial Insyghts.

Economic theory suggests that the supply and demand for goods and services should be inversely related. As price rises, suppliers should offer more of a product while consumers should demand less; and, as price falls, suppliers should offer less while consumers demand more.

Applying this concept to credit, it suggests that as the price of credit falls, lenders should offer less while borrowers should demand more; and as the price of credit rises, lenders should offer more while borrowers demand less. With changes in price, supply and demand should move in opposite directions.

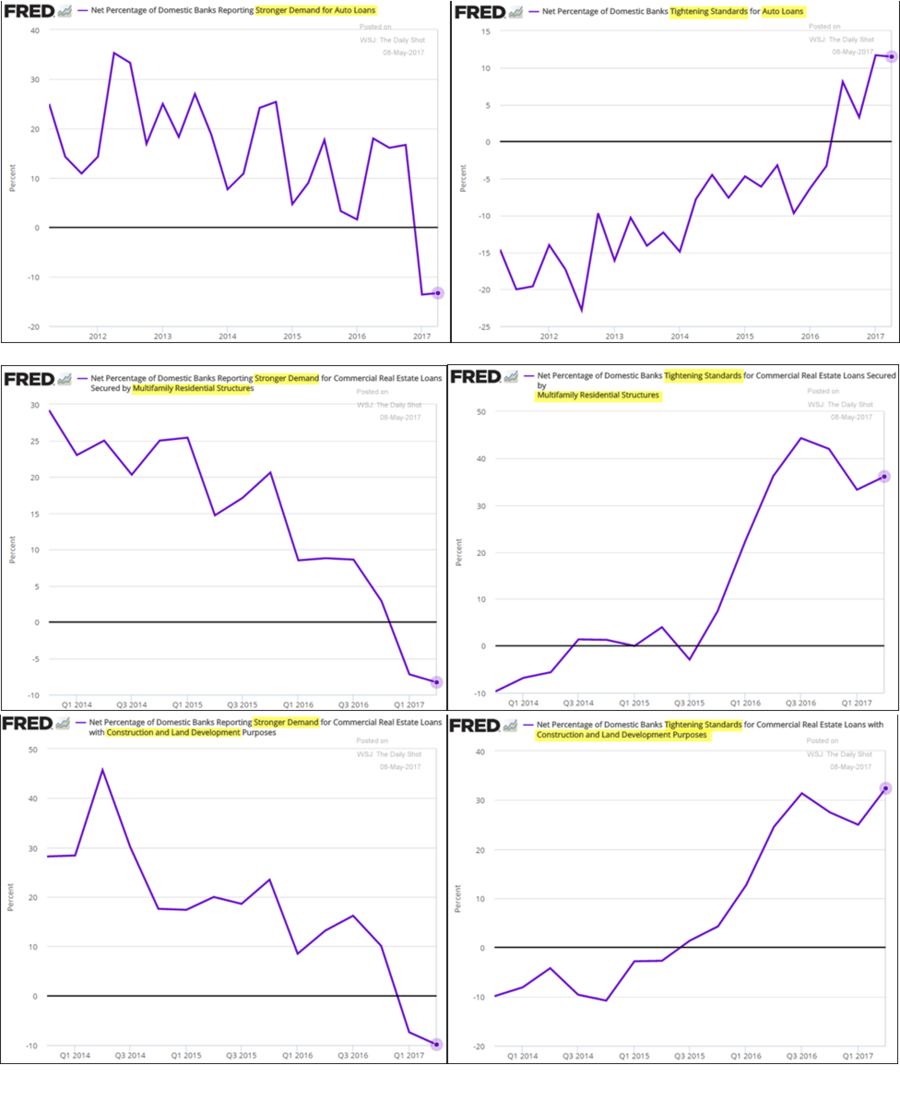

Last week the Daily Shot from the Wall Street Journal unknowingly offered a series of charts showing just how poor current economic thinking is, at least with respect to the world of finance.

Using data from the Federal Reserve’s Senior Lender Survey, the charts show that over the past five years, as demand for auto loans, multifamily residential loans and land development/construction loans has fallen, banks have tightened rather than loosened their credit standards. Banks have reduced supply coincident with demand rather than counter to it.

reminiscing on the Housing Crisis...

To be clear this is hardly the first time we have seen this non-textbook supply/demand relationship in the credit world. At the peak in the housing bubble, lenders were jubilantly giving out 110% loan-to-value mortgages backed by hyper-valued properties to insatiable NINJA borrowers, too. The more borrowers wanted mortgages, the more bankers were happy to oblige.

In 2005, we witnessed a historic simultaneous peak in both the supply and demand for residential credit, that was then followed by an equally historic and simultaneous collapse in both. At the lows in early, 2009 anemic mortgage demand was matched by some of the most onerous terms in modern US housing history.

When it comes to finance – whether it is borrowing, lending or investing more broadly – supply and demand move together. All reflect confidence coincidentally. They don’t move in opposition like Econ 101 textbooks would suggest; they move as one. Everyone wants in at the top and out at the bottom.

