We’ve been talking a lot recently about the acceleration in retail bankruptcies – to the tune of 2 per week. We saw four retailers of size file Ch.11 in the last 7 days alone.

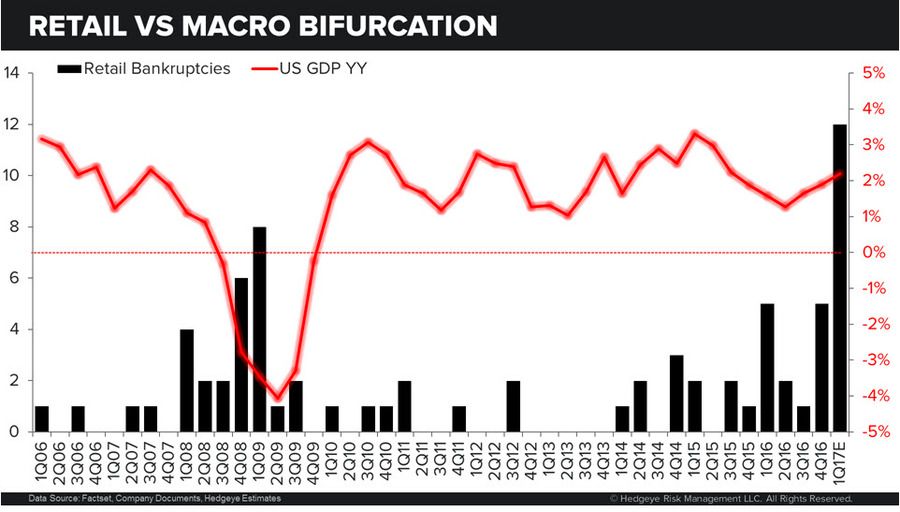

Take a close look at the chart below. It’s not what you’d expect to see.

Retail bankruptcies accelerated during the 2008-2009 financial crisis, as economic growth cratered. No real surprise—it’s what you’d presume would occur.

Fast forward to today

U.S. growth is accelerating, and yet .. retail bankruptcies are spiking to the highest levels we have ever seen. Not supposed to happen right?

My analyst team has been doing a lot of research into what’s going on. We have an idea on what’s driving this counterintuitive development.

We will explore this as one of our ‘game-changing’ themes in our “Retail 5.0” deck later this month. This is an important call. If you’re an institutional investor, email sales@hedgeye.com for more info and access.