To be fair, and to give credit where credit is due, I am not the first to observe this peculiar relationship in the financial markets. I became aware of it thanks to the pioneering work of Bob Prechter, whose new book, “The Socionomic Theory of Finance,” I highly recommend. He focused me on the point that when it comes to supply and demand, “utility” goods and “speculative” financial products don’t behave similarly. Tulips bulbs, for example, get priced one way when they go in the ground, and another way altogether when they are traded.

While it would be nice if economists understood how, and even more importantly why, the supply and demand for credit move in unison with confidence, the charts above are warning us of something. For at least the three segments of the credit world shown above, borrower and lender confidence peaked 3-4 years ago and has turned down sharply.

With the major equity markets now soaring to new all-time highs, I am sure that many will chuckle at the notion that a major peak in borrower and lender confidence is not just behind us, but several years ago.

So, let me offer a few charts that may help to further support that view.

The St Louis Fed’s Financial Stress Index, a broad measure credit market strain, bottomed in June 2014; and despite the staggering flows into fixed income markets over the past 18 months, that point remains as the post-banking crisis recovery peak in systemic confidence.

Another measure of confidence, Gallup Economic Confidence Index, peaked six months later as gas prices troughed in early 2015. After adjusting the index for the highly partisan 2016 post-election political “relief,” that date remains the post-banking crisis high in confidence, too.

The most extreme sectors – auto lending, among them, for example – from this cycle have turned first. Others with soon follow. As the last in, the worst always go first when the cycle turns.

The big elephant in the room, though, is and will continue to be corporate lending, especially given the role of fixed income ETFs. While the banks have been important lenders in this cycle, the real money has been outside of the banking system. When the ETF world decides to “tighten standards” watch out. Credit won’t just become more difficult to get, it will evaporate altogether. Lenders with market liquidity (or at least the perception of market liquidity) won’t stick around for long. The P2P lending space – the subprime of the “who needs committed liquidity anyway” meme of this cycle – has already shown that. The less risky will soon follow.

Finally, I would not ignore what this will mean for corporate stock buybacks.

As the chart above shows, not only has there been a clear positive relationship between corporations’ debt and buyback levels, but the former peaked more than two years ago. If there were ever a behavior in which borrower, lender and investor supply and demand were one great big reflection of confidence, it was debt-funded stock buybacks. Talk about a choir singing “Ode to Joy” in unison!

The worst have gone first – as they inevitably do when credit cycles turn down.

But the charts above tell a very clear story. The supply and demand for credit are now shrinking. Not only will this be trouble for economic growth ahead, but for corporations with supersized debt maturities in 2018, 19 and 20, it is going to turn their business into a garage sale. Anything that can be sold will be as companies scramble to resize their balance sheets for far smaller credit markets.

If you thought things were deflationary as the housing market struggled to resize itself in 2008, just wait. With goodwill and other intangibles among the biggest assets on many companies’ balance sheets today, corporations are going to realize that when it comes to available collateral, the cupboard is bare.

Valeant and others in the drug space are already demonstrating the challenges of reducing debt in a post-overconfident, intangible-laden world. I would recommend that you think of pharma as simply the “subprime” of what is to come.

When this credit cycle turns down, it won’t bounce folks. All the filling that was once there on company balance sheets to cushion a credit cycle downturn has been replaced by air. Tangible, real assets have been superseded by “this time is different” goodwill. Now coupled with “liquidity-driven” lenders (aka credit EFTs), the impact, when we hit bottom, will be, let’s just say, intense.

2014 was a non-textbook, textbook example of what a major credit cycle peak looks like – simultaneous overconfidence by lenders and borrowers. While economists may have missed it, you don’t have to.

Peter Atwater

Position in SDS, SH; creditor of JPM

EDITOR'S NOTE

This is a Hedgeye Guest Contributor note written by Peter Atwater, founder and president of Financial Insyghts. He previously ran JPMorgan’s asset-backed securities business. He is also the author of the book Moods and Markets (FT Press, 2012) which details how investors can improve returns by using non-market indicators of confidence. This piece does not necessarily reflect the opinion of Hedgeye.

* * * * *

The information contained herein was prepared solely for the clients of Financial Insyghts LLC (“Financial Insyghts”). Any distribution beyond the intended recipient is strictly prohibited.

Financial Insyghts provides analysis of and commentary on how changes in confidence alter human decision making. Financial Insyghts is not registered as a securities broker-dealer or as an investment adviser either with the U.S. Securities and Exchange Commission or with any state securities regulatory authority. The material provided herein is for informational purposes only for the clients of Financial Insyghts. While specific companies may be referenced herein, no information is intended as securities brokerage, investment, tax, accounting or legal advice, as an offer or solicitation of an offer to sell or buy, or as an endorsement, recommendation or sponsorship of any company, security, or fund.

Financial Insyghts cannot and does not assess, verify or guarantee the adequacy, accuracy or completeness of any information, the suitability or profitability of any particular investment, or the potential value of any investment or informational source.

©2017 Financial Insyghts, LLC